I will be celebrating my birthday in May.

More specifically, on the 10th. That’s only four months away!

Putting plans in motion now is essential if I want to throw an impressive birthday bash. Just like preparing well in advance for investments pays off.

This past weekend, I had to drop off my car at the Porsche shop. To my delight, the dealership offered me a loaner—none other than a 2023 Porsche Taycan in arctic blue, which has now made its way onto my wish list. For the uninitiated, I have a soft spot for high-quality cars. While most vehicles don’t appreciate in value, I’ve found that certain top-notch cars, acquired sensibly, tend to do just that.

My eyes are set on a reward from Mr. Market on or before May 10th. Wondering how? Keep reading…

An Analysis Worth its Weight in Gold

I’m known to be a real estate investment trust, or REIT, analyst. Over time, I have managed to grow my nest egg by making shrewd investments in stocks when they are trading at discounted prices.

Seems simple, right? But it all starts with identifying quality. Just like my love for the Taycan, to comprehend quality, I dig deep…

Earnings history, Dividend history, Dividend safety, Balance Sheet, Management, Growth prospects—all of these attributes are crucial when evaluating stocks. And if any of these factors fall short, I steer clear. Why settle for a Volkswagen when you can have a Porsche?

Now, if quality is the baseline, then the subsequent step is the price. What I desire is a Porsche for the price of a Volkswagen. How does one achieve that? It’s all revealed in the following picks…

My Top 3 Strongest Convictions

What else is significant about May? The Federal Reserve is scheduled to convene again on January 30th and will conclude with a policy statement on January 31st.

As of January 10th, the possibility of the FOMC leaving the short-term federal funds rate unchanged at a target range of 5.25% to 5.50%, according to CME Group’s FedWatch Tool, has been pegged at 95% by interest rate traders.

We anticipate the Fed might begin to lower rates at the May meeting, or perhaps even as early as March. It’s already evident from the market reaction to the word “pause” that significant shifts can occur. Needless to say, it looks promising. But is it really? Let’s delve into the details…

Scouring through the 2-year chart offers a broad-brush exercise, with the Vanguard Real Estate ETF (VNQ) serving as the benchmark. However, it’s imperative to remember that one cannot paint all REITs with the same brush. In my view, the top-tier REITs boasting robust balance sheets will outperform their peers in the coming months and quarters. When rates do fall, the decline won’t be abrupt, and many of the lower-quality REITs will likely continue to face hurdles. I’m betting on the so-called blue chips, and that’s precisely what I’m adding to my portfolio.

So, without further ado, let’s celebrate my birthday with these investments!

Lightning in a Bottle – Four Corners Property Trust, Inc. (FCPT)

FCPT had its origins as a subsidiary of Darden Restaurants back in 2015. It was established with the goal of acquiring, owning, and leasing restaurants and other food-related properties on a net basis.

Late in 2015, FCPT was spun off and obtained a 100% equity interest in 418 restaurants operated by Darden, predominantly under the Olive Garden and LongHorn Steakhouse banners.

Now functioning as an independent net lease REIT, FCPT specializes in the acquisition and management of restaurants, along with a sprinkling of other retail properties, primarily consisting of automotive service and medical retail.

Based on the latest update, FCPT’s portfolio comprised 1,106 commercial properties operating under 148 brands across 47 states. Of note, some of the prominent brands FCPT’s properties are associated with include Olive Garden, LongHorn Steakhouse, Chili’s, Red Lobster, Outback Steakhouse, Arby’s, Burger King, as well as non-restaurant brands such as Caliber Collision, WellNow Urgent Care, NAPA auto parts, and Aspen Dental.

Olive Garden stands tall as FCPT’s largest tenant, accounting for 37.0% of their annualized base rent (“ABR”). Both LongHorn and Chili’s follow closely as the second and third largest tenants, contributing 10.4% and 7.9% of FCPT’s ABR, respectively.

FCPT closed the third quarter with a portfolio that boasted 99.8% occupancy, 4.8x tenant EBITDAR coverage, and an average remaining lease term of 8 years.

While primarily recognized for its restaurant properties, this net lease REIT has recently been venturing into other e-commerce resistant industries such as the automotive sector and medical retail.

REITs: A Deep Dive into FCPT and ARE

Four Corners Property Trust

Four Corners Property Trust (FCPT) is making strategic investments in auto service properties that are not dependent on the combustion engine. As electric vehicle adoption continues to increase, FCPT targets tire service and collision repair properties, ensuring their relevance in the evolving automobile industry. With 138 leases in its Auto Industry portfolio, FCPT’s auto-related properties currently represent 9% of its ABR.

Aside from its Auto Industry portfolio, FCPT also focuses on medical retail properties, specializing in urgent care, dental, veterinary, and outpatient services. With 84 leases in this sector, FCPT’s medical retail properties contribute 7% to its ABR.

Despite the challenging market conditions, FCPT maintains an investment-grade balance sheet with a Baa3 credit rating from Moody’s. Their solid debt metrics, including a net debt to adjusted EBITDAre of 5.6x, a long-term debt to capital ratio of 42.17%, and a fixed charge coverage ratio of 4.2x, demonstrate their financial stability and ability to weather market fluctuations.

Furthermore, FCPT has achieved an average adjusted funds from operations (AFFO) growth rate of 4.20% since 2019, coupled with a compound dividend growth rate of 10.60%. Analysts anticipate a positive trajectory for AFFO per share, with expected increases of 3% in both 2024 and 2025, followed by a 7% upturn in 2026.

With a notable 5.48% dividend yield, well-covered by an 81.74% AFFO payout ratio, FCPT’s stock is a compelling investment. Its current P/AFFO of 15.06x, compared to an average AFFO multiple of 19.47x, suggests potential upside for investors.

If FCPT can reclaim its 5-year normal AFFO multiple of 19.58x by the end of 2024, investors could realize a substantial total annual rate of return of 40.76%.

We rate Four Corners Property Trust a Hold.

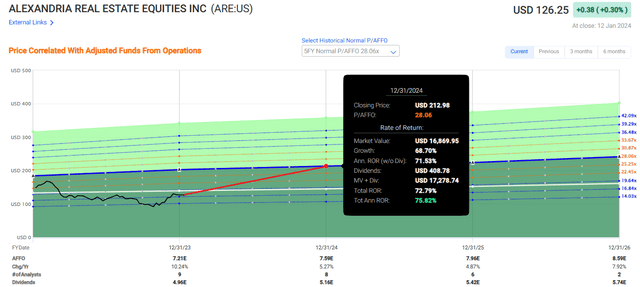

Alexandria Real Estate Equities, Inc. (ARE)

Alexandria Real Estate Equities, Inc. (ARE) operates as a life science REIT, distinguishing itself from traditional office REITs. With a massive 75.1 million SF asset base in North America, ARE has solidified its position as a pioneer and leader in the life science real estate niche. The company’s properties are utilized by renowned pharmaceutical, biotechnology, and healthcare-related organizations, along with prestigious academic institutions, reflecting the esteemed stature of ARE’s real estate offerings.

Unlike traditional office spaces, tasks conducted in ARE’s lab facilities are heavily regulated and cannot be feasibly conducted remotely. The company’s third quarter results affirm this with substantial leasing volume and impressive rental rate increases, indicating strong occupancy and demand for its specialized real estate properties.

ARE’s status as a blue-chip REIT is reinforced by its BBB+ credit rating and impressive debt metrics, including a net debt plus preferred stock to Adj EBITDA of 5.4x, a long-term debt to capital ratio of 39.05%, and a fixed charge coverage ratio of 4.8x. Furthermore, 99.0% of their debt is fixed rate, underpinning their financial strength and stability.

Over the years, ARE has demonstrated an average AFFO growth rate of 5.91%, coupled with an average dividend growth rate of 6.64%. Analysts project a positive outlook for ARE, with anticipated AFFO per share growth of 5% in both 2024 and 2025, followed by an 8% upturn in 2026.

With a 4.02% dividend yield and a well-covered 68.79% AFFO payout ratio, coupled with a P/AFFO of 17.48x (compared to a 10-year average AFFO multiple of 25.11x), ARE’s stock demonstrates potential value at its current trading levels.

If ARE can ascend to its 5-year normal AFFO multiple of 28.06x by the end of 2024, it could yield a substantial total annual rate of return of 75.82%.

We rate Alexandria Real Estate a Strong Buy.

Rexford Industrial Realty: Master of SoCal

Rexford Industrial Realty, Inc. (REXR)

Rexford Industrial Realty, Inc. (REXR) stands tall as an industrial REIT with a solid market cap of approximately $11.45 billion and a substantial 45.8 million SF portfolio comprising 373 industrial properties solely situated throughout infill Southern California (“SoCal”).

Dominating SoCal’s High Demand Market

Focusing on acquiring, redeveloping, and managing properties in SoCal, this REIT aims to dominate the fourth largest industrial market in the world and the highest demand, lowest supply market in the United States.

The SoCal region’s attractiveness stems from the size of its economy and scarce availability of land for development. Surrounded by natural barriers and constrained by burdensome state regulations, the supply of developable land remains limited.

Amidst the scarcity, Rexford considers its portfolio irreplaceable and mission-critical for commerce in the region.

Fortress-Like Balances and Growth Prospects

Rexford Industrial boasts a BBB+ credit rating and a fortress-like balance sheet, with impressive ratios showcasing its financial strength – a net debt to Adj EBITDA of 3.7x, a long-term debt to capital ratio of 24.23%, and an EBITDA to interest expense ratio of 7.92x.

With all debt fixed rate, carrying a weighted average interest rate of 3.6% and having no material debt maturities until 2026, inclusive of their 2024 extension options, the industrial REIT had $1.5 billion of liquidity at the end of the third quarter.

Impressive Growth Trajectory

Since 2016, Rexford Industrial has been a growth machine, with only 1 year of negative growth (2019) and an impressive blended average AFFO growth rate of almost 15% since then.

Its projected AFFO growth rates of 16% in 2024 and a further 21% in 2025 point towards an even more accelerated growth trajectory.

Brad’s Birthday Picks: An Optimistic Portfolio

The writer, evidently invested in Rexford Industrial Realty, is intrigued by the potential of the REIT, planning to add another one to their portfolio. They even go as far as to create a whimsical portfolio named “Brad’s Birthday Picks” for entertainment, showcasing their enthusiasm for these investments.

Closing on an optimistic note, the writer urges investors to always check under the hood before making any investment decisions, wrapping up their investment musings with a cheerful “Happy SWAN Investing!”

And now it’s time to get back behind the wheel of my loaner car.

Just remember, before you buy anything, always check under the hood!

Happy SWAN Investing!