The Uphill Battle Ahead: Canadian Pacific Kansas City (CP) faces a rocky path ahead due to its financial instability stemming from soaring operating expenses and a liquidity crunch. With fuel costs running high, the company’s financial health is under undue pressure, exacerbated by dwindling cash reserves that hinder its ability to meet obligations.

Let’s uncover the layers of this financial conundrum.

Navigating Southward Earnings Estimates

The Zacks Consensus Estimate for CP’s current-quarter earnings has taken a 2.70% dip in the past 60 days. Further widening the gap, the consensus estimate for the current year shows a 0.62% decline. These downward revisions speak volumes of brokers’ lack of optimism in the stock’s future potential.

Unimpressive Rankings and Price Performance

CP presently holds a concerning Zacks Rank #4 (Sell). Additionally, its Value Score lingers at an uninspiring ‘F,’ reflecting its dwindling attractiveness. An unpalatable cocktail, indeed.

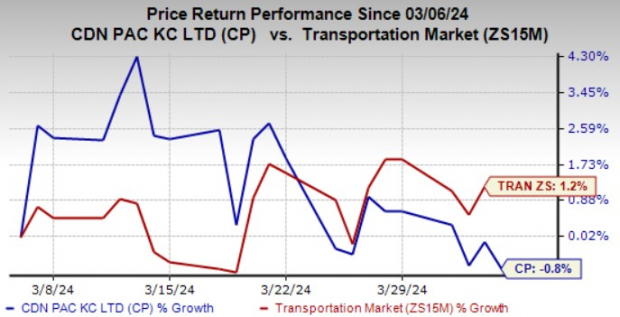

To make matters worse, Canadian Pacific KC’s stock has trailed its sector’s growth, dropping by 0.8% over the last 30 days while its sector saw a 1.2% surge.

Image Source: Zacks Investment Research

Overcoming Headwinds

Besides the financial quagmire, CP is grappling with heavy leverage. While the company saw a slight uptick in cash reserves, its long-term debt ballooned from C$18.14 billion to C$19.35 billion in just one year. Moreover, operating costs ballooned by a staggering 48.9% due to a 20% spike in fuel expenses in 2023, further straining its financial muscle.

The company’s ambitious capital expenditure plans, with a C$2.75 billion earmarked for 2024, might further constrict its ability to generate free cash flow.

Bearish Industry Outlook

Compounding CP’s woes is its industry’s dismal Zacks Industry Rank of 182 out of more than 250 groups. Holding a spot in the bottom 28% of Zacks Industries, the industry’s poor performance directly impacts CP’s market trajectory.

As studies suggest, a mediocre stock in a robust industry often outshines a strong stock in a feeble sector. Hence, understanding the industry’s landscape emerges as a key consideration for investors.

Exploring Alternatives: Stocks to Watch

Investors eyeing the broader transportation sector might find solace in stocks like Air Lease (AL) and SkyWest (SKYW). AL’s consistent track record of beating earnings estimates, coupled with a Zacks Rank #2 (Buy), paints a promising picture. Strong fleet growth and sales activity are propelling Air Lease’s revenues.

Meanwhile, SKYW proudly wears the Zacks Rank #1 (Strong Buy) badge. With a more than 100% expected earnings growth for 2024 and a remarkable four-quarter earnings surprise history, SkyWest’s upward trajectory is hard to miss.

Top 5 ChatGPT Stocks Revealed

Zacks Senior Stock Strategist, Kevin Cook, unveils 5 potential stocks with sky-high growth in the Artificial Intelligence sector. As the AI industry gears up for a seismic impact, investing in the future wave is both prudent and promising.

Seize the chance to step into the future of automation – where impeccable responses and insightful challenges redefine human-machine interactions. Automation, indeed, paves the way for miraculous achievements beyond the realm of mundane tasks!

Download Free ChatGPT Stock Report Right Now >>

To delve further into this analysis on Zacks.com, follow this link.

Remember, the insights shared here are subjective opinions and do not necessarily mirror Nasdaq, Inc.’s views.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.