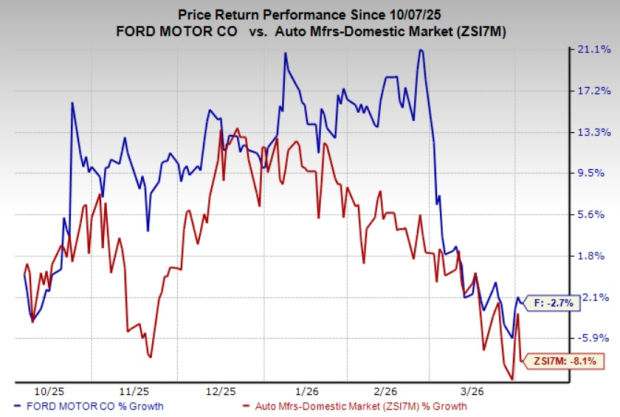

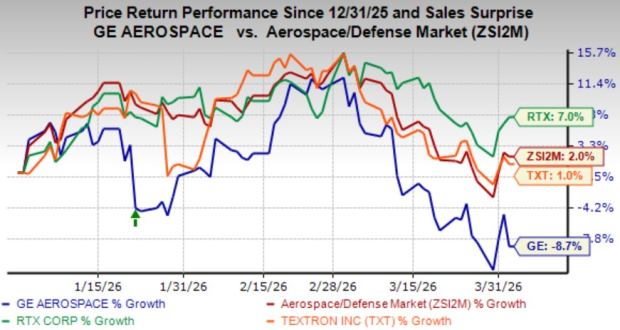

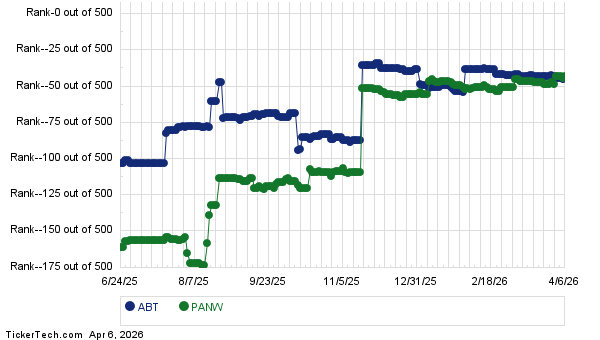

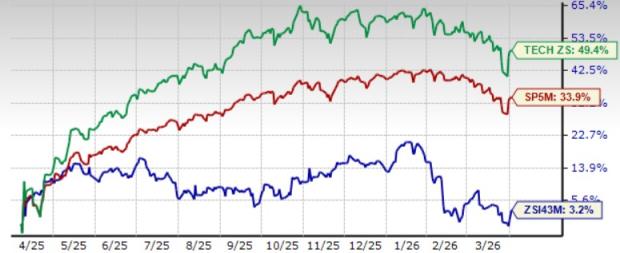

AMD’s 3,240% Growth Transforming Semiconductor Market Dynamics

Advanced Micro Devices‘ (NASDAQ: AMD) stock has increased by an impressive 3,240% over the last decade. Once a challenger to industry giants Intel and Nvidia in x86 CPUs and discrete GPUs, AMD has successfully pivoted its business strategy since Lisa Su became CEO in 2014.

Under Su’s leadership, AMD revamped its PC CPU designs, increased custom accelerated processing units sales for gaming consoles, and offered competitive GPUs at lower prices. The company also introduced high-performance CPUs and GPUs tailored for AI-focused data centers.

Considering an investment of $1,000? Our analysts have identified the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

AMD’s Revenue Growth and Future Projections

From 2014 to 2024, AMD’s revenue experienced a compound annual growth rate (CAGR) of 17%. The company returned to profitability in 2018, with earnings per share (EPS) growing at a CAGR of 21% over the next six years. This growth stemmed from innovative chip designs, a partnership with Taiwan Semiconductor Manufacturing, and increased market share against Intel, which faced ongoing supply issues and delays in the x86 CPU sector.

Analysts predict AMD’s revenue and EPS will continue to grow at CAGRs of 20% and 73%, respectively, from 2024 to 2027. This growth is expected to be aided by the recovery of the PC market and rising demand for data center CPUs and GPUs. If AMD maintains a trailing earnings ratio of 30 by the end of 2027, its stock price could increase nearly 50%, elevating its market capitalization from $175 billion to $260 billion. However, rival chipmakers could potentially outpace AMD’s performance.

1. Arm Holdings: A Contender

The first contender is Arm Holdings (NASDAQ: ARM), currently valued at $144 billion. Arm specializes in designing energy-efficient chips for mobile devices, automobiles, IoT equipment, and various electronics. Its chip designs are licensed by many manufacturers, accounting for about 99% of the premium smartphones in the market.

Arm primarily earns revenue through patent royalties and licensing fees. The company has seen substantial growth due to the high demand for its AI-optimized Armv9 chips, which are used in smartphones, cloud computing, and automotive sectors.

This year, Arm plans to introduce its first-party data center CPUs, produced by a third-party foundry like TSMC, and has already partnered with Meta Platforms as its initial client. This move could attract additional major companies away from AMD and Intel’s data center CPU offerings.

From fiscal 2024 through fiscal 2027, analysts forecast Arm’s revenue and EPS growth rates of 23% and 83%. Despite appearing pricey, trading at 469 times its projected fiscal 2024 earnings and 45 times trailing sales, maintaining its high-growth valuations could enable Arm to surpass AMD’s market cap.

2. Micron Technologies: A Strong Player

Micron Technologies (NASDAQ: MU) ranks as one of the leading memory chip manufacturers, currently valued at $104 billion. Although it isn’t the largest in the sector, Micron produces chips that offer higher density than its competitors.

Micron’s performance reflects the cyclical nature of the memory chip industry. Its most recent downturn occurred in 2023, driven by a slowdown in the PC market, reduced 5G smartphone upgrades, and prioritization of AI-oriented GPU purchases over memory chip acquisitions. Consequently, Micron saw a 49% revenue decline and reported a net loss for fiscal 2023 (ending August 2023).

However, in fiscal 2024, the company rebounded with a 62% revenue increase, returning to profitability. This recovery is attributed to stabilizing PC and smartphone markets and growing sales of solid-state drives and high-bandwidth memory chips necessary for AI applications.

Looking ahead to fiscal 2024 through fiscal 2027, analysts predict Micron’s revenue and EPS will grow at CAGRs of 21% and 150%. Currently trading at 15 times this year’s earnings, if Micron meets these projections, its stock price could nearly increase by 80% to $165, boosting its market cap to about $185 billion. Alternatively, if evaluated at a premium of 25 times earnings, the stock price could approach $275, raising its market cap to over $300 billion.

Investment Potential Among Top Chipmakers

While it is intriguing to consider whether Arm and Micron may surpass AMD in market valuation, investors should not be overly concerned with these comparisons. Each of these chipmakers holds significant potential and could emerge as worthwhile investments in the next two years.

Opportunity Alert: Don’t Miss Out

Feeling like you’ve missed out on lucrative stocks? There is an opportunity now that you won’t want to ignore.

Occasionally, our team of analysts identifies companies for their “Double Down” stock recommendations, suggesting they are on the verge of significant gains. If you fear you have already missed your investment chance, now may be the best time to act.

Consider these exceptional returns:

- Nvidia: If you had invested $1,000 in 2009 when we issued a double down, you’d have $340,411!

- Apple: If you had invested $1,000 in 2008, you’d have $45,570!

- Netflix: If you had invested $1,000 in 2004, you’d have $533,931!

Currently, we are issuing “Double Down” alerts for three promising companies—a chance you won’t want to miss.

Learn more »

*Stock Advisor returns as of February 24, 2025

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Leo Sun holds positions in Meta Platforms. The Motley Fool has investments in and recommends Advanced Micro Devices, Intel, Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing, as well as a recommendation for shorting February 2025 $27 calls on Intel.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.