Investment Outlook: Comparing Nvidia and Palantir in AI Stocks

Nvidia (NASDAQ: NVDA) and Palantir Technologies (NASDAQ: PLTR) saw significant gains in 2024 due to rising demand for their artificial intelligence (AI) hardware and software solutions. However, the 2025 stock performance has deviated from this trajectory, showing different challenges for these two fast-growing companies.

Nvidia’s stock has declined nearly 14% in 2025, while Palantir has struggled after an initially strong year. Nevertheless, both companies remain well-positioned to take advantage of lucrative markets. Nvidia’s recent financial results highlight that demand for AI hardware continues to drive growth, whereas Palantir is seeing enhancements in its growth profile fueled by the rising need for generative AI software.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

When considering which of these two AI stocks to invest in, it’s critical to analyze their respective strengths. Let’s examine the prospects for each company.

The Case for Nvidia

Market skepticism surrounds Nvidia regarding its ability to maintain robust growth. Concerns stem from export controls on AI graphics processing units (GPUs), potential dips in AI infrastructure spending, and competition from custom processors developed by major tech firms aiming to lower costs.

Recent quarterly results, however, demonstrate solid demand for Nvidia’s AI chips. In the fourth quarter of fiscal 2025 (ending January 26), revenue surged 78% year over year to a record $39.3 billion, and adjusted earnings rose 71% year over year to $0.89 per share. These results surpassed Wall Street expectations.

Looking ahead, Nvidia anticipates revenue of $43 billion for the current quarter, reflecting a 65% increase from the previous year. The company may even surpass this expectation as it scales production of its latest Blackwell processors to meet increasing demand.

The versatility of the Blackwell processor may enhance Nvidia’s lead in the AI chip sector. Management highlighted on their earnings call that “Blackwell addresses the entire AI market from pretraining, post-training to inference across cloud, to on-premise, to enterprise.”

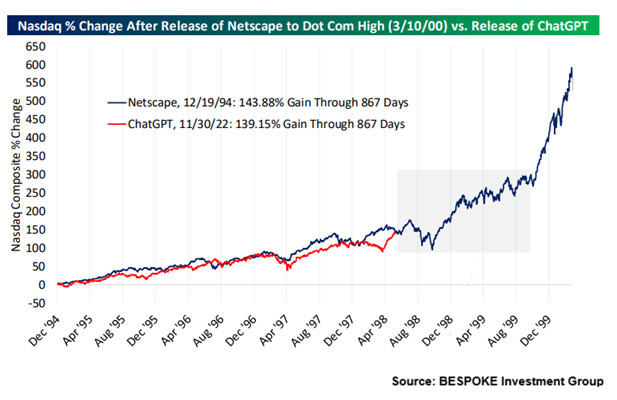

With the introduction of cost-effective reasoning models like DeepSeek’s R1, computing demand is poised for substantial increases. Nvidia claims that the Blackwell architecture is capable of processing requests 25 times faster and at a 20 times lower cost compared to the previous H100 processor. Consequently, Nvidia’s significant market share in AI chips, approximately 85%, is expected to hold strong.

This upward trend is mirrored in analysts’ revision of revenue growth expectations for the current and next two fiscal years.

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

Furthermore, Nvidia’s earnings are expected to grow by 50% in the ongoing fiscal year despite near-term pressure on margins as it increases Blackwell output. Management expects adjusted gross margins to return to the mid-70% range later this fiscal year, signaling further growth potential as production stabilizes.

The Case for Palantir Technologies

Palantir Technologies, a leading vendor of AI software platforms, operates in a rapidly growing market. According to IDC, the global AI software platforms market may expand from $28 billion in 2023 to $153 billion in 2028 at an impressive annual growth rate exceeding 40%.

This burgeoning market positively influences Palantir’s performance, with the company’s revenue growth accelerating to 29% in 2024, up from 17% the previous year. Given that Palantir’s revenue for last year was just under $2.9 billion, further growth appears promising as the AI software platforms market continues to expand.

Notably, Palantir has been signing new contracts at a pace that matches the anticipated growth of the AI software platforms sector. In the fourth quarter of 2024, Palantir reported a remarkable 40% year-over-year increase in its remaining deal value (RDV)—a metric reflecting the total value of unfulfilled contracts—reaching $5.4 billion.

This uptick is significant compared to the 22% year-over-year growth observed in RDV during the third quarter. Such growth indicates that Palantir is securing contracts faster than it can fulfill them, suggesting stronger revenue and earnings growth on the horizon.

Moving forward, Palantir’s revenue pipeline is likely to further improve as new customers tend to sign larger contracts over time, often benefiting from the efficiency of its Artificial Intelligence Platform (AIP). The company increased its customer count by 43% year over year in the previous quarter. As these new clients implement AIP in different areas, Palantir’s RDV should see increased growth.

Additionally, rising expenditures by existing customers are enhancing Palantir’s margins; its adjusted operating margin increased by 11 percentage points year over year last quarter. Consequently, Palantir’s adjusted earnings soared 64% in 2024 to $0.41 per share, with analysts predicting that the company will continue to deliver strong double-digit growth moving forward.

Comparing Investment Prospects: Palantir vs. Nvidia

Investors should note that Palantir Technologies (PLTR) is currently projected to experience moderate earnings growth in the coming year. Analysts predict that growth could be aided by its improving revenue pipeline and margin enhancements.

PLTR EPS Estimates for Current Fiscal Year data by YCharts

Market Analysis: Palantir Compared to Nvidia

While Nvidia provides investors opportunities in the lucrative AI hardware sector, Palantir focuses on benefiting from the swift adoption of generative AI software. Both companies could have a spot in a well-diversified portfolio. However, a significant concern arises from Palantir’s high valuation compared to Nvidia, which is growing at a quicker rate.

NVDA PE Ratio data by YCharts

This inflated valuation has led to concerns about Palantir’s stock potentially being overvalued, contributing to its recent pullback. Analysts forecast Palantir’s stock to appreciate by only 15% over the next year, with a median price target of $97. In contrast, Nvidia is anticipated to surge by 51% within the same timeframe.

Nvidia’s more attractive valuation may result in higher market rewards, given its faster expected earnings growth. This could help investors make decisions about which of these two AI stocks provides a better investment opportunity at present.

Is Nvidia a Smart $1,000 Investment Right Now?

Before deciding to invest in Nvidia, prospective buyers should consider this:

The Motley Fool Stock Advisor analyst team recently highlighted what they believe are the 10 best stocks to purchase at the moment, and Nvidia was not included in that list. The ten recommended stocks could yield significant returns in the upcoming years.

Reflecting on Nvidia’s past, if you invested $1,000 at the time they were recommended on April 15, 2005, your investment would be worth $690,624 today!*

Stock Advisor offers investors a clear strategy for success, including portfolio building tips, regular analyst updates, and two new Stock selections each month. To date, the Stock Advisor service has greatly outperformed the S&P 500 since 2002.* Join to access the latest top 10 list.

*Stock Advisor returns as of March 3, 2025

Harsh Chauhan has no position in any of the mentioned stocks. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.

The views expressed here are those of the author and do not necessarily reflect the views of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.