Investors Weigh Options on Twilio Inc. Amid Year-to-Date Decline

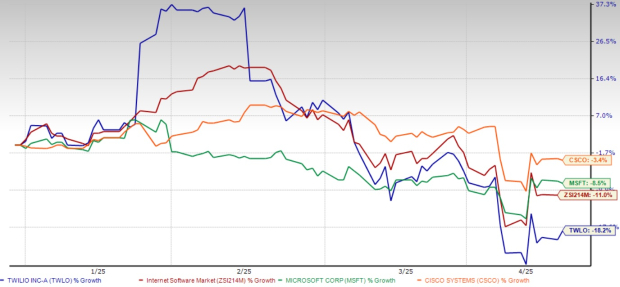

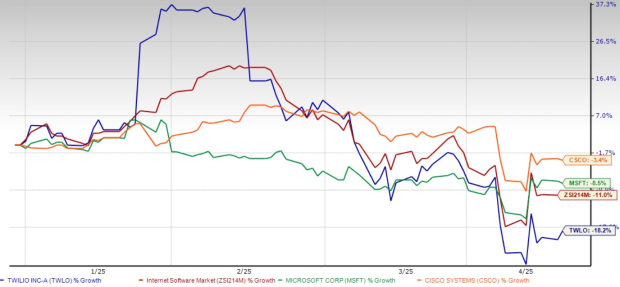

Twilio Inc. (TWLO) has faced significant challenges in 2024, as its stock has dipped by 18.2% year to date. This decline surpasses that of the broader Zacks Internet – Software industry, which has decreased by 11% during the same timeframe. When compared to major competitors such as Microsoft Corporation (MSFT) and Cisco Systems, Inc. (CSCO), the severity of Twilio’s downturn becomes even more apparent.

Assessing Twilio’s Year-to-Date Performance

Twilio Stock YTD Price Return Performance

Image Source: Zacks Investment Research

This substantial decline prompts the important question: should investors exit and cut their losses, or is TWLO Stock a hold for the long term? Despite the immediate challenges, Twilio maintains strong long-term growth prospects, providing a rationale for retaining shares.

Factors Behind Twilio’s Decline

Twilio’s recent stock struggles are part of a broader tech sector retreat fueled by apprehensions over a potential tariff war and signs of slowing economic growth. Additionally, its fourth-quarter results for 2024 fell short of expectations for bottom-line performance, compounded by a lackluster profit outlook for the first quarter of 2025.

On February 13, Twilio posted a non-GAAP EPS of $1.00, which was lower than the Zacks Consensus Estimate of $1.02. Nevertheless, it did report revenues of $1.19 billion, slightly exceeding forecasts.

Twilio Inc. Stock Price, Consensus and EPS Surprise

Twilio Inc. price-consensus-eps-surprise-chart | Twilio Inc. Quote

Investors were alarmed by Twilio’s disappointing guidance for the first quarter of 2025. Management forecast EPS in the range of 88-93 cents, falling short of the consensus estimate of 95 cents. Furthermore, anticipated revenues of $1.13 to $1.14 billion suggested a sequential decline, raising concerns about diminishing demand and profitability.

While these immediate results are troubling, they do not overshadow Twilio’s robust long-term fundamentals. Continuous investments in AI and customer engagement solutions, coupled with a devoted customer base, strengthen the case for holding the Stock during this volatile period.

Twilio’s Leadership in Customer Engagement

Twilio holds a dominant position in the customer engagement market by facilitating real-time, personalized interactions for businesses worldwide. Its AI-enhanced solutions significantly improve efficiency and customer satisfaction. Platforms such as Twilio Verify and Voice Intelligence utilize AI to optimize customer interactions, enhancing security and providing insight.

Another key growth driver is Twilio Segment, which serves as a dynamic customer data platform. By consolidating customer information across multiple channels, Segment enables businesses to run targeted, data-driven marketing campaigns that boost retention and sales.

The increasing adoption of AI by enterprises to streamline processes and elevate customer experiences places Twilio’s advanced data-driven platforms in a favorable position. This strategic focus on the customer engagement market underscores Twilio’s long-term viability, despite facing short-term challenges.

API-First Strategy Provides Competitive Advantage

Twilio’s application programming interface (API)-first approach sets it apart from larger competitors such as Microsoft, Amazon (AMZN), and Cisco. Unlike these behemoths, which often offer standardized solutions, Twilio provides customizable APIs that businesses can tailor to their specific communication needs, creating a distinct competitive edge.

This flexibility attracts diverse customers, ranging from startups to large corporations, thereby enhancing customer loyalty. Additionally, Twilio’s presence in over 180 countries broadens its market footprint compared to regional competitors. Its deep integration of messaging, voice, email, and video solidifies its role as a leading provider of holistic customer engagement solutions, boosting its growth outlook.

Financial Resilience and Shareholder Returns

Despite the earnings miss, Twilio’s financial performance remains strong. In the fourth quarter, the company achieved 16.3% year-over-year EPS growth, with a revenue increase of 11%, showcasing its resilient business model.

Twilio’s dollar-based net expansion rate rose to 106%, improving from 105% in the prior quarter and 102% year over year, highlighting solid customer retention and upselling strength. Active customer accounts exceeded 325,000 as of December 31, 2024, compared to 320,000 in the previous quarter, indicating continued customer growth.

The company’s balance sheet remains robust, boasting $2.38 billion in cash, cash equivalents, and short-term investments at the end of December 2024. Its free cash flow of $657.5 million in 2024, along with $716.2 million in operating cash flow, reflects its financial stability and capacity to support growth initiatives.

Thanks to its solid cash flow, Twilio has been able to return capital via regular quarterly dividends and stock buybacks. In 2024 alone, it repurchased $2.33 billion worth of shares, concluding its $3 billion buyback program. In January 2025, a new $2 billion repurchase plan was authorized by the board, demonstrating management’s confidence in the company’s long-term value.

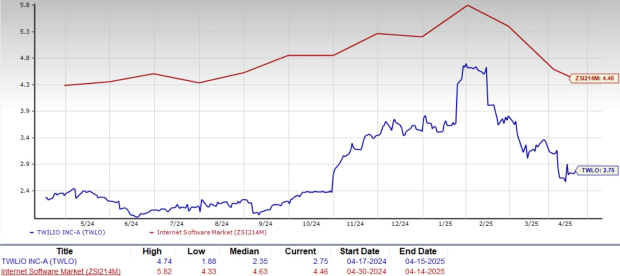

Valuation Analysis: A Case for Holding Twilio Stock

Following the recent sell-off, Twilio’s valuation has become increasingly attractive. The Stock now trades at a forward price-to-sales (P/S) ratio of 2.75X, significantly lower than the Zacks Internet – Software industry average of 4.46X. This relative discount indicates that much of the short-term weakness has been factored into the stock price, making it a sound hold for investors willing to be patient.

Twilio Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

When compared to larger tech players, Twilio’s P/S ratio is higher than Amazon’s but lower than Microsoft and Cisco’s. Currently, Microsoft, Cisco, and Amazon hold P/S ratios of 9.43X, 3.91X, and 2.67X, respectively.

Conclusion: Consider Holding TWLO

As the market dynamics continue to evolve, the lower valuation and Twilio’s fundamental strength suggest that holding TWLO could be a strategic decision for investors willing to weather the current market volatility.

Investors Should Hold Twilio Stock Amid Challenges

Twilio is currently navigating near-term challenges due to disappointing guidance and a downturn in the tech sector. However, the company’s long-term growth potential remains promising. Its leadership in customer engagement, advancements in artificial intelligence, and financial robustness position Twilio well for sustainable expansion.

Considering its fair valuation and strategic advantages, investors are advised to hold onto Twilio stock for the present. The company is well-equipped to leverage long-term trends in customer engagement and AI technology, even as it faces short-term market challenges.

Twilio currently holds a Zacks Rank #3 (Hold). Investors can view the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Identifies Top Semiconductor Stock

In the semiconductor sector, a notable contender has emerged. Although it is only 1/9,000th the size of NVIDIA—whose shares have soared over +800% since our recommendation—this new stock has significant growth potential ahead.

With robust earnings growth and an expanding customer base, it stands ready to fulfill increasing demand for artificial intelligence, machine learning, and the Internet of Things. The global semiconductor manufacturing market is forecasted to surge from $452 billion in 2021 to $803 billion by 2028.

For those interested, you can discover this stock for free >>

Are you looking for the latest recommendations from Zacks Investment Research? Today, you can download the “7 Best Stocks for the Next 30 Days.” Click to obtain this free report.

For additional analysis, check out the free stock analysis reports for:

- Amazon.com, Inc. (AMZN): Free stock analysis report

- Microsoft Corporation (MSFT): Free stock analysis report

- Cisco Systems, Inc. (CSCO): Free stock analysis report

- Twilio Inc. (TWLO): Free stock analysis report

This article was originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.