Lucid Group: A Discount Opportunity Amidst Market Headwinds

Investors often look for chances to secure shares in promising companies at a discount. Many see Lucid Group (NASDAQ: LCID) as such an opportunity, especially after a notable correction at the start of 2025. Currently, the shares are trading well below historical norms, even as sales are expected to surge by over 100% this year.

Is now the right time to invest in this growing stock? If you are in pursuit of investments with substantial growth potential, Lucid may be worth considering.

Factors Contributing to Lucid’s Share Decline

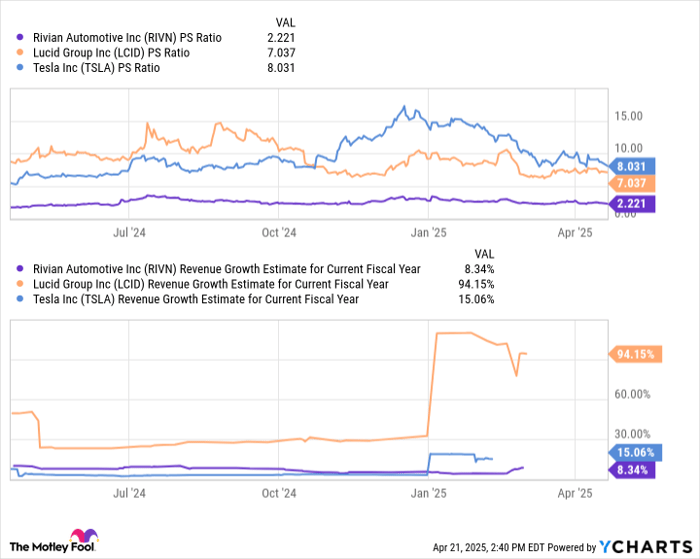

Since the beginning of 2025, Lucid shares have depreciated nearly 25%. The overall electric vehicle (EV) sector is struggling this year, with Tesla shares down over 40% and Rivian Automotive shares falling close to 20%.

Consequently, it’s difficult for any individual company to appreciate when the entire industry is in decline. This industry-wide downturn is significantly impacting Lucid’s stock performance. What are the primary reasons for this sector struggle? There are three key factors.

The first reason is a market reset in the appetite for growth stocks. Unlike traditional car manufacturers, EV producers like Lucid have more growth opportunities ahead. However, as growth prospects were once heavily factored into stock valuations, the recent market downturn has reduced the premium investors are willing to pay, regardless of stable growth expectations. Presently, market sentiment has lowered the amount investors are prepared to invest in the prospective growth of Tesla, Rivian, Lucid, and similar companies.

Further complicating matters, consumer confidence fell to the second-lowest levels since 1952 last month. Although electric vehicles generally offer savings through lower maintenance and fuel costs over time, their initial purchase price is often higher than that of conventional vehicles. This premium may lead consumers to delay EV purchases, directly impacting demand.

Moreover, the $7,500 federal tax incentive for electric vehicle purchases faces uncertainty under the new administration. If the incentive is withdrawn, a decline in EV demand could be anticipated.

A Case for Investing in Lucid Shares

Despite these challenges, 2025 could present a unique buying opportunity for long-term investors. Lucid is projected to experience impressive growth, with a sales increase of 94.2%, especially following the launch of its Gravity SUV platform.

Currently, shares of Lucid trade at about 7 times sales, which, while still a premium, reflects a 50% discount compared to the highs of 2024. When evaluated using next year’s expected sales, Lucid trades at around 3.5 times forward sales, making it a more attractive option.

Looking ahead, Lucid plans to introduce three mass-market vehicles in 2026, each priced at $50,000 or less. Historical trends show that offering affordable vehicles can drive substantial growth, as evidenced by Tesla’s trajectory. Although there’s skepticism regarding the company’s ambitious production schedule, it’s evident that Lucid has a clear growth path. Investing now provides a discount compared to the company’s recent trading history.

That said, potential investors should note that this is a high-risk, high-reward opportunity suited for those willing to take on volatility.

Should You Invest in Lucid Group Shares?

Before committing to a stake in Lucid Group, consider the following:

Investment analysts have identified other stocks they believe are strong buys currently, and Lucid Group is not included on that list. The selected top stocks could yield significant returns in the coming years.

Reflect on past recommendations: when Netflix was suggested on December 17, 2004, a $1,000 investment would now be worth $566,035. Similarly, a $1,000 investment in Nvidia back on April 15, 2005, would now be valued at $629,519.

Such histories underline the potential of well-researched investments. In the context of strong performance metrics, Lucid Group’s future remains uncertain and so careful consideration is warranted.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.