As the possibility of a more accommodating Federal Reserve and rate decreases loom, the hunt for high-yield dividends may grow more arduous for income investors.

Staggering interest rates, however, do not mean that lucrative dividend stocks are out of reach in the market.

Rida Morwa, a distinguished analyst at Seeking Alpha and leader of the Investing Group, offers insight on areas where income investors can unearth promising dividend investments for the year 2024.

His advice: Keep cash readily available, home in on sectors benefiting from dwindling rates, and foster a portfolio that ensures steady income irrespective of market conditions.

According to Morwa, there’s always a “forgotten” gem.

Morwa’s perspective is presented below:

Seeking Alpha: Income generation is a significant focus for you. How will the Fed’s movement to a more dovish stance in 2024 impact income investing?

Rida Morwa: Opting for U.S. Treasuries, agency mortgage-backed securities, or high-grade corporate bonds remains a viable option for income-seeking investors. Although T-Bills at a 0.25% or lower yield may not entice most, offering zero credit risk and a 3%, 4%, or even a 5% yield would pique the interest of numerous income investors.

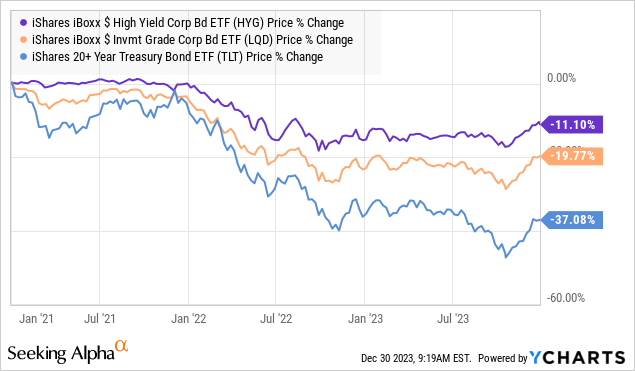

Investors who favored A-rated corporate bonds may consider T-bills or Treasuries instead. This shift pushes A-rated corporate bonds to trade at a lower price/higher yield, making them an attractive prospect for previous BBB bond investors. It’s a truism in income investing that seeking less risk for an equivalent yield is prudent. Consequently, bond prices are linked to Treasury prices. Lower yields amplify Treasury price effects. This is why high-yield bonds have notably outperformed investment-grade bonds.

Even common equities offering dividends are influenced by Treasury rate movements, akin to the constant gravitational force. However, similar to gravity, the influence diminishes the farther the equities are.

A decrease in interest rates raises bond prices across the board. The closer the bonds are to U.S. Treasuries in terms of risk, the more pronounced the surge will be. Other things remaining constant, declining interest rates will buoy all income-style investments.

Lower-risk fixed-income products such as Agency MBS and investment-grade corporate bonds or preferreds will reap the most benefits. Below investment-grade debt and common equities will also see gains from lower rates, but considerations such as potential recession concerns may assume greater significance in these cases.

Though 2023 afforded ample opportunities to secure high-yield investments aligned with our 8%-10% yield target, a dovish pivot by the Fed could make unearthing similar prospects more challenging. Nevertheless, overlooked pockets will still exist within the market.

SA: What errors should investors avoid while devising plans for the upcoming year?

RM: The gravest mistake any investor can make is presuming they can prophesize the future.

A question posited earlier assumed the Fed’s inclination to adopt a more dovish stance in 2024. While I concur that a Fed interest rate cut is the likeliest scenario for 2024, the Fed’s December meeting projections point to a Federal Funds rate of 4.5-4.75%. Personally, I believe the market underestimates the extent of the cuts the Fed will be compelled to implement. The crux is the word “believe.” Investors frequently mistake “believing” for “knowing.” Four years ago, investors held certain beliefs about 2020 that proved unequivocally wrong.

We should not manage our portfolios as we would speculate in Vegas. My portfolio aim is income production, irrespective of future correctness or fallacy.

This is why our model portfolio pivoted to being “agnostic” concerning interest rates throughout 2022 and 2023. We retained exposure to holdings that would flourish under a dovish Fed pivot and sectors thriving in a rising interest rate climate, such as business development corporations (BDCs), our primary source of dividend hikes and supplementary dividends over the past two years.

Should the pivot materialize in 2024, I anticipate that our most interest rate-sensitive positions will stage the most robust resurgence. Consequently, we have concentrated on augmenting these areas in recent months. Nonetheless, we will retain some exposure to BDCs, commodity funds, and floating-rate investments, beneficiaries if inflation escalates and the Fed opts for further hikes.

Do not assume you can predict the future. A well-structured portfolio should encompass positions flourishing if your predictions hold true, while also embracing positions thriving even if you are mistaken.

SA: Your defensive approach has found favor with you. What constitutes your defensive strategy for 2024?

RM: I pinpointed late 2023/2024 as the probable onset of a recession for a couple of years. With this timeline materializing, I persist in my belief that a recession beginning in 2024 carries significant plausibility.

Gratifyingly, adopting a defensive stance is straightforward and lucrative, even sans a recession. Many “defensive” investments have been trading at extremely discounted valuations. Preferred equity, bonds, utilities, healthcare, and REITs harbor abundant opportunities, trading at lows unseen in several years. Some are transacting at valuations not witnessed since 2009. These investments have a historical predilection to thrive during recessions. Even in the event of a gentle economic deceleration, current modest valuations furnish substantial upside potential.

For individuals subscribing to the notion that a robust offense is the pinnacle defense, agency MBS offers an appealing avenue.

The Looming Recession – A Wealth of Opportunities for Income Investors in 2024

In the world of investments, history often becomes the guiding star. It’s indeed fascinating to note how certain sectors, like those that primarily focus on agency MBS, have historically thrived during economic downturns. The looming recession in 2024, although daunting to many, presents a multitude of opportunities for income investors.

Sector Opportunities in 2024

Robert Merton, a well-known figure in the investment arena, points out some sectors that could harbor significant potential for income investors in 2024. These sectors include fixed income, agency mortgage REITs, equity REITs, healthcare, and utilities. Notably, these sectors have weathered the storm of rising rate cycles and stand to benefit from declining rates. They also possess the resilience to perform well in the face of a recession not driven by a financial collapse.

Economic Outlook and Maximizing Returns

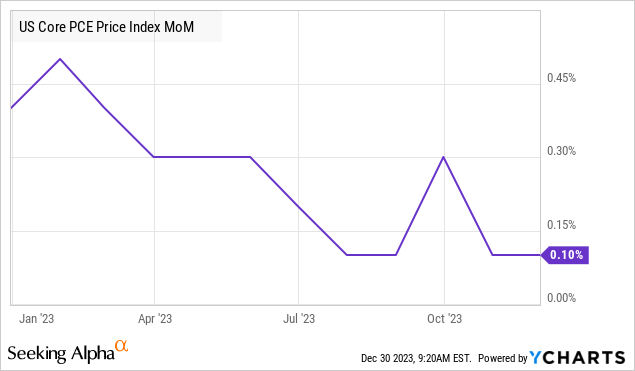

Considering the economic landscape, it’s vital to be mindful of the current scenario. Merton believes that Core PCE inflation may reach the Fed’s 2% goal, possibly in the first half of the year. The trends over the past 12 months have shown mild Core PCE inflation, mitigating concerns. However, the possibility of a recession remains palpable, and it could materialize faster than expected, as historical metrics often lag current economic realities.

Despite the uncertainty, Merton emphasizes a focus on tangible returns and income generation. Citing Benjamin Graham, he underscores that market dynamics often reflect prevailing sentiments rather than enduring value. The pursuit of a high yield, irrespective of market conditions, remains an evergreen endeavor.

Opportunities Amid Market Flux

Merton’s philosophy extends to advocating a vigilant search for investments that promise a robust income stream, underpinned by sound fundamentals. He stresses the enduring presence of high-yield opportunities, stemming from sectors temporarily out of favor or possessing “accidental high yields.” These undervalued stocks often hide in plain sight, offering substantial potential for discerning investors.

Merton’s team prides itself on the tenacity to unearth such opportunities through meticulous research and analysis. This resilience to delve deeper into the market fabric is indeed a hallmark of successful income investing.

The Advantage of Liquidity

In Merton’s view, constructing a portfolio brimming with income-generating assets confers the invaluable gift of liquidity. The regular inflow of funds into the investment accounts allows for swift capitalization on market downturns, offering the luxury to remain unperturbed by any need to liquidate holdings for personal cash requirements, particularly for those in retirement.

This liquidity, as Merton extols, endows income investors with the ability to seize opportunities as they arise, ensuring that no potential windfall is missed due to a dearth of available capital. The ceaseless stream of income thereby perpetuates an endless cycle of cash flow, a hallmark and allure of income investing.