PetMed Express (PETS)

One does not need a crystal ball to foresee the stormy weather that lies ahead for the online pet pharmacy, PetMed Express (NASDAQ:PETS). The company, mired in financial mismanagement, recently made the perplexing decision to halt dividends in Q2, aiming to steer funds towards expansion.

Q2 did not bring any silver lining for PETS, with the firm missing analyst estimates for the sixth consecutive quarter. With net sales of $71 million falling short by $5 million and adjusted EBITDA plummeting 55% year-over-year (YOY), the red flags are glaringly evident.

The dismal performance of PETS stock stands in stark contrast to broader market exuberance. Shedding over 64% of its value in a mere decade, it has woefully underperformed the S&P 500. With a negative return on common equity standing at 4.83%, the outlook is anything but promising, pointing towards the need for investors to divest.

Fisker (FSR)

Like a car stuck in the mud, electric vehicle (EV) player Fisker (NYSE:FSR) finds itself navigating through murky financial waters. The company’s recent slump led to a notice from the New York Stock Exchange due to the inability to maintain a minimum stock price of $1 per share over 30 consecutive days.

The road ahead looks bumpy for Fisker, with a massive net loss of $463.6 million in Q4 and a concerning 67% decline in cash reserves since December 2020. CEO Henrik Fisker’s ‘going concern’ warning during the latest earnings call further adds salt to the wound, hinting at a storm on the horizon. Reports of bankruptcy looming on the horizon only intensify the conundrum, making FSR one of the top penny stocks to shed.

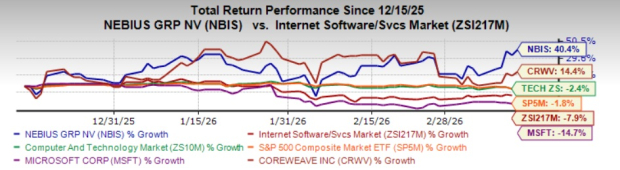

LivePerson (LPSN)

As the competition in the conversational AI arena heats up, LivePerson (NASDAQ:LPSN) finds itself sinking in turbulent waters. The company’s struggle is evident, with dwindling growth and lackluster earnings clouding its prospects.

In a bid to turn the tide, LivePerson’s 2024 strategy zeroes in on high-margin ventures while shedding excess baggage. However, the journey ahead seems arduous, with the company’s stock plummeting over 72% year-to-date (YTD).

Latest financial reports paint a grim picture for LPSN, with GAAP EPS plunging to a negative 48 cents in Q4, missing analyst projections by a wide margin. Adding to the misery, YOY revenue took a hit, declining by 22.1% to $95.47 million, marking the fourth consecutive quarter of double-digit sales decline. The guidance ahead looks equally somber, signaling rough seas for investors.

Penny Stock Woes in MicroVision, Lucid Group, and New York Community Bancorp

Lurking Shadows at MicroVision (MVIS)

MicroVision (NASDAQ:MVIS) is akin to a novice driver stuck at a crossroads – full of potential but unsure of the road ahead. Known for its lidar technology crucial for self-driving vehicles, the company’s stock has enjoyed a fleeting moment of glory driven by meme stock frenzy. Yet, lurking beneath the surface lies a tale of caution and hesitation. Despite trumpeting advancements in lidar technology, MicroVision is candid about its lengthy journey to market viability and profit. With the slowdown in the broader EV sector casting a looming shadow, investor faith in EVs, and by extension, in MicroVision, hangs in the balance.

The steady drumbeat of MicroVision’s long road to commercial sustainability, paired with the lukewarm sentiment towards the EV market, paints a complex and delicate picture. The allure of meme-driven rallies might offer fleeting highs, but the sobering reality of MicroVision’s speculative future looms large, making it a penny stock earmarked for the chopping block.

Challenges Galore for Lucid Group (LCID)

The journey of EV upstart Lucid Group (NASDAQ:LCID) since its stock market debut cartwheels between disappointments and setbacks, akin to a marathon runner tripping at the finish line. With LCID stock plummeting 64.30% in the past year due to production hiccups, the delivery of a mere 6,000 vehicles in the previous year marks a 32% nosedive in Q4 deliveries year on year. This slump arrives at a tumultuous time for the EV market, exacerbating Lucid’s woes.

Analysts at Seeking Alpha project a date as distant as 2029 for Lucid to turn profitable, lagging far behind its competitors in racing towards a robust EV lineup. Targeting a paltry 9,000 vehicles by 2024 seems like a drop in the bucket, especially when considering the hefty losses Lucid accrues with every vehicle sold. During Q4 alone, the company hemorrhaged $653.8 million in 2023, adding up to a staggering $2.8 billion in overall losses.

Storm Clouds Gather Over New York Community Bancorp (NYCB)

New York Community Bancorp (NYSE:NYCB) finds itself navigating treacherous waters amidst a tempest of internal turmoil and leadership turbulence. The bank’s unanticipated spike in loan loss provisions and subsequent dividend slash in January triggered a freefall, with NYCB stock shedding over 65% in the last three months. The plot thickened with the abrupt exit of CEO Thomas Cangemi and the appointment of Executive Chairman Alessandro DiNello against a backdrop of internal control lapses.

The rough waters for New York Community Bancorp deepened with a Q4 loss that surpassed expectations by $2.4 billion, culminating in a $2.7 billion deficit. This fiscal debacle has dealt a severe blow to investor confidence. While the bank might dodge an outright collapse, the remedial steps taken, including seeking brokered deposits or raising fresh equity, could further cloud its financial outlook and stock performance. In the face of these lingering uncertainties and the murky roadmap ahead, investors would be wise to heed caution.

Proceed with Caution: AMC Entertainment’s Financial Rollercoaster

AMC Entertainment (AMC)

Investors, buckle up as we delve into the turbulent journey of AMC Entertainment (NYSE: AMC). The past year saw AMC’s stock plummet by over 90%, serving as a stark indicator of the challenges gripping the movie theatre chain operator. The primary culprits behind this downward spiral are lackluster box office performances and the seismic shifts caused by streaming platforms in the entertainment realm.

The Reality Beneath the Surface

Source: rblfmr / Shutterstock.com

In a turn of events, AMC’s latest quarterly report seemed to paint a brighter picture. The company experienced an 11.5% surge in Q4 sales, reaching $1.1 billion, exceeding analysts’ estimates. Additionally, AMC managed to narrow its net loss, shrinking from $287.7 million to $182 million. However, a closer examination reveals a concerning narrative beneath these superficial gains. The financial upturn was primarily fueled by two major event films – “Taylor Swift: The Eras Tour” and “Renaissance: A Film by Beyonce.” This heavy reliance on a couple of blockbuster releases underscores the fragility of AMC’s path to recovery.

A Precarious Position

AMC’s financial stability is further called into question by its alarming debt-to-equity ratio, which currently stands at negative 4.95, indicating negative shareholder equity. This precarious position amplifies the risks associated with investing in AMC and highlights the urgent need for a sustainable and diversified revenue stream.

Disclosure: At the time of publication, the writer, Muslim Farooque, did not hold any positions in the securities discussed in this article. The views expressed are solely those of the author and do not necessarily reflect the views of InvestorPlace.