Investing Insights: Nvidia vs. Broadcom in AI Market

Both Nvidia (NASDAQ: NVDA) and Broadcom (NASDAQ: AVGO) have significantly benefited from major investments in artificial intelligence (AI) hardware. This surge in interest explains their impressive share price increases over the past couple of years.

Nvidia’s stock rose by over 280% in the last two years, while Broadcom saw gains of around 160% during that same timeframe. However, 2025 has not been as kind to these AI-focused stocks, as both companies experienced a notable pullback in their stock prices even after reporting strong revenue and earnings. Nvidia’s stock retreated nearly 18% this year, and Broadcom faced an even sharper decline of about 28%.

The drop in share prices is largely due to negative stock market sentiment driven by ongoing economic uncertainty, particularly from the tariff-induced trade war. In addition, the increasing likelihood of a U.S. recession has caused investors to become more risk-averse, prompting them to take profits in strongly performing stocks.

Despite this pullback, Nvidia and Broadcom’s share declines may present opportunities for savvy investors looking to add potential long-term winners to their portfolios. The AI market is still in its early growth stages and is projected to grow at an annual rate of 36% through 2030.

So, if you had to choose between these two AI stocks, which one should it be? Let’s explore further.

The Case for Nvidia

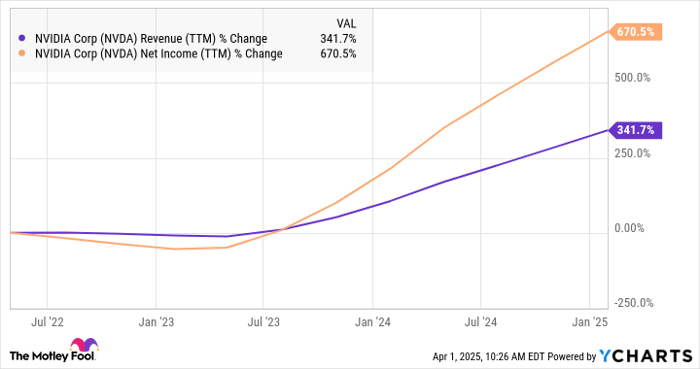

Nvidia played a pivotal role in the AI revolution three years ago by providing powerful data center graphics processing units (GPUs) that OpenAI used to train the popular chatbot, ChatGPT. The chip designer has become the preferred supplier of AI GPUs for various tech giants and governmental entities around the world, which has been reflected in its impressive revenue and earnings.

NVDA Revenue (TTM) data by YCharts

As of 2024, Nvidia commands an extraordinary 92% share of the data center GPU market, according to third-party estimates. Recent results indicate that Nvidia is well-positioned to maintain this dominance, with $11 billion in sales of its latest generation Blackwell AI GPUs reported last quarter.

Nvidia claims that Blackwell represents “the fastest product ramp in our company’s history,” indicating strong demand driven by the rise of cost-efficient reasoning models like DeepSeek’s R1. During its February earnings conference call, Nvidia’s management highlighted:

Our inference demand is accelerating, driven by test time scaling and new reasoning models like OpenAI’s O3, DeepSeek-R1, and Grok 3. Long-thinking reasoning AI can require 100x more compute per task compared to one-shot inferences. Blackwell was architected for reasoning AI inference, supercharging reasoning AI models with up to 25x higher token throughput and 20x lower cost compared to Hopper 100.

Nvidia’s rivals are racing to release new chips to keep pace, but catching up is challenging due to Nvidia’s well-established supply chain and a strong developer community that provides a competitive edge. As noted by Nvidia management during the conference call, their “programmable architecture accelerates every AI model and over 4,400 applications,” which protects substantial infrastructure investments against rapid market changes.

As a result of these factors, Nvidia has achieved a remarkable 200x reduction in AI inference costs over recent years. The company is expected to maintain its leadership in the AI chip market—a market projected to reach approximately $360 billion annually by 2030. Nvidia’s data center revenue surged by 142% last fiscal year, reaching a record $115 billion, indicating significant growth potential in this domain.

This robust performance has prompted upward revisions in Nvidia’s revenue growth estimates for the next three fiscal years, with projections showing healthy double-digit growth even after the rapid expansion of recent quarters.

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

Therefore, Nvidia remains a prime AI stock going forward, although Broadcom is also making significant strides in the market.

The Case for Broadcom

Broadcom operates in a different segment of the AI market than Nvidia, focusing on application-specific integrated circuits (ASICs). ASICs are custom processors designed for specific tasks, unlike GPUs, which are versatile for general computing tasks. This specialized focus allows Broadcom’s custom AI processors to excel in handling AI workloads, resulting in impressive growth for the company’s AI revenue.

In the most recent fiscal year 2024, Broadcom’s AI revenue more than tripled to $12.2 billion. Commentary from management during the March earnings conference call suggests that this growth could surge even more in the coming years, bolstered by demand from three hyperscale cloud customers utilizing Broadcom’s custom AI processors and networking chips.

The company sees a potential annual revenue opportunity of between $60 billion and $90 billion from these three customers, outlining how Broadcom is positioning itself for substantial growth within the AI sector.

Broadcom and Nvidia Poised for Exceptional Growth in AI Sector

Broadcom’s growth opportunities in AI are expanding as it secures additional hyperscale customers to its roster. Over the next three fiscal years, the company anticipates significant revenue from AI-related initiatives. Notably, four new hyperscale clients are currently utilizing Broadcom’s designs to manufacture custom AI chips, with two expected to reach the crucial tape-out stage in 2025, marking the final development phase before production.

The remaining two clients are working on developing custom accelerators aimed at training their next-generation frontier models. These developments suggest that Broadcom’s revenue potential from AI could greatly exceed current estimates. As a result, the company stands a strong chance of outperforming Wall Street’s growth expectations in the coming fiscal years.

AVGO Revenue Estimates for Current Fiscal Year data by YCharts

Dominance in ASIC Market Enhances Growth Potential

A key factor contributing to Broadcom’s promising growth trajectory is its leading position in the Application-Specific Integrated Circuit (ASIC) market, where it holds an estimated market share of 55% to 60%. Recent customer acquisitions reinforce the likelihood that Broadcom will maintain its competitive edge, suggesting a substantial increase in AI revenue in the future.

The Verdict: Strong Prospects for Nvidia and Broadcom

It’s evident that both Nvidia and Broadcom are formidable players in their specific AI semiconductor markets, poised for robust growth. Their respective valuations indicate that investors have a reliable option in either stock.

Nvidia and Broadcom currently have similar forward earnings multiples.

NVDA PE Ratio (Forward) data by YCharts

Investors considering an AI stock now might look at either Nvidia or Broadcom. There’s merit in considering both companies, as they capitalize on distinct yet lucrative segments of the AI semiconductor market, which should enable sustained growth for years ahead.

Don’t Miss This Opportunity for Growth

If you have ever felt like you missed out on some of the most successful stocks, it’s worth taking note. Our analysts occasionally present a strong “Double Down” Stock recommendation for companies they believe are primed for success. If you think you’ve missed an investing opportunity, now might be the ideal time to act before the moment passes. The returns speak for themselves:

- Nvidia: An investment of $1,000 when we first advised a double down in 2009 would now be worth $285,647!*

- Apple: A $1,000 investment from our 2008 recommendation would have grown to $42,315!*

- Netflix: Investing $1,000 when we recommended it in 2004 would be valued at $500,667!*

Currently, we are issuing “Double Down” alerts for three promising companies. This could be an opportune moment for investors.

Continue »

*Stock Advisor returns as of April 1, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.