Key Tronic Corp Suffers Revenue Decline Amid Global Tariff Issues

Shares of Key Tronic Corporation (KTCC) have experienced a 6.6% decline since the release of its third-quarter fiscal 2025 results. In contrast, the S&P 500 index registered a minor drop of 0.1% during the same period. Over the past month, while Key Tronic’s stock has slightly increased by 0.4%, the S&P 500 has grown by 6.6%.

Revenue and Earnings Overview

In the third quarter of fiscal 2025, Key Tronic reported total revenues of $112 million, reflecting a significant 21.3% decline from $142.4 million in the same quarter of the previous year. This downturn was largely due to global tariff fluctuations that escalated costs, disrupted production, and weakened demand from customers.

However, the gross margin improved to 7.7%, up from 5.7% in the previous year, aided by ongoing cost-cutting measures and workforce reductions. The operating margin remained steady at -0.4%.

The company recorded a net loss of $0.6 million, or 6 cents per share, marking an improvement from the $2.2 million or 21 cents per share loss from the prior year. The adjusted net loss also decreased to $0.6 million or 5 cents per share from $2.2 million or 20 cents per share in the same period last year.

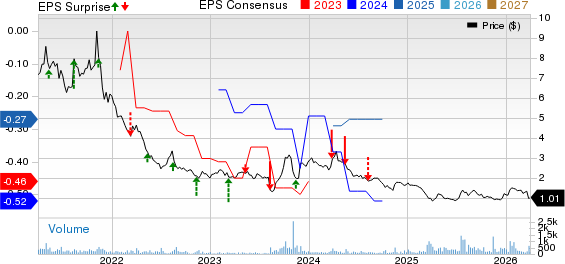

Price, Consensus, and EPS Surprise

Key Tronic Corporation price-consensus-eps-surprise-chart

Operational Performance and Business Metrics

Despite the drop in revenues, Key Tronic generated $10.1 million in operating cash flow over the first nine months of fiscal 2025, up from $6.1 million during the same period last year. The company’s inventory levels decreased by 14% or $16 million year over year, which is more in line with current revenue levels. Notably, total liabilities also fell by 14% or $34.3 million compared to the same quarter last year.

Capital expenditures stood around $3 million in the first nine months of fiscal 2025, with yearly expectations between $6 million and $8 million. These expenses mainly relate to capacity expansions in Arkansas and Vietnam to enhance geographic flexibility amid tariff uncertainties.

Management Commentary

CEO Brett Larsen and CFO Tony Voorhees noted that global tariff uncertainty, particularly concerning components from China, led to “hesitancy and business paralysis” among clients. However, they maintain a hopeful outlook for long-term growth. Management highlighted operational streamlining in Mexico, necessitated by wage inflation, and ongoing cost reductions in other locations.

Key Tronic secured five significant contracts in the quarter, including a $12 million telecommunications project in Mexico, a $6 million pest-control device contract in Vietnam, a $7 million energy initiative in Arkansas, and a consumer product contract valued between $2 million and $5 million. A $1 million design contract, with production potential reaching up to $15 million, emphasizes the company’s design strengths in facilitating growth.

The previously announced $60 million program is progressing as planned, with production ramp-up expected to start in the first quarter of fiscal 2026 and reach full capacity within 12 to 18 months.

Factors Behind the Results

The substantial revenue decline resulted primarily from decreased demand from existing clients, delayed production starts, and customers overstocking inventory. Tariff disruptions, particularly relating to components sourced from China, prompted clients to reassess their sourcing strategies. Additionally, some legacy programs concluded due to obsolescence or Key Tronic’s strategic exits in response to financial risk or difficulties managing specific accounts.

On a positive note, the gross margin has improved yearly, reflecting past restructuring benefits. Management indicated that with an additional $20 million in revenues, margins could surpass 10%, indicating potential growth from the current 7.7% margin seen in the third quarter of fiscal 2025, assuming stable macroeconomic conditions.

Other Developments

Key Tronic is advancing its capacity expansions. In Arkansas, the company plans to invest over $28 million in a new manufacturing and R&D facility, projected to create more than 400 jobs in the next five years. In Vietnam, the company intends to more than double its manufacturing capacity. These initiatives are expected to provide alternatives to Chinese manufacturing and reduce the risk of future tariff impacts.

In conclusion, while Key Tronic faces short-term challenges with declining revenues and macroeconomic uncertainty, it is concurrently fortifying its cost base, expanding its operations, and diversifying its customer portfolio. These strategic moves may pave the way for a return to profitability in the longer term.

Key Tronic Corporation (KTCC) Stock Analysis

Key Tronic Corporation (KTCC): Free Stock Analysis Report

This article originally published on Zacks Investment Research.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.