Altria Group’s Investment Potential

When it comes to long-term investments, the focus is on companies that play essential roles in today’s economy, spanning transportation, healthcare, defense, financial services, energy, and related sectors.

The investment strategy aims to strike a balance between growth and value, avoiding strict categorization as either a “growth” or “value” investor.

As a result, the portfolio typically holds companies yielding between 2.5% and 3.0%, with an annual dividend growth rate in the high-single-digit to low-double-digit percentage range, subject to economic conditions.

Cigarette giant Altria Group, Inc. (NYSE:MO) is not an obvious candidate for inclusion in this portfolio due to concerns surrounding the industry it operates in.

- Despite personal reservations about the industry, the company is weathering significant headwinds from anti-smoking campaigns and regulatory actions that impact cigarette sales.

- Nonetheless, the stock is capturing attention as it currently offers a 10% yield and an attractive valuation.

- The company’s ability to sustain growth, notably through pricing strategies, investment in alternative segments like NJOY, and a robust balance sheet, positions it as a potential opportunity for >15% annual returns.

- While the industry faces challenges, Altria’s resilience in the face of adversity is evident from its consistent dividend growth and pricing power, factors that contribute to its appeal as an investment.

Given these points, it seems prudent to explore Altria’s potential as a stock for a dividend growth portfolio.

Seeking Value in the Market

A shift toward value investments is emphasized in light of lofty stock market valuations, which could limit equity returns in the near future. This sentiment was expressed in the 2024 Outlook article, where a potential shift in focus from capital gains to dividends was highlighted.

It’s been observed that when market valuations are stretched, investments with better valuations and higher yields tend to fare well, with dividends assuming a more significant role in total returns.

Altria’s appeal as a value stock is underlined by its performance relative to the S&P 500 and the contrasting trajectories of value and growth stocks in the market since the Great Financial Crisis.

The stock’s notable resilience and strong performance, despite the ongoing challenges faced by the industry it operates in, suggest that it may be an undervalued gem in the current market landscape.

The Dividend’s Enduring Appeal

Altria’s allure as an investment is further underscored by the consistent strength of its dividend. Despite the industry’s tribulations, the stock has delivered impressive returns over the last two decades, a testament to the enduring appeal of its dividend and pricing power.

Altria’s Dividend Growth and Market Strategy

When people think of Altria, they think of a juicy dividend.

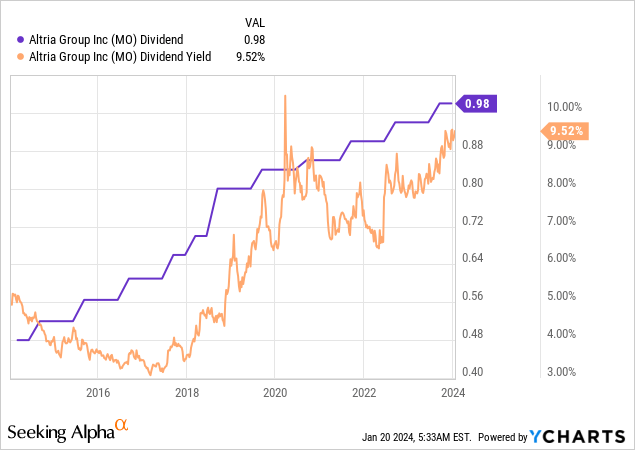

After hiking its dividend by 4.3% on August 24, 2023, Altria currently pays $0.98 per share per quarter. This translates to a yield of 9.7%.

The dividend king, which has hiked its dividend for more than 50 consecutive years (adjusted for the Phillip Morris (PM) spin-off), yielded barely more than 3% in 2017. Now, it yields 10%, one of the highest numbers in its recent history.

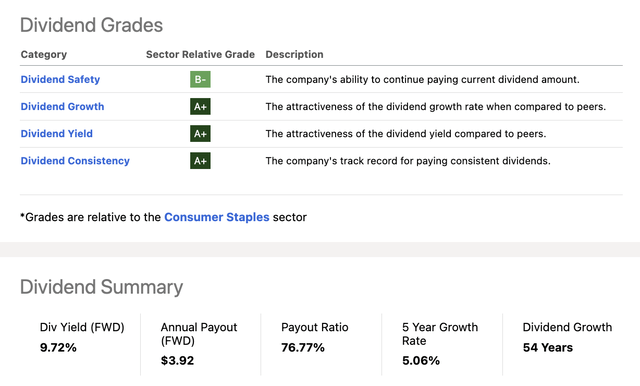

Thanks to a healthy balance sheet with an investment-grade BBB credit rating and a sub-2.0x net leverage ratio, the company can prioritize shareholder returns over debt reduction.

It also has a healthy payout ratio.

In 2024, MO is expected to generate $8.6 billion in free cash flow, roughly 12.1% of its current market cap!

This translates to a cash payout ratio of 80%.

Next year, free cash flow is expected to fall to $8.0 billion, which would still be 11.2% of its $71.3 billion market cap.

As a result, the five-year dividend CAGR is 5.1%, which is extremely high for a company with a 10% yield (or any yield above 7%, frankly).

These numbers explain why the company has one of the best Seeking Alpha dividend scorecards in the consumer staples sector:

With that in mind, let’s take a closer look at the company’s numbers.

Altria’s Steady Earnings Growth

Altria is on a path for consistent earnings growth.

In its most recent quarter, 3Q23, the company reported a 3.3% growth rate in adjusted diluted earnings per share for the first nine months of the year.

According to the company, this performance reflects the resilience of their traditional tobacco businesses in a dynamic operating environment.

This growth rate was possible despite a notable continuation of high declines in the volume of the cigarette industry.

This trend was primarily attributed to a combination of macroeconomic factors and the increasing prevalence of illegal disposable e-vapor products.

Altria Group Inc: A Smoky Yet Promising Investment

Resilient Pricing Power and Market Position

Amidst a challenging environment, Altria has stood strong, displaying resilient pricing power. Despite aggressive price hikes, the iconic Marlboro brand managed to gain retail share within the cigarette category. The company’s ability to command a 8.6% net price realization in the third quarter and a significant 9.8% for the first nine months is a testament to its robust position in the market. This strength was further highlighted by the impressive growth of Marlboro’s share within the stable premium segment, reaching 58.9%.

The cigarette industry, infamous for its cyclical challenges and illegal competition, has hindered many players. Yet, Altria has managed to weather these storms, showcasing the potential for consistent growth moving forward.

Earnings Outlook and Market Expectations

Altria’s commitment to delivering solid financial performance is evident from its expected adjusted diluted earnings per share in the range of $4.91 to $4.98 for FY2023. This represents a growth rate of 1.5% to 3% from the base of $4.84 in 2022. Despite the volatility in the market, analysts expect the company to announce earnings of $1.17 per share, aligning with Altria’s own guidance range of $4.96 for the full year.

Valuation and Potential Returns

Looking at the valuation metrics, Altria seems to be trading at an attractive multiple, presenting a compelling investment opportunity. The stock is undervalued by up to 34% according to a 10x EBITDA multiple, with a fair price target of $54. Such undervaluation implies potential annual returns upwards of 15% over the next three years, including dividends and potential buybacks. A conservative estimate, at $40 per share, suggests a return between 15% and 20% on a prolonged basis.

Potential for Value Investment

Considering the potential trigger for improving its valuation through higher e-vapor regulation and rising consumer confidence, Altria stands as a promising value investment. In a environment emphasizing a shift towards value investments, Altria’s undervaluation and robust earnings outlook make it a compelling consideration.

Concluding Thoughts

Altria, though operating in a controversial industry, presents an intriguing investment opportunity. Its current 10% yield, strong market position, and attractive valuation make it a potential value gem. As the company continues to make strategic moves in alternative segments and showcase resilient earnings, it stands as an attractive consideration for a 3-5% position in many dividend growth portfolios.