Netflix Inc. Reports Strong Q1 2025 Results with Bright Future Projections

Netflix Inc. (NFLX) has announced impressive financial figures for the first quarter of 2025. The company recorded earnings of $6.61 per share, exceeding the Zacks Consensus Estimate of $5.69. Revenues reached $10.54 billion, slightly below the consensus estimate of $10.55 billion, but still reflected a substantial 12.5% year-over-year increase.

Despite facing challenges due to trade and tariff concerns, Netflix has sustained robust engagement levels during the quarter. With its vast subscriber base, NFLX remains positioned to outpace its closest competitor, The Walt Disney Co. (DIS).

Confident Projections from Netflix

Looking ahead, Netflix has reaffirmed its 2025 guidance. The company expects revenues to fall between $43.5 billion and $44.5 billion. Additionally, NFLX is aiming for a 2025 operating margin of 29%, an increase from the previous forecast of 28%, and two points higher than the 27% margin for 2024.

Enhanced Use of AI Technology

Netflix strategically employs artificial intelligence (AI), data science, and machine learning (ML) to deliver more relevant and intuitive content recommendations to viewers. The AI platform assesses individual viewing habits to provide personalized suggestions.

By aggregating subscriber data, NFLX’s AI model tailors content choices based on specific user preferences. These AI-driven capabilities allow Netflix to offer an enhanced streaming experience while optimizing bandwidth usage.

High Visibility with Advertising Strategies

On April 1, Netflix launched its Ad Suite in the United States, with plans to expand this offering to international markets in the subsequent quarter. This expansion of ad-supported streaming will likely bolster subscriber acquisition and improve Average Revenue Per User (ARPU).

Capitalizing on its scalable ad business, NFLX intends to utilize its proprietary ad system, moving away from its previous partnership with Microsoft Corp. (MSFT). The company’s initiatives, including offering lower-priced ad-supported tiers, ending password sharing, and implementing effective price increases, place NFLX in a strong position to withstand potential economic downturns.

Positive Estimate Revisions for NFLX Stock

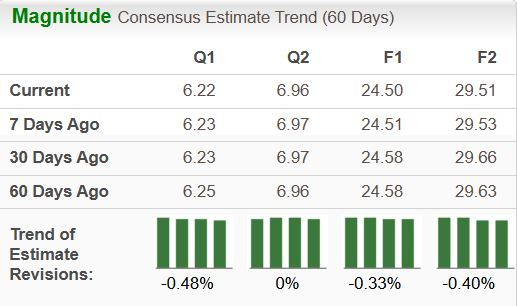

The Zacks Consensus Estimate for second-quarter 2025 projects revenues of $10.96 billion, reflecting a 14.7% improvement from the prior year, alongside estimated earnings per share of $6.22, representing a 27.5% year-over-year increase. Over the last four quarters, Netflix has consistently outperformed expectations with an average earnings surprise of 6.9%.

In the past 90 days, NFLX has also seen upward revisions in earnings estimates for 2025. Currently, the Zacks Consensus indicates projected year-over-year increases of 13.8% in revenue and 23.6% in EPS for 2025. For 2026, estimates reflect expected growth of 11.4% in revenues and 20.5% in EPS.

Image Source: Zacks Investment Research

Valuation of NFLX Shares

Netflix displays an impressive long-term growth rate of 19.6%, surpassing the S&P 500 Index’s growth rate of 12.6%. The company boasts a return on equity (ROE) of 40%, compared to the S&P 500’s 17% and the industry average of 6.17%. Additionally, NFLX currently maintains a net margin of 23.07%, significantly higher than the S&P 500’s net margin of 12.7%.

Image Source: Zacks Investment Research

Investment Considerations

Currently, Netflix holds a Zacks Rank #3 (Hold). As of February 14, the stock price reached an all-time high of $1,064.5 but dropped to $821.1 by April 7 due to market volatility connected to tariffs. Presently, the stock price is 8.6% below its 52-week high.

Despite recent fluctuations, Netflix shares have risen 9.2% year-to-date, while the S&P 500 Index has declined 10%. The average target price among analysts suggests a potential 10.8% increase from the last closing price of $973.03, with projected values ranging from $800 to $1,494, presenting a maximum upside of 53.5% and minimal downside of 17.8%.

As earnings estimate revisions are likely to trend upward in the near term, many analysts anticipate adjustments to their price targets for NFLX, thus enhancing its favorable risk/reward profile.

In light of this, it may be wise to invest progressively in this stock. Adopting a systematic investment approach can help average costs, making it advisable to hold onto this stock long-term. The company’s strong execution in recent quarters combined with robust projections should yield significant value, potentially resulting in an attractive price appreciation.

Image Source: Zacks Investment Research

Zacks’ Research Chief Identifies Top Stock with Doubling Potential

Our expert team has identified five stocks that have the highest likelihood of gaining +100% or more in the upcoming months. Among these, Director of Research Sheraz Mian singles out one stock anticipated to achieve the highest growth.

This top choice is noted for being an innovative financial firm, boasting a customer base exceeding 50 million alongside a diverse array of cutting-edge solutions, positioning it well for substantial growth. While not every elite pick ensures success, this one has the potential to outperform previous standout Zacks stocks, such as Nano-X Imaging, which surged +129.6% in merely nine months.

For additional insights, view our top stock and four alternatives.

Want comprehensive recommendations from Zacks Investment Research? Download our report on the 7 Best Stocks for the Next 30 Days. Click for access to this exclusive report.

Microsoft Corporation (MSFT): Access Free Stock Analysis report.

Netflix, Inc. (NFLX): Access Free Stock Analysis report.

The Walt Disney Company (DIS): Access Free Stock Analysis report.

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.