Key Points

-

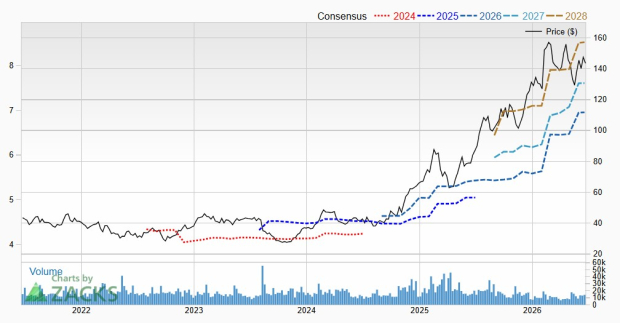

Tesla’s electric vehicle (EV) sales represent over 70% of its revenue, but have seen declines, with 2024 sales dropping to 1.79 million cars and a further decline to 1.63 million in 2025.

-

On July 2, Tesla is expected to report its second quarter 2026 EV deliveries, with analysts predicting around 400,000 cars, which would indicate a potential turnaround.

-

Tesla’s high P/E ratio of 366 raises concerns about the stock’s growth prospects despite new products like the Cybercab and Optimus humanoid robot.

As of now, Tesla (NASDAQ: TSLA) is facing challenges as it comes off two consecutive years of declining EV sales. A key moment will occur on July 2, 2026, when the company reports its second-quarter EV deliveries, with a projected target of approximately 400,000 units. This figure could reflect a rebound in sales after recent losses, as first-quarter deliveries in 2026 already saw a 6% year-over-year increase.

In 2025, Tesla’s automotive revenue fell by 10%, contributing to a 3% decrease in total revenue. While the competitive landscape intensifies—with rivals like BYD and Geely reporting substantial growth—Tesla is banking on innovative products. CEO Elon Musk has indicated the Cybercab began production in April, aiming for operational rollout pending regulatory approvals. However, the company’s hefty P/E ratio could pose risks for investors, depending on how successful these new ventures become.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.