Understanding Broadcom’s Recent Stock Decline and Future Prospects

The stock market often experiences declines, which can be unsettling, particularly when they occur rapidly. Recent weeks have exemplified this volatility, driven in part by the Trump Administration’s tariff announcements and geopolitical tensions. As a result, stocks have suffered substantial losses.

Broadcom (NASDAQ: AVGO) has experienced a significant drop, falling nearly 40% from its late-2024 highs, marking its steepest decline in a decade, except during the initial market crash due to COVID-19 in early 2020. The stock has since rebounded from its recent lows. Should investors consider purchasing Broadcom at this juncture?

Where to invest $1,000 right now? Our analyst team has identified the 10 best stocks to buy currently. Learn More »

Here are key insights to consider.

Past Buying Opportunities During Market Declines

Historically, market panic can create favorable buying opportunities. The reasons for these panic-induced declines vary, but fear often leads investors to overreact. While fears around tariffs are currently driving the market downward, similar panic was witnessed with COVID-19 in 2020.

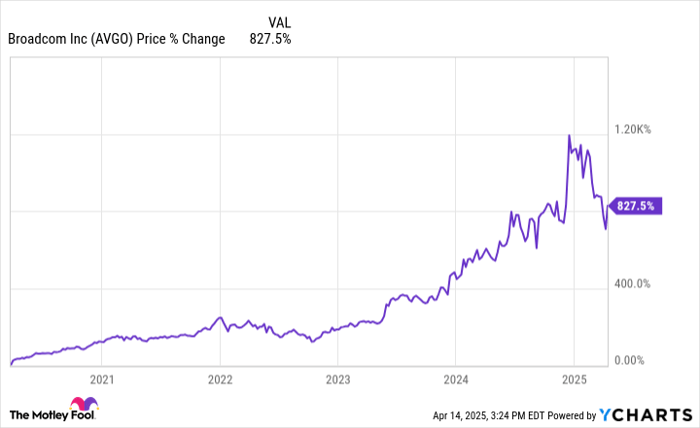

During that period, the stock market collapsed, and Broadcom’s stock price plummeted almost 50%. While investing in such a tumultuous environment may be daunting, those who seized the moment and invested in the semiconductor giant have seen substantial returns. Since March 2020, Broadcom’s stock has surged over 800%:

AVGO data by YCharts

However, it’s essential to note that not every stock thrives during a downturn. A bear market can eliminate low-quality companies and lead to lasting losses. Yet, Broadcom, recognized as a leader in the semiconductor industry, has shown resilience and a strong recovery post-pandemic.

Broadcom’s Growth Prospects Fueled by AI

For the past decade, Broadcom has prospered, primarily fueled by growth in its foundational semiconductor business, which focuses on chips for networking and communications. The company has further diversified through strategic acquisitions, with infrastructure solutions now accounting for about 40% of its operations. This division offers products and services that include cybersecurity, software for enterprise mainframes, and private cloud solutions.

The rise of artificial intelligence (AI) has introduced new growth avenues for the semiconductor sector. AI models require vast computing capabilities to train and operate, and Broadcom is securing its position in this evolving landscape. The company is actively developing specialized accelerator chips (XPUs) for major firms, often referred to as AI hyperscalers, that are investing heavily in AI infrastructure.

Management anticipates that contracts with just three hyperscalers could yield a revenue opportunity ranging from $60 billion to $90 billion by 2027. In 2024, Broadcom generated $12.2 billion in AI-related chip revenue; achieving even a fraction of the projected opportunity would significantly boost growth in the coming years. Analysts project that the company’s earnings will increase by nearly 21% annually over the next three to five years.

Evaluating the Investment in Broadcom Stock

Broadcom’s strong growth outlook and recent price drop may suggest a buy, but caution is warranted.

Recall the previous mention of the pendulum effect. This time, it appears to have swung in the opposite direction. The market has rebounded sharply on AI enthusiasm over the last two years. Consequently, as stock valuations rise, they increasingly reflect anticipated future growth. Broadcom’s price-to-earnings (P/E) ratio has escalated from 32 in March 2020 to 86 today. Although the stock price has risen dramatically, earnings have not grown at a comparable rate.

With a PEG ratio of 4, Broadcom’s valuation seems excessive, even for a company with projected earnings growth of 21% per year. I usually prefer to invest in high-quality stocks with PEG ratios from 2 to 2.5. As the PEG ratio rises, risk increases—business growth may not meet expectations, or overall market valuations may decline.

While Broadcom remains a strong business entity, overpaying for stocks, regardless of their quality, tends to result in unfavorable outcomes.

Is Investing $1,000 in Broadcom Wise Right Now?

If you’re contemplating buying Broadcom stock, consider the following:

The Motley Fool Stock Advisor has identified the 10 best stocks to buy now, and Broadcom isn’t included. The recommendations on this list could yield significant returns in the near future.

For instance, if you had invested $1,000 in Netflix on December 17, 2004, when it was recommended, your investment would now be worth $524,747!* Similarly, a $1,000 investment in Nvidia on April 15, 2005, would now be valued at $622,041!*

It’s important to note that Stock Advisor has achieved an impressive total average return of 792%, far surpassing the 153% return of the S&P 500. Don’t miss the latest top 10 list available to join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of April 14, 2025

Justin Pope has no position in any of the stocks mentioned. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.