For the past couple of years, the cloud computing sector experienced a bear market, leaving investors a tad disheartened. However, in 2024, cloud computing stocks are resurging with artificial intelligence (AI) taking center stage, taking the tech world by storm in the first two months of the year.

While the AI hype is reaching new heights, it’s worth noting that cloud software maintained a steady presence even during the downturn. Surprisingly, global spending on cloud computing continued to rise despite heightened investor concerns. Analysts at Gartner forecast that end-user spending on cloud services is set to reach $680 billion in 2024, up from $411 billion in 2021, showing the relentless growth trajectory of the market.

The Ongoing Cloud Revolution

The surge in cloud spending has not only caught the attention of tech giants but has also led to an upswing of smaller software companies, particularly in the security and analytics domain. One such company that has been steadily churning out profitable growth since its IPO in 2019 is Dynatrace, a leading player in cloud observability and application performance monitoring (APM).

Dynatrace stands out in the market, providing its cloud observability and security software to some of the world’s largest organizations, giving it an edge over its competitors.

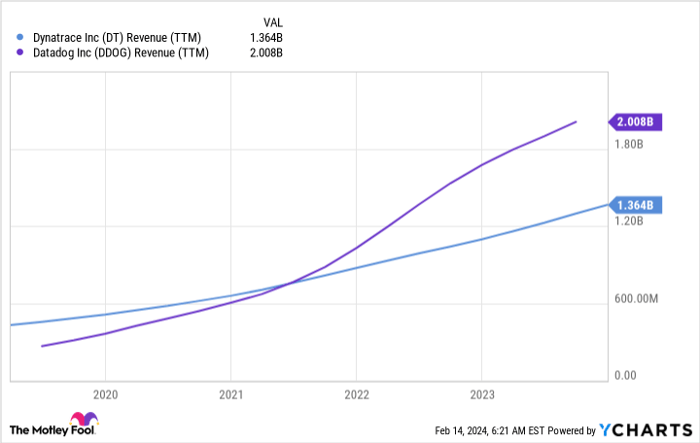

Resilience in Steady Growth

Constantly evolving to cater to modern demands, Dynatrace excels in all IT environments, whether it’s cloud-based or traditional setups. This flexibility has been a key driver behind its steady revenue growth, consistently hovering around 20% for the past few years. The company’s ability to adapt to the needs of big and complex customers sets it apart in an increasingly competitive landscape.

Data by YCharts.

Dynatrace’s Lucrative Prospects

In the fourth quarter of 2023, revenue surged 23% year-over-year to $365 million. Notably, this growth outpaced the company’s own guidance, showcasing its ability to consistently deliver robust results even during challenging times.

Furthermore, Dynatrace’s profitability metrics are equally impressive. In the same quarter, the company achieved a net income margin of 11.7% and a free cash flow (FCF) margin of 18%, underlining its prowess in generating profits without compromising on growth. Its strong financial position, with substantial cash reserves and zero debt, underscores its stability in the market.

Although trading at a premium, Dynatrace’s strong fundamentals and promising growth trajectory make it an attractive investment opportunity. The company’s ability to capture a significant share of the high-growth cloud observability and APM market further solidifies its position as a compelling investment prospect.

Even with the high premium, I view Dollar-Cost Averaging as an appropriate strategy for investing in Dynatrace, especially given the company’s consistent execution and growth strategy.

Is Dynatrace Worth Your Investment?

While Dynatrace shows immense potential, investors should conduct thorough research and weigh the risks before making any investment decisions. It’s important to consider the dynamics of the market and understand the long-term prospects of the company.

*Stock Advisor returns as of February 12, 2024

Nick Rossolillo and his clients have positions in Broadcom and Dynatrace. The Motley Fool has positions in and recommends Cisco Systems, Datadog, and Splunk. The Motley Fool recommends Broadcom and Gartner. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.