Alibaba Group reported disappointing third-quarter fiscal 2026 earnings on [date] with revenues of approximately $40.7 billion, missing estimates by 1.95%. Non-GAAP diluted earnings per ADS were $1.01, falling short by 47.12%. While revenues grew 2% year over year in local currency, net income plummeted 66%, illustrating significant challenges for the company amidst its ongoing transformation.

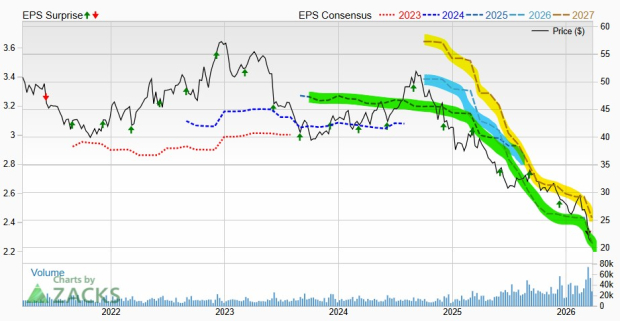

The decline in adjusted EBITDA was 57% year over year, driven by hefty investments in Quick Commerce and technology. Sales and marketing expenses surged, reflecting intense competition in China’s e-commerce space. While Alibaba’s Cloud Intelligence Group reported a 36% revenue increase, it was insufficient to offset broader profitability declines. The outlook remains grim, with projected fiscal 2026 earnings at $5.72 per share, a 36.51% year-over-year decrease.

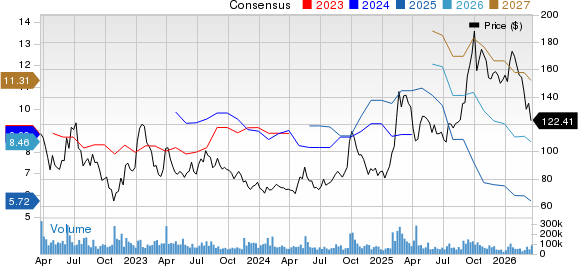

Investors face risks associated with structural headwinds and lack of clear profitability milestones. Alibaba’s shares have dropped 24.9% over the past six months, significantly underperforming the Zacks Retail-Wholesale sector, which declined 7.5%. The company’s ambitious investment commitments and pressures from domestic and international cloud competitors compound worries about its financial trajectory.