Seeking to bolster your retirement fund with a robust growth stock? Merely selecting a company witnessing a meteoric rise in its market value won’t suffice. Key qualities define optimal choices, including unparalleled growth potential and a loyal customer base that frequently engages with the brand.

One standout contender fitting this bill is none other than Amazon (NASDAQ: AMZN). Here are three compelling reasons to consider investing.

The Power of Repeat Revenue

Amazon boasts a massive pool of retail customers, with millions leveraging their Prime memberships for frequent purchases. In the U.S. alone, Statista projects 167 million Prime members, with a global count topping 200 million. Notably, about 42% of U.S. members make between two to four monthly transactions. As of June 30, 2024, Amazon’s revenue stood strong at a whopping $604 billion with $42 billion sourced from subscriptions and $237 billion from online sales.

Additionally, Amazon reaps repeat revenue via its Amazon Web Services (AWS), the leading global cloud provider. Despite contributing less than 20% to overall revenue, AWS stands out as Amazon’s most lucrative segment, accounting for approximately two-thirds of operating profit.

Abundant Growth Possibilities

Amazon’s online marketplace and cloud services hold vast expansion opportunities, promising sustained growth over the long haul.

The global e-commerce sector, predicted by eMarketer to reach $6 trillion in 2024 and set to soar to $8 trillion by 2028, offers a fertile ground for Amazon to continue its upward trajectory.

Meanwhile, in the cloud domain, AWS exhibited 19% year-over-year revenue growth last quarter, tallying $98 billion in trailing-12-month revenue. However, with roughly 80% of enterprise data yet to migrate to the cloud, AWS showcases substantial room for growth. The potential for AWS to become Amazon’s primary revenue driver hints at amplified profitability and upward mobility for shareholders.

Promising Upside for Investors

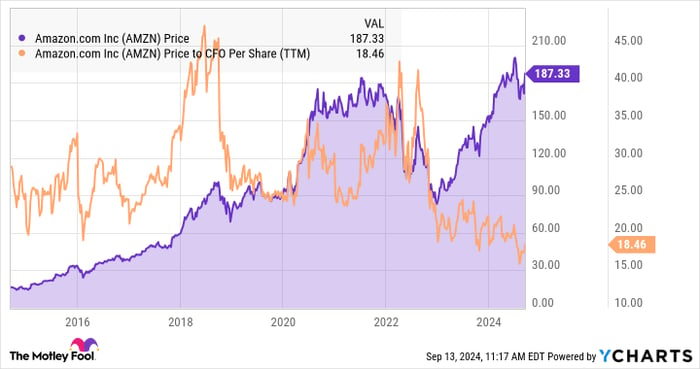

Amazon often appears overvalued based on price-to-earnings ratios, reflecting the company’s focus on long-term cash flow maximization over short-term earnings per share gains.

Assessing Amazon’s cash from operations (CFO) per share, the stock currently trades at a price-to-CFO ratio of 18.4. Despite doubling in value over the past five years, Amazon stands at its lowest P/CFO ratio in a decade.

With the trajectory of Amazon’s cash from operations mirroring share price growth, and the untapped potentials in e-commerce and cloud services, Amazon’s stocks present compelling growth prospects.

Concluding Thoughts

For the savvy investor with limited capital, Amazon’s current position slightly below its recent high of $201 offers an opportune moment to dive in.

Before plunging into the Amazon stock pool, reflect on this:

The Motley Fool Stock Advisor recently unveiled their top 10 stock picks for investors, bypassing Amazon. However, the stocks that made the cut exhibit the potential for substantial returns in the foreseeable future.

Noteworthy is the narrative of Nvidia making the list back in April 2005, demonstrating a meteoric growth from a $1,000 investment to $729,857.

*Stock Advisor has significantly outperformed the S&P 500 since 2002, offering invaluable insights, regular analyst updates, and bimonthly stock picks to their subscribers.

Could the next big win be among the 10 stocks they’ve spotlighted?

*Stock Advisor returns as of September 9, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, serves on The Motley Fool’s board of directors. John Ballard holds no positions in stocks mentioned. The Motley Fool advocates for and holds positions in Amazon. The Motley Fool stands by its disclosure policy.

Opinions shared here represent the author’s and not Nasdaq, Inc.’s views and opinions.