Microsoft Corporation (MSFT) reported revenues of $82.9 billion for the third quarter of fiscal 2026, reflecting an 18% year-over-year increase. GAAP earnings per share reached $4.27, up 23%. Cloud revenues surged 29%, totaling $54.5 billion, with Azure growing by 40%. The company anticipates revenues for the fiscal fourth quarter to be between $86.7 billion and $87.8 billion, with a projected operating margin of approximately 44% due to significant capital expenditures exceeding $40 billion.

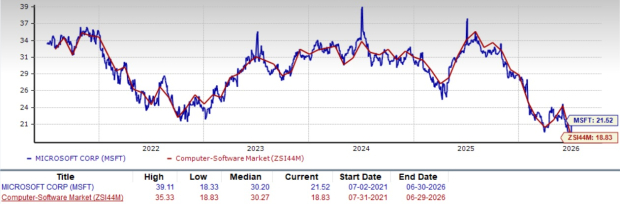

Looking ahead, Microsoft has guided cloud growth of 15% to 16% for Microsoft 365, supported by rising Copilot seat additions. The Zacks Consensus Estimate projects fiscal 2026 earnings at $16.76 per share, indicating a solid 22.84% year-over-year growth. However, MSFT’s forward price-to-earnings ratio stands at 21.52X, exceeding the Zacks Computer – Software industry’s average of 18.83X, raising concerns among investors regarding its premium valuation amid continued heavy investments in data-center and AI infrastructure.

Microsoft shares have declined 21.1% over the last six months, while the Zacks Computer – Software industry decreased by 23.8%. Competitors like Amazon and Google are intensifying pressure in the cloud and AI sectors, with Amazon’s AWS and Google’s cloud solutions gaining traction. Investors are weighing the trade-off between Microsoft’s promising growth prospects and the risks associated with its current valuation and margin pressures.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.