Ford Motor Company (F) is shifting its focus towards software and services, forecasting an annual revenue growth of nearly 8% from its current $15 billion through 2030, according to the company’s first-quarter 2026 transcript. A significant driver behind this growth is the expanding aftersales and parts business, as Ford increases its catalog to cater to third-party repair shops across the U.S. Nearly 20% of repairs are now performed remotely, directly at customer locations, particularly beneficial for commercial fleet operators.

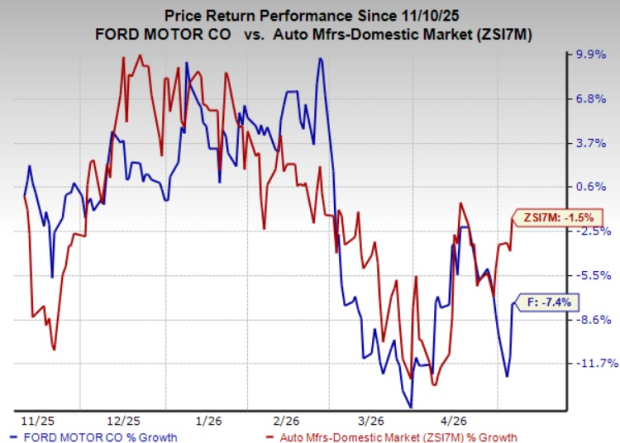

Ford’s parts business offers an annuity-like revenue profile, counter-cyclical to vehicle sales, enhancing the company’s resilience during downturns. Currently, Ford’s stock carries a Zacks Rank of #3 (Hold), and its share performance has declined 7.4% over the past six months, underperforming the automotive domestic industry, which saw a 1.5% decline.

Valuation-wise, Ford trades at a forward price/sales ratio of 0.28, significantly lower than the industry average of 3.51, and far below peers like General Motors (0.38) and Tesla (14.71). The Zacks Consensus Estimate for Ford’s EPS has witnessed minor adjustments in the past week, with a 5-cent increase for 2026 and a 2-cent decrease for 2027.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.