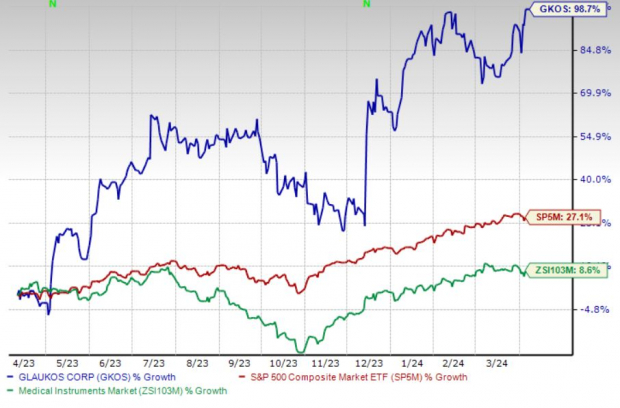

Shares of Glaukos Corporation GKOS surged to a new 52-week high of $97.77 on Apr 5, later closing slightly lower at $96.77. Over the past year, this Zacks Rank #3 (Hold) stock has outpaced the industry’s growth soaring 98.8%, while the S&P 500 recorded a 27.1% increase.

Glaukos’ projected growth rate of 3.9% for 2024, albeit lower than the industry’s 13.5%, hasn’t deterred investors amidst the recent uptrend. The company’s consistent earnings beat against the Zacks Consensus Estimate highlights resilience amidst market fluctuations, reflecting an average surprise of 1.3% over the previous four quarters.

Bolstered by a dominant presence in its flagship product, iStent, Glaukos continues its upward trajectory. The stock’s rally was further fueled by a stellar performance in the fourth quarter of 2023, indicating a promising future amid prospects of robust business growth. However, challenges like vendor uncertainties and setbacks in its pipeline loom over Glaukos’ otherwise stellar performance.

Image Source: Zacks Investment Research

Diving deeper into the company’s key growth drivers:

Strength in iStent

Investor optimism surrounding Glaukos’ iStent remains high. The iStent procedure enjoys reimbursement by Medicare and major private payors in the U.S. and is commercially available across several global markets. Surgeon feedback on the three-stent solution indicates a positive safety profile, further enhancing its market position.

Robust Business Potential also underscores Glaukos’ growth trajectory. Anticipation for sustained growth across international markets and the success of iStent infinite’s commercial launch in 2023 bode well for the company, indicating a promising future.

Strong Q4 Results in 2023 have not gone unnoticed. Investors are buoyed by Glaukos’ impressive year-over-year top-line and segmental performances, reinforcing market confidence.

Challenges Ahead

Pipeline Setbacks: Glaukos’ pipeline, while promising, has faced hurdles in clinical developments and regulatory processes. Adverse outcomes in these aspects could impact the company’s stock price, signaling a cautionary note to investors. The FDA’s denial of approval for the MicroShunt is a recent setback that necessitates the exploration of alternative pathways for regulatory approval in the U.S.

Vendor Uncertainty: Dependency on a limited number of suppliers for critical components introduces risk. Any disruptions in the supply chain could adversely affect Glaukos’ operations, necessitating a proactive stance to mitigate potential risks.

Noteworthy Alternatives

While Glaukos shines, other key performers in the medical industry merit attention. Companies like DaVita Inc., Cardinal Health, Inc., and LeMaitre Vascular, Inc. present intriguing opportunities for investors seeking diverse avenues for growth.

DaVita, armed with a Zacks Rank #1 (Strong Buy), projects long-term growth of 12.1%, having consistently surpassed earnings estimates over the past four quarters. Cardinal Health and LeMaitre Vascular are also promising entities with favorable long-term growth estimates, offering a compelling investment landscape.

To peruse the potential “home runs” in the stock market, investors can explore Zacks’ recommendations, uncovering hidden gems that might alter their investment fortunes positively. Expanding horizons beyond Glaukos to include other thriving companies could diversify investment portfolios, unlocking fresh possibilities in the dynamic financial markets.

If you seek the latest insights from Zacks Investment Research to refine your investment strategies, visit Zacks’ platform to access comprehensive reports and recommendations, guiding your financial decisions effectively in the ever-evolving market landscape.

The perspectives shared are that solely of the author and may not align with Nasdaq, Inc.’s views and opinions.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.