Alibaba’s Q4 Earnings Highlight Strong Growth and Valuation Potential

Alibaba Group (BABA) recently unveiled its fourth-quarter fiscal 2025 financial results, reflecting resilience and a strategic approach that positions the company favorably for investors. Although revenue estimates were slightly missed, Alibaba showcased robust earnings growth and demonstrated strong momentum across its primary business segments. Currently, shares are trading at notably lower valuations compared to industry rivals, suggesting that BABA is an appealing investment opportunity.

Strong Earnings Growth and Strategic Focus

For the fourth quarter of fiscal 2025, Alibaba reported non-GAAP earnings of $1.73 per ADS, exceeding analyst expectations by 16.89%. This marks a significant 23% year-over-year increase in earnings, showcasing strong operational efficiency despite challenging market conditions. Revenue totaled $32.6 billion (RMB 236.5 billion), rising by 7% year over year, though it missed the consensus estimate slightly. However, adjusted EBITA surged by 36% to RMB 32.6 billion ($4.5 billion).

The company’s outstanding performance is a result of effectively executing its dual growth strategy centered around e-commerce and AI + Cloud, with each segment reporting year-over-year EBITA improvements. Management’s “user first, AI-driven” strategy is bearing fruit, as evidenced by accelerated growth across its core businesses, positioning Alibaba to utilize its technological advantages while sustaining leadership in its traditional e-commerce markets.

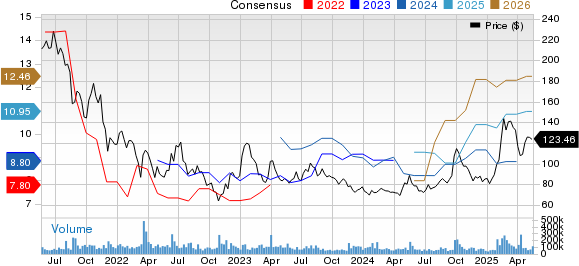

The Zacks Consensus Estimate for fiscal 2026 indicates revenues of $143.48 billion, reflecting an anticipated growth of 3.87%. Furthermore, earnings estimates for fiscal 2026 have seen a revision upwards by 1.1% over the last two months to $10.95 per share, signaling market optimism regarding Alibaba’s growth path.

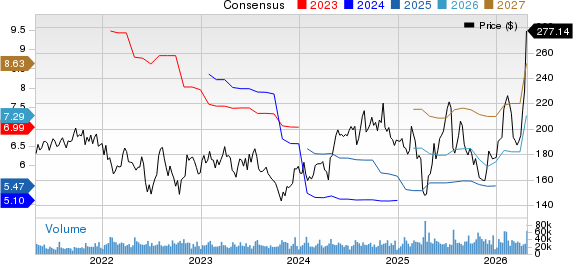

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Strong Momentum in AI-Driven Cloud Growth

The company’s Cloud Intelligence Group is demonstrating impressive performance. Cloud revenues increased 18% year over year, and AI-related product revenues have attained triple-digit growth for the seventh consecutive quarter. This upward momentum allows Alibaba to capture substantial market share in the swiftly evolving cloud computing and AI sectors.

Significant investments have been made in AI infrastructure and advanced technologies, reinforcing Alibaba’s leadership stance on the global stage. The launch of its next-generation Qwen3 model as open source was a notable achievement, with the model ranking highly on various authoritative benchmarks, underscoring Alibaba’s innovation commitment.

Alibaba’s AI products are penetrating industries beyond traditional technology, including manufacturing and agriculture. This diversification indicates considerable growth potential as AI adoption accelerates around the globe. Given the increasing role of AI in defining technology trends over the next 10 to 20 years, Alibaba’s foresight and continued investment in this area are critical long-term growth drivers.

Attractive Valuation Offers a Compelling Entry Point

Despite robust performance metrics and beneficial growth trajectories, Alibaba’s stock is substantially undervalued relative to competitors. With a forward 12-month Price/earnings ratio of 11.07X, Alibaba trades at less than half the Zacks Internet-Commerce industry average of 22.29X, suggesting that BABA shares present a significant value opportunity.

BABA’s P/E F12M Ratio Depicts Discounted Valuation

Image Source: Zacks Investment Research

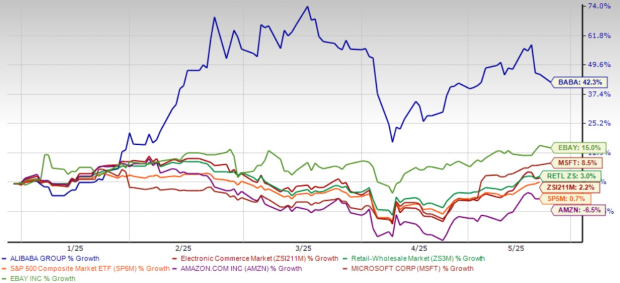

This valuation disparity becomes more evident when contrasting Alibaba’s performance with that of its peers. The stock has appreciated by 42.3% year to date, outperforming the S&P 500, which achieved returns of 0.7%, as well as the Zacks Retail-Wholesale sector, at 2.2%. Yet, Alibaba continues to trade at significantly lower multiples than comparable technology companies.

BABA Beats Peers & Sector Year to Date

Image Source: Zacks Investment Research

Alibaba’s performance stands out in comparison to leading global e-commerce players, including Amazon (AMZN) and eBay (EBAY). Despite facing competition from top cloud providers like Amazon, Microsoft (MSFT), and Google, where Amazon’s stock has declined by 6.5% year to date, Alibaba’s relative strength is evident. Meanwhile, eBay and Microsoft have experienced returns of 15% and 8.5%, respectively.

A noteworthy aspect of Alibaba’s investment appeal is its commitment to shareholder returns. The company’s board approved an annual dividend of $1.05 per ADS (a 5% increase) and a special dividend of 95 cents per ADS, totaling $2.00 per ADS ($4.6 billion). In fiscal 2025, Alibaba returned a total of $16.5 billion to shareholders, demonstrating management’s confidence in the long-term outlook of the firm.

Investment Outlook: Positioned for Long-Term Growth

With a solid core e-commerce business, rapid growth in cloud and AI segments, and strong performance in international commerce (22% revenue growth this quarter), Alibaba stands as a compelling investment opportunity. The company possesses a robust net cash position of $50.5 billion, which provides ample resources for strategic investments and continued shareholder rewards.

Even as Alibaba contends with competition from global e-commerce and cloud computing firms, its attractive valuation, strong financial performance, and strategic emphasis on high-growth sectors like AI position BABA Stock as a wise investment for those seeking value and growth potential in 2025. BABA Stock currently holds a Zacks Rank #2 (Buy).

7 Best Stocks for the Next 30 Days

Recently released: Experts have identified 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys, indicating these tickers may see early price gains.

Since 1988, this curated list has outperformed the market more than two-fold, averaging an annual gain of +23.0%. These 7 stocks deserve immediate attention.

Want the latest recommendations? Download the 7 Best Stocks for the Next 30 Days report.

This article was originally published on Zacks Investment Research.

Zacks Investment Research

The views and opinions expressed herein represent those of the author and do not reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.