Market Eases After Strong Employment Data Spurred Fed Caution

The S&P 500 Index ($SPX) (SPY) has rebounded in afternoon trading, up by +0.74%. The Dow Jones Industrials Index ($DOWI) (DIA) follows with a rise of +0.65%, while the Nasdaq 100 Index ($IUXX) (QQQ) has increased by +0.86%.

Fed’s Cautious Approach Affects Market Sentiment

During a midday speech on Friday, Federal Reserve Chairman Jerome Powell indicated the Fed is taking a cautious stance before making any decisions regarding policy easing.

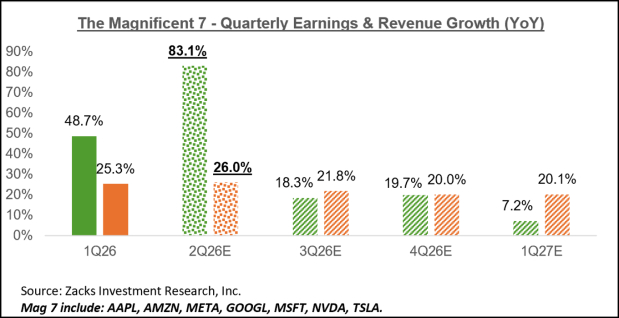

The stock indexes had earlier turned lower due to a decline in the so-called Magnificent Seven stocks. Additionally, ongoing economic uncertainties, largely stemming from the Trump administration’s trade policies and a recent US payroll report showing an unexpected rise in the unemployment rate, have impacted market performance.

Labor Market Surprises with Unexpected Unemployment Increase

Today’s labor data revealed that nonfarm payrolls for February increased by +151,000, falling short of expectations which had anticipated a rise of +160,000. Additionally, the January figures were revised lower from +143,000 to +125,000. The unemployment rate unexpectedly increased by +0.1% to 4.1%, signaling a labor market softer than expected, while expectations had estimated a steady rate of 4.0%.

Average hourly earnings in the US also grew to a year-over-year rate of 4.0%, slightly below the anticipated 4.1% but up from a revised 3.9% in January.

Market Reactions to Fed Officials’ Comments

Comments from Fed officials have also recently influenced market conditions. Atlanta Fed President Raphael Bostic suggested keeping interest rates unchanged until late spring due to uncertainty about the economy’s trajectory affected by President Trump’s policies. Meanwhile, Fed Governor Michelle Bowman remarked that the neutral rate—the level where Fed policy neither encourages nor restricts economic activity—has likely risen since the Covid-19 pandemic.

Trade Policies Continue to Fuel Economic Concerns

Concerns that US tariffs might ignite a global trade war pose additional bearish pressures on the market. Earlier this week, President Trump imposed a 25% tariff on Canadian and Mexican goods and raised the tariff on Chinese goods to 20%. However, he has provided a one-month exemption for US automakers and goods complying with the United States-Mexico-Canada Agreement (USMCA), stressing that he plans to introduce reciprocated tariffs on April 2.

Additionally, China’s recent trade data did not meet expectations, further dampening global growth prospects. For February, Chinese exports increased by only +2.3%, falling short of the expected +5.9%. Meanwhile, imports plunged by -8.4%, marking the most significant drop in nearly two years.

Global Market Overview

The chances of a -25 basis point rate cut at the upcoming Federal Open Market Committee meeting on March 18-19 are currently estimated at 4%.

International stock markets are also experiencing declines. The Euro Stoxx 50 index is down -1.10%. China’s Shanghai Composite Index dropped -0.25%, while Japan’s Nikkei 225 faced a significant decline of -2.17%, reaching a 5-1/2 month low.

Interest Rate Insights

In the interest rate market, June 10-year T-notes (ZNM25) are up +11 ticks, with the 10-year T-note yield decreasing by -1.9 basis points to 4.259%. The uptick in T-notes follows a less-than-expected labor report, along with positive momentum from European government bonds. Additionally, expectations for inflation have decreased, as demonstrated by the 10-year breakeven inflation rate dropping to a 2-1/4 month low of 2.313%.

Despite these movements, hawkish remarks from Fed officials like Atlanta’s Bostic and Bowman’s indications of a higher neutral rate have tempered gains in T-notes.

Meanwhile, European bond yields have decreased as well, with the 10-year German bund yield down -1.0 basis points to 2.823% and the 10-year UK gilt yield down -2.1 basis points to 4.639%.

Economic Reports and Market Movers

In other economic updates, Eurozone GDP for Q4 was revised upward to +0.2% quarter-over-quarter and +1.2% year-over-year, from previously reported figures of +0.1% and +0.9%, respectively. Conversely, German factory orders dropped by -7.0% month-over-month, significantly below the expected decline of -2.5% and representing the steepest drop in a year.

Comments from ECB Governing Council member Muller underscored the need for caution regarding potential future interest rate cuts, citing tariffs and defense spending’s potential effects on inflation. Swaps indicate a 65% chance of a -25 basis point rate cut at the ECB’s policy meeting on April 17.

US Stock Highlights

The broader market is being weighed down by the underperformance of the Magnificent Seven stocks today, with Meta Platforms (META), Amazon.com (AMZN), and Tesla (TSLA) each declining by over -2%. Microsoft (MSFT) and Alphabet (GOOGL) saw smaller declines of over -1% and -0.38%, respectively.

In contrast, chip stocks are showing strength. Broadcom (AVGO) leads with a +3% increase after announcing Q1 adjusted net revenue of $14.92 billion, surpassing expectations of $14.61 billion. Micron Technology (MU) and GlobalFoundries (GFS) are up more than +3%, while ARM Holdings Plc (ARM) and ASML Holding NV (ASML) also gained more than +2%. Additional notable performers include Lam Research (LRCX), Qualcomm (QCOM), ON Semiconductor (ON), and NXP Semiconductors NV (NXPI), all up more than +1%.

Energy stocks are showing upward momentum as WTI crude oil prices increased by over +2%. Consequently, Schlumberger (SLB) and Halliburton (HAL) are both up more than +3%. Chevron (CVX), Hess Corp (HES), Occidental Petroleum (OXY), and Devon Energy (DVN) have each gained over +2% as well.

The Gap (GAP) surged by more than +14% following Q4 comparable sales growth of +3.00%, exceeding predictions of +1.88%. Walgreens Boots Alliance (WBA) rose more than +7% after agreeing to a $10 billion acquisition by Sycamore Partners. Sandisk Corp (SNDK) gained over +6% after Cantor Fitzgerald initiated coverage with an overweight recommendation at a $60 price target. Zscaler (ZS) climbed by more than +1% after a buy rating upgrade from Bank of America Global Research with a target of $240.

Declining Stocks of Note

On the downside, HP Enterprise (HPE) leads S&P 500 losers, down more than -15% following a Q1 adjusted gross margin of 29.4%, falling short of the consensus of 31.2% and forecasting a full-year adjusted EPS of $1.70 to $1.90, below the consensus of $2.12. Cooper Companies (COO) is down more than -7% after reporting Q1 net sales of $964.7 million, missing the expected $982.1 million.

Costco Wholesale (COST) is down over -6%, leading losses in the Nasdaq 100 after reporting a Q2 EPS of $4.02, below the consensus of $4.11. Samsara (IOT) fell more than -13% after predicting total revenue for 2026 between $1.52 billion-$1.53 billion, just below the consensus of $1.53 billion. Air Lease (AL) also fell more than -2% after a downgrade from Bank of America Global Research, while Intuitive Machines (LUNR) plunged more than -20%, adding to a prior loss after concerns about its lunar lander orientation.

Upcoming Earnings Reports

(3/7/2025) Advantage Solutions Inc (ADV), Aemetis Inc (AMTX), Aldeyra Therapeutics Inc (ALDX), Cartesian Therapeutics Inc (RNAC), GCT Semiconductor Holding Inc (GCTS), Gencor Industries Inc (GENC), Genesco Inc (GCO), IGM Biosciences Inc (IGMS), Immersion Corp (IMMR), Mammoth Energy Services Inc (TUSK), National Beverage Corp (FIZZ), Ovid Therapeutics Inc (OVID), Preformed Line Products Co (PLPC), Savara Inc (SVRA), Silvercrest Asset Management G (SAMG), Valhi Inc (VHI), Werewolf Therapeutics Inc (HOWL), XOMA Royalty Corp (XOMA).

On the date of publication, Rich Asplund did not hold (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.