Devon Energy Set to Announce Earnings Amid Mixed Market Performance

Devon Energy Corporation (DVN), with a market capitalization of $25.7 billion, operates as an independent energy company. The firm, headquartered in Oklahoma, specializes in the exploration, development, and production of oil, natural gas, and natural gas liquids in significant U.S. basins such as the Delaware, Eagle Ford, Anadarko, Williston, and Powder River. Investors are eagerly awaiting the company’s fiscal Q3 earnings announcement, scheduled for after the market closes on Tuesday, Nov. 5.

Profit Predictions and Historical Performance

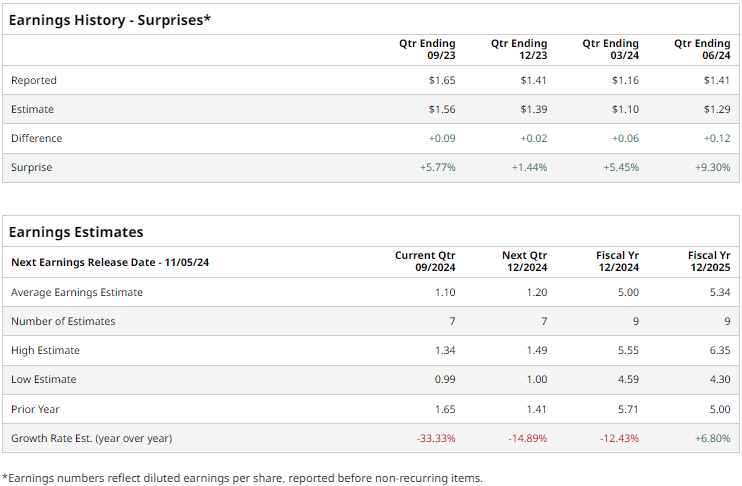

Analysts forecast that DVN will report a profit of $1.10 per share for the upcoming quarter, which reflects a notable decrease of 33.3% from $1.65 per share registered in the same quarter last year. Nonetheless, DVN has a track record of surpassing Wall Street’s earnings forecasts, having exceeded the consensus EPS estimate by 9.3% in the last quarter.

Future Earnings Expectations

Looking ahead to fiscal 2024, projections suggest that DVN will achieve an EPS of $5, indicating a decrease of 12.4% from $5.71 in fiscal 2023. However, a recovery is anticipated in fiscal 2025, with expectations of a 6.8% growth to reach an EPS of $5.34.

Stock Performance and Market Trends

This year, shares of Devon Energy have underperformed compared to broader markets, experiencing a decline of 10.2%. In contrast, the S&P 500 Index ($SPX) has gained nearly 23%, while the Energy Select Sector SPDR Fund (XLE) has returned 7.8% year-to-date.

Earnings Release and Analyst Ratings

After its Q2 earnings release on Aug. 6, shares of Devon Energy rose by 2.8%. This increase was fueled by better-than-expected adjusted EPS of $1.41 due to higher production volumes and effective cost management. The company also raised its full-year 2024 production guidance without increasing capital expenditures, showcasing its operational efficiency. Furthermore, Devon expanded its share repurchase program by 67% to $5 billion, boosting investor confidence. However, the stock faced a downturn in September, falling due to a 7.3% drop in oil prices, largely driven by apprehensions over potential OPEC production increases and a global economic slowdown impacting cash flow.

Analysts’ Outlook

The consensus among analysts on DVN stock remains cautiously optimistic. Out of 25 analysts, 14 recommend a “Strong Buy,” two give a “Moderate Buy,” and nine suggest a “Hold” rating. This outlook is slightly less bullish than three months ago when 15 analysts recommended a “Strong Buy.” The average analyst price target for DVN stands at $52.96, indicating a potential upside of 30.3% from current prices.

More Stock Market News from Barchart

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are for informational purposes only. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.