Berkshire Hathaway’s Investment Strategies Shift Amid Changing Insurance Landscape

Berkshire Hathaway (NYSE: BRK.A) (NYSE: BRK.B) has consistently outperformed the S&P 500 (SNPINDEX: ^GSPC) over the past 60 years, credited largely to its investment choices in enduring stocks like American Express, Coca-Cola, and recently, Apple. However, Berkshire’s significant public equity positions may not be the primary driver of its success moving forward.

On May 3, Berkshire released its first-quarter results, showcasing a record cash position of $342.39 billion in cash, cash equivalents, and U.S. Treasury bill investments. As of May 2, the company’s public equity portfolio was valued at $277.41 billion, which accounts for about a quarter of its total market capitalization of $1.16 trillion. The remaining value is derived from Berkshire’s subsidiaries.

Valuable Subsidiaries and Insurance Focus

Berkshire holds significant wholly-owned businesses, notably the BNSF railroad and Berkshire Hathaway Energy. However, the most critical component remains its property and casualty (P&C) insurance operations. During Berkshire’s annual shareholder meeting on Saturday, investors expressed interest in the future of these P&C businesses, especially regarding the influx of private equity investment and the effects of technological advancements like autonomous vehicles.

Will changes in the P&C insurance sector undermine Berkshire’s investment strategy? Here are the main insights gathered from remarks by Warren Buffett and Ajit Jain, Berkshire’s vice chairman of insurance operations, at the annual meeting.

Image source: Getty Images.

Insurance Insights from Berkshire’s Q1 Results

In the first quarter, Berkshire recorded $4.23 billion in income from both insurance underwriting and investments, amounting to 43.9% of its total operating earnings.

As insurance revenues increase, this segment has garnered greater attention at Berkshire’s annual gatherings. The P&C division remains the primary focus, distancing the company from life insurance markets, now heavily influenced by private equity. Buffett and Jain indicated that while private equity firms can profit significantly in life insurance, Berkshire views the leverage and credit risks involved as less appealing from a risk management perspective.

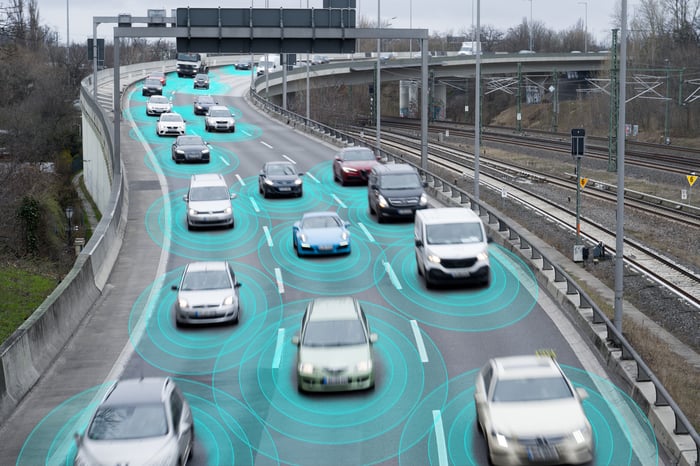

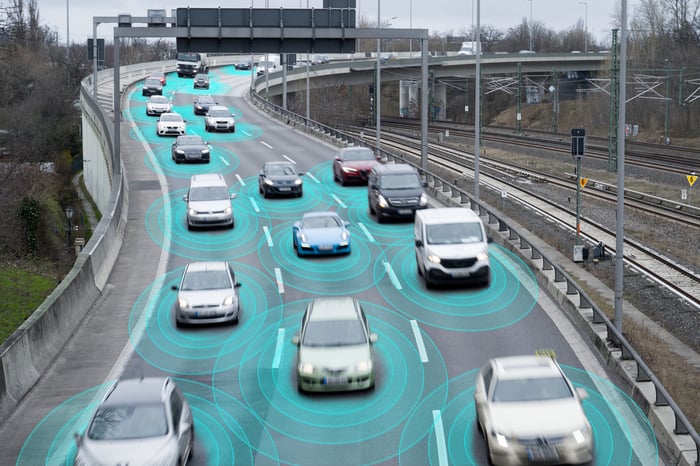

The emergence of autonomous vehicles introduces another paradigm shift in the insurance sector. When asked about potential impacts on underwriting, Buffett noted, “We expect change in all of our ideas,” expressing openness to the evolving auto insurance landscape. He mentioned that annual auto insurance premiums from GEICO have surged from as low as $40 in the 1950s to approximately $2,000 today. Despite this, accident rates have decreased by over 80%. Consequently, advancements in autonomous technology could further reduce accidents, positioning the insurance sector favorably.

Jain highlighted that full vehicle autonomy might shift the focus of auto insurance from the risks posed by drivers to the liabilities associated with automaker errors, presenting a new challenge within product liability. Buffett confidently stated that Berkshire maintains unique advantages in the insurance realm that competitors find difficult to replicate.

While significant advancements in vehicle autonomy remain on the horizon, the increasing prevalence of such technology could enhance profitability for insurers. This may come from policies either held by owners of autonomous vehicles or bundled with new vehicle sales as added value.

For instance, Tesla (NASDAQ: TSLA) has entered the insurance space with Tesla Real-Time Insurance, which adjusts premiums based on a safety score linked to its “Full Self-Driving” feature. Yet, insuring completely autonomous cars poses different challenges.

Long-Term Perspectives on Investment

The widespread integration of autonomous vehicles will indeed reshape the P&C business model, requiring the entire industry to adapt—not just Berkshire. Still, insurance remains a vital part of Berkshire Hathaway’s overarching investment perspective, necessitating continual monitoring of how technological shifts might influence underwriting practices and operating earnings.

When evaluating Berkshire Hathaway, like any investment, it is essential to adopt a long-term perspective rather than fixating on quarterly results. Buffett emphasized during the annual meeting, “We don’t do anything based on its impact on quarterly or annual earnings.” Remaining committed to this long-term strategy could afford Berkshire an advantage as the industry transitions to greater vehicle autonomy. This could enable the company to seize market share, particularly if competitors prioritize short-term profits over sustainable growth.

Evaluating Your Investment in Berkshire Hathaway

Before investing in Berkshire Hathaway, consider the following:

The Motley Fool Stock Advisor analyst team recently identified what they deem the 10 best stocks for investors currently, and Berkshire Hathaway was not among them. The highlighted stocks might yield significant returns in the years to come.

Take a look at how Netflix performed after being recommended on December 17, 2004; a $1,000 investment then would now be worth approximately $623,685! Additionally, Nvidia, when recommended on April 15, 2005, would have turned a $1,000 investment into about $701,781!

It’s important to highlight that the Stock Advisor has achieved a total average return of 906%, significantly outperforming the S&P 500’s 164% return. Don’t miss the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of April 28, 2025.

American Express is an advertising partner of Motley Fool Money. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Berkshire Hathaway, and Tesla. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.