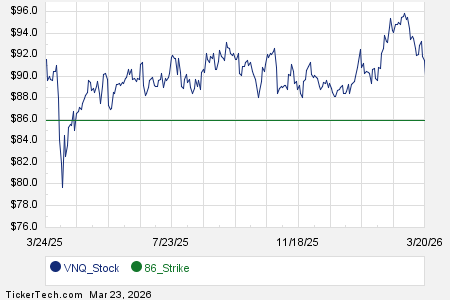

Investors in the Vanguard Index Funds Mid-Cap Value Index VIPER Shares (Symbol: VNQ) saw new options trading begin today for contracts expiring on December 18, with 270 days until expiration. The available put contract at the $86.00 strike price has a current bid of $2.00, allowing sellers to achieve an effective share purchase price of $84.00. This represents a 5% discount to the current trading price of $90.06 per share.

For call options, a contract at the $91.00 strike price is priced at $3.00. If an investor buys shares at $90.06 and sells this call, they could see a total return of 4.37% by expiration, assuming the stock is called away. The probabilities for both contracts expiring worthless are 65% for the put and 52% for the call.

The implied volatilities for the put and call contracts are 19% and 18%, respectively, while the trailing twelve-month volatility, based on recent trading data, is calculated to be 16%.