Foot Locker Reports Mixed Q3 Results Amid Market Challenges

Foot Locker, Inc. (FL) has released its third-quarter fiscal 2024 results, revealing that both its earnings and revenues fell below expectations set by the Zacks Consensus Estimate. Although revenue dropped, earnings increased compared to the same quarter last year.

The company experienced positive trends in comparable sales and expanded gross margins. However, its third-quarter results were impacted by weaker consumer spending following the Back-to-School season and heightened promotional activities. Nevertheless, progress continues on its Lace Up Plan, including partnerships with Nike, Jordan Brand, and the Chicago Bulls to enhance customer experiences.

Initial trends in November were sluggish, but a notable surge occurred during Thanksgiving week. Due to decreased demand and a competitive pricing landscape, the company has adjusted its full-year projections. Foot Locker plans to focus on growth through new store designs, an improved digital platform, and increased customer engagement, with ambitions for an 8.5-9% EBIT margin by 2028. In the last three months, FL shares have declined 11.9%, in contrast to the industry’s impressive 22.4% growth.

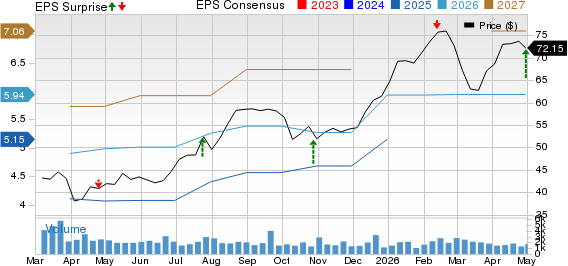

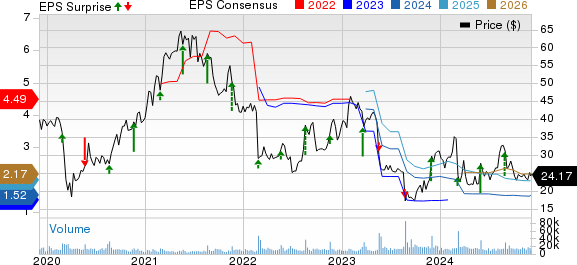

Overview of Foot Locker’s Price, Consensus, and EPS Surprise

Foot Locker, Inc. price-consensus-eps-surprise-chart | Foot Locker, Inc. Quote

Details of Foot Locker’s Q3 Performance

Foot Locker reported adjusted earnings of 33 cents per share, which fell short of the Zacks Consensus Estimate of 39 cents. However, this amount rose from adjusted earnings of 30 cents in the same period last year.

Total revenues reached $1,961 million, down 1.4% from the previous year. When considering foreign currency fluctuations, sales decreased by 2.2%. This total also missed expectations, as analysts predicted revenues of $2,001 million.

Comparable sales saw a rise of 2.4% year over year, primarily fueled by a 2.8% uptick in sales at global Foot Locker and Kids Foot Locker stores. Additionally, Champs Sports and WSS both experienced positive comparable sales growth, reporting increases of 2.8% and 1.8%, respectively.

Examining FL’s Margins

Foot Locker’s gross margin rate saw an increase of 230 basis points. This gain was mainly attributed to reduced markdown levels, while analysts had anticipated a growth of 280 basis points for the quarter.

On the other hand, selling, general and administrative (SG&A) expenses as a percentage of sales increased by 210 basis points compared to last year. This rise stems from investments in technology and brand development but was partially countered by savings from an ongoing cost-optimization initiative. Analysts had projected an expansion of 200 basis points in SG&A expenses.

Image Source: Zacks Investment Research

Update on Foot Locker’s Store Operations

During the third quarter, Foot Locker opened 10 new stores while closing 24 locations. The company also remodeled or relocated 20 stores and updated 167 existing stores to align with their latest design standards.

As of November 2, 2024, Foot Locker operates 2,450 stores across 26 countries, including locations in North America, Europe, Asia, Australia, and New Zealand. There are also 214 franchised stores functioning in the Middle East and Asia.

Financial Overview for Foot Locker

At the end of the fiscal third quarter, Foot Locker had cash and cash equivalents of $211 million. Its long-term debt and finance lease obligations total $440 million, while shareholders’ equity stands at $2.87 billion. Merchandise inventories were valued at $1.74 billion, reflecting a 6.3% decrease from the previous year.

Future Outlook for Foot Locker

Looking ahead, Foot Locker’s fourth-quarter guidance for fiscal 2024 indicates a revenue decline expected between 3.5% and 1.5%. Comparable sales are projected to grow by 1.5% to 3.5%. Gross margin is anticipated in the range of 29-29.2%, with the SG&A rate estimated to fall between 22.3% and 22.5%, due to ongoing investment expenditures. The EBIT margin forecast for the fourth quarter lies between 4.5% to 5%, while adjusted EPS is expected to be between 70 cents and 80 cents.

For the full fiscal year of 2024, Foot Locker expects a revenue decline of 1.5% to 1%, revising earlier guidance that called for a drop of 1% or potential growth of 1%. The range for comparable sales growth has tightened to 1-1.5% compared to a prior range of 1-3%.

The company has also adjusted its gross margin expectations, lowering them to 28.7-28.8% from an earlier projection of 29.5-29.7%. Meanwhile, the SG&A rate forecast has improved slightly to 24-24.1%, indicating effective cost management despite ongoing investments. The EBIT margin guidance for the entire year has been adjusted down to 2.3-2.5%, compared to the previous estimate of 2.8-3.2%. Adjusted EPS guidance has shifted to a range of $1.20-$1.30, down from $1.50-$1.70. Capital expenditures expectations are set at $270 million, slightly less than the previous estimate of $275 million, while adjusted capital expenditures are now projected to be $320 million instead of $330 million, highlighting a commitment to technology investments.

Solid Alternatives in Retail

Investors may consider looking at other stocks that have shown better performance, including The Gap, Inc. (GAP), Abercrombie & Fitch Co. (ANF), and Steven Madden, Ltd. (SHOO).

The Gap is a well-known international specialty retailer providing a wide array of clothing, accessories, and personal care items, currently rated as a Zacks Rank #1 (Strong Buy). It shows promising growth potential with a Zacks Consensus Estimate indicating a 40% increase in fiscal 2025 earnings and 0.8% growth in sales compared to fiscal 2024.

Abercrombie specializes in high-quality casual apparel and currently holds a Zacks Rank of 2 (Buy). Its fiscal 2025 earnings and sales are projected to grow by 67.5% and 14.9%, respectively, over fiscal 2024 figures.

Steven Madden, known for its fashionable footwear designs and marketing, also carries a Zacks Rank of 2. Its estimates for 2024 point to an 8.6% increase in earnings and a 13.6% rise in sales compared to last year.

Zacks’ Research Chief Highlights Top Stock Picks

Our

Expert Analysts Predict 5 Stocks With 100% Growth Potential

A new report reveals the top five stocks expected to rise by 100% or more in the upcoming months. Among these, Sheraz Mian, Director of Research, has singled out one stock anticipated to achieve the greatest increase.

This leading investment choice is from a pioneering financial firm experiencing rapid growth. With a customer base exceeding 50 million, the company offers an array of innovative solutions. While past selections haven’t guaranteed success, this stock may significantly outshine previous Zacks picks, such as Nano-X Imaging, which soared by +129.6% in just over nine months.

Discover Our Top Stock and 4 Competitors

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

Foot Locker, Inc. (FL): Free Stock Analysis Report

The Gap, Inc. (GAP): Free Stock Analysis Report

Steven Madden, Ltd. (SHOO): Free Stock Analysis Report

Click here to read this article on Zacks.com.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.