Nvidia’s Strong Results Face Share Pressure After Q4 Earnings

With Nvidia’s (NVDA) quarterly release completed, the 2024 Q4 reporting cycle for the broader Mag 7 group has officially wrapped up. Most members of this elite club reported solid growth in both revenue and earnings, yet not all enjoyed a positive reaction from the market.

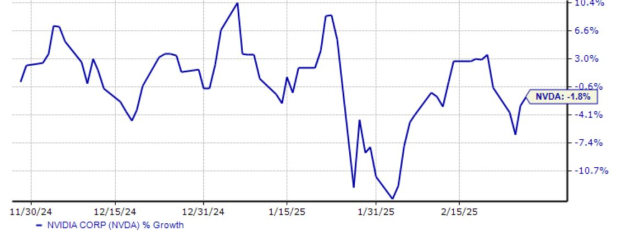

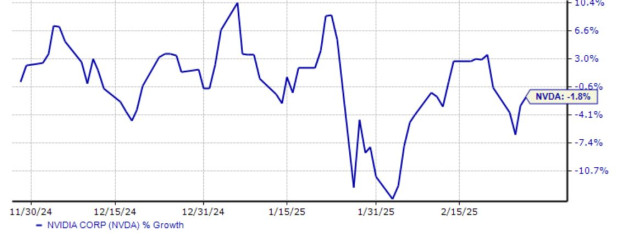

Nvidia shares also experienced pressure following their earnings report. Over the past three months, the stock has declined roughly 2%, showing limited overall positivity during this period.

Image Source: Zacks Investment Research

This raises an important question: Were Nvidia’s earnings disappointing? Let’s analyze the results more deeply.

NVDA Results Reflect Healthy Demand

Nvidia reported quarterly revenues of $39.3 billion, which marks a 78% year-over-year increase and sets a new record for the company. The adjusted earnings per share (EPS) of $0.89 indicated a 71% growth year-over-year, surpassing the consensus estimate by nearly 6%.

This substantial growth aligns with the ongoing strong demand for Nvidia’s products, a trend that has persisted in recent quarters. The Data Center segment performed particularly well, standing out as a key highlight of the earnings report.

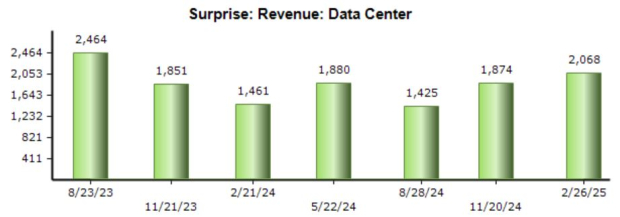

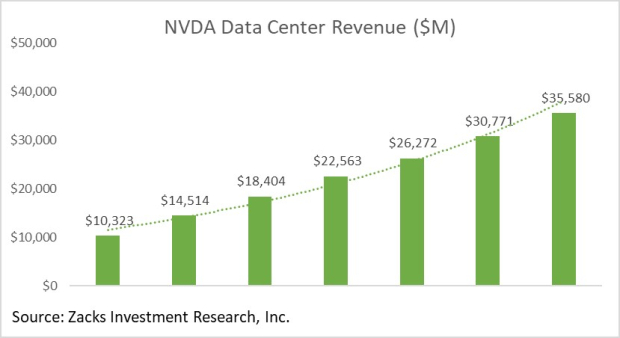

Data Center revenue reached a record $35.6 billion, a 90% year-over-year increase and a 16% bump from the previous quarter. This result not only exceeded our consensus estimate by $2.0 billion but also continued a trend of significant earnings surprises for the segment.

Image Source: Zacks Investment Research

There were notable developments regarding Blackwell, the successor to the Hopper architecture. CEO Jensen Huang commented on Blackwell’s impact:

“We’ve successfully ramped up the massive-scale production of Blackwell AI supercomputers, achieving billions of dollars in sales in its first quarter. AI is advancing at light speed as agentic AI and physical AI set the stage for the next wave of AI to revolutionize the largest industries.”

Below is a quarterly chart illustrating Nvidia’s Data Center sales over the last seven periods.

Image Source: Zacks Investment Research

The demand for Blackwell remains robust, which is likely to persist as companies increasingly invest in AI technologies. Despite this strong demand, Nvidia shares have dipped 2% over the past three months, trailing the performance of the S&P 500 index.

Relative to historical values, Nvidia shares are not overly expensive. The current forward earnings multiple of 30.6X for the next twelve months is significantly lower than its five-year median, and only a fraction of the five-year peak of 106.3X. Furthermore, the PEG ratio stands at 1.5X, again well below historical standards.

It’s important to remember that share prices were much higher during 2020 and 2021, before the rise of the AI trend that has since captivated the market.

Image Source: Zacks Investment Research

Nvidia forecasts sales of $43.0 billion (plus or minus 2%) for its next quarter, demonstrating a continued trajectory of growth.

Putting Everything Together

While the immediate market reaction to Nvidia’s earnings was negative, the overall results were solid. Nvidia continues to be a frontrunner in the AI sector, driven by its strong Data Center performance.

The share price presents a compelling opportunity for investors seeking to capitalize on the ongoing AI trend. Forecasts remain optimistic, buoyed by positive statements from CEO Jensen Huang regarding the Blackwell architecture and overall demand for computational resources.

Although the stagnant share price over the recent months may be frustrating to some investors, this pause was likely necessary after the significant gains over the previous years.

5 Stocks Set to Double

These stocks were handpicked by a Zacks expert as their top favorites likely to gain +100% or more in 2024. Previous recommendations have seen returns of +143.0%, +175.9%, +498.3%, and +673.0%.

Many of these stocks are currently under the radar of Wall Street, offering an excellent opportunity to invest early.

Today, See These 5 Potential Home Runs >>

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.