MercadoLibre is experiencing margin pressure as it aggressively expands its first-party (1P) business, which saw a 69% year-over-year gross merchandise volume increase in Q1 2026, significantly outpacing overall marketplace growth. This rapid scaling, particularly in consumer electronics, requires higher logistics and fulfillment spending due to inventory ownership, resulting in a gross margin contraction of 300 basis points compared to the previous year.

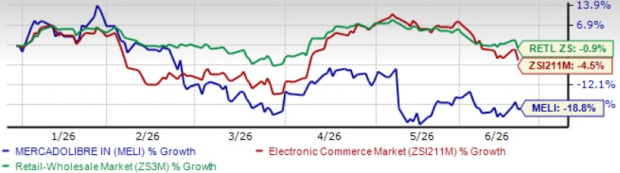

As of Year-To-Date (YTD) 2026, MercadoLibre’s stock has declined 18.8%, contrasting with the 4.5% decline in the Zacks Internet–Commerce industry. The Zacks Consensus Estimate projects the company’s earnings to reach $40.97 per share, a 3.98% increase year-over-year. Despite these challenges, MercadoLibre continues to prioritize market share growth over immediate profits, facing competition from Amazon and Alibaba, which have strengthened their logistics and inventory capabilities while navigating similar margin pressures.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.