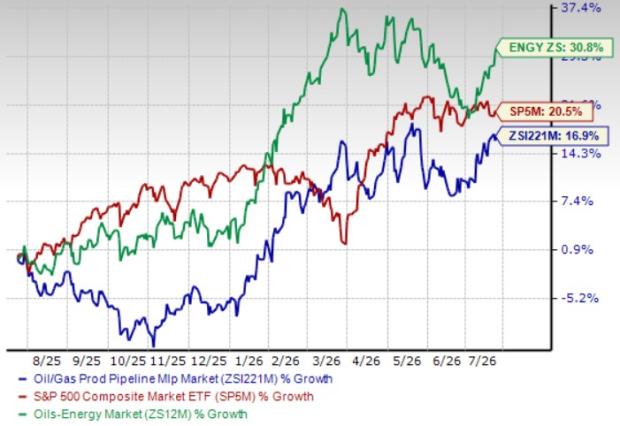

Demand for oilfield services is expected to surge as oil prices reach peak levels again, driven by the ongoing Middle East war. The price of West Texas Intermediate (WTI) crude is currently trading above $90 per barrel, promoting exploration and production activities. The oil and gas field services industry, comprising companies like Halliburton, Baker Hughes, TechnipFMC, and Archrock, is well-positioned to capitalize on this trend, with high profitability potential due to their low debt exposure, reflected in a debt-to-capitalization rate of only 31.16%.

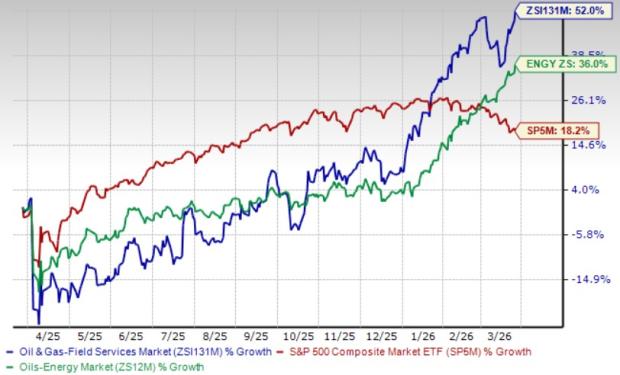

Over the past year, the Zacks Oil and Gas – Field Services industry has increased by 52%, outperforming the S&P 500’s growth of 18.2% and the broader oil and energy sector’s 36%. The industry’s favorable outlook is also supported by investments in technology that help companies reduce emissions and costs. Currently, the industry is trading at a trailing twelve-month EV/EBITDA ratio of 10.06X, compared to 17.07X for the S&P 500 and 6.95X for the oil and energy sector.

As global demand for cleaner energy sources rises, particularly natural gas, oilfield service companies are expected to benefit significantly, especially those focused on LNG infrastructure. The strong financial positions of these firms should also allow them to navigate potential market volatility effectively.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.