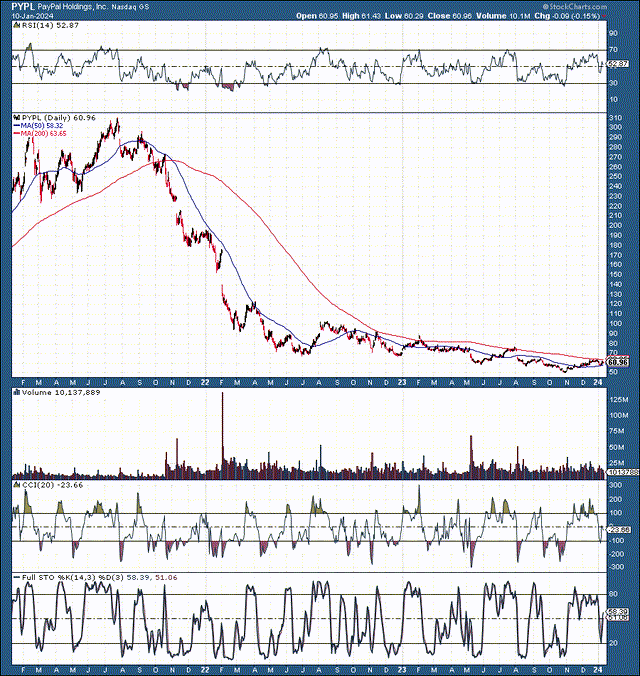

PayPal Holdings, Inc. (NASDAQ:PYPL) stock used to trade around $300, hitting a high of about $310 in 2021. However, due to a series of unfortunate events such as poor management decisions, a slow economic environment, high interest rates, worsening sentiment, higher costs, and other factors, PayPal’s stock plummeted to a low of just $50 in recent months.

This monumental decline indicates a staggering drop of 84%. Could this be the start of a remarkable turnaround? Despite the temporary setbacks, PayPal remains a dominant force in the global online payment platform. Furthermore, despite economic challenges, PayPal’s revenues continue to expand, setting the stage for healthy revenue growth in the near future. Notably, PayPal stock is currently undervalued, trading at only 11 times this year’s EPS estimates and below a 10 forward P/E.

This exceptionally low valuation is unlikely to persist, as PayPal’s leading market position, growth potential, and profitability prospects justify a higher multiple. Additionally, surpassing its most recent earnings announcement and the potential for better-than-expected earnings could enhance sentiment, causing PayPal’s multiple to expand and its share price to surge in the coming years.

Revamping Leadership – A Significant Advantage

One of the most favorable developments for PayPal is the appointment of a new CEO and a revamp in the management team. Under the guidance of Dan Schulman, PayPal ousted accounts that didn’t align with its core values. However, the company became excessively politicized, deviating from its primary focus on growth and optimization. Consequently, PayPal alienated users, employees, and investors, finding itself embroiled in turmoil.

The primary objective of any business, including PayPal, is to generate returns for its shareholders. While adhering to ethical and moral standards and providing beneficial products or services to society is crucial, deviating from its core objectives and taking on undue responsibilities can be detrimental. Fortunately, PayPal’s challenges seem temporary and correctable. Schulman’s departure from the company may be the best course of action for shareholders, enabling PayPal to refocus on revenue growth, increased profits, and delivering shareholder value.

Projected Growth in PayPal’s Revenues

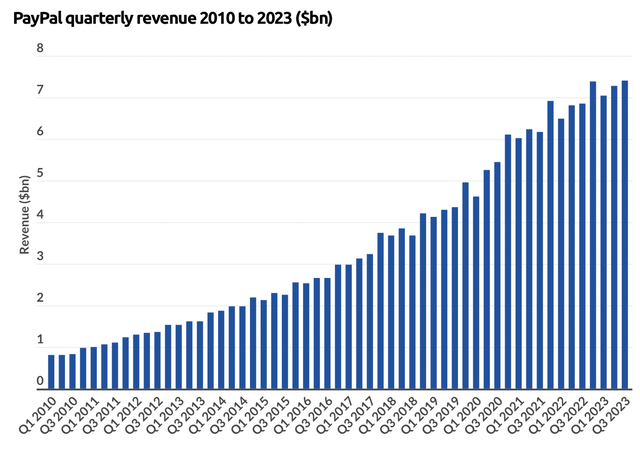

It is crucial to highlight PayPal’s exceptional revenue growth trajectory. From having less than $1B in quarterly revenue in 2010 to an anticipated $7.9B in Q4, PayPal’s growth trajectory is truly remarkable. With the stock trading at an 84% discount from its all-time high, an air of incredulity surrounds this situation.

Moreover, PayPal’s earnings projections may be excessively pessimistic. This scenario sets the stage for PayPal to surpass its upcoming earnings announcement, improving sentiment and resulting in a higher stock price as time progresses.

Anticipated Earnings Surge for PayPal

In the last quarter, PayPal reported a solid increase of 8% with $7.42 billion in revenues. Notably, this healthy revenue increase occurred during an economic slowdown and amidst historically high interest rates, yet PayPal experienced limited adverse effects. As economic conditions improve, costs and inflation moderate, and interest rates decline, PayPal’s growth and profitability should experience an upturn.

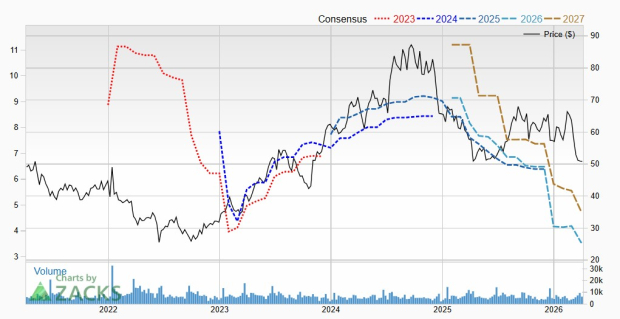

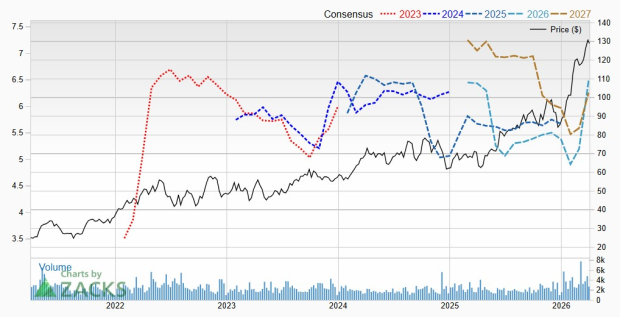

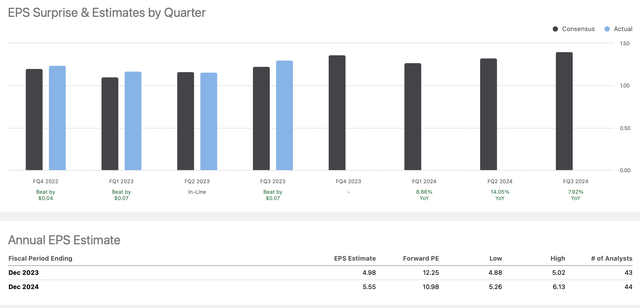

With this year’s consensus EPS estimate at $5.55, PayPal’s dirt-cheap P/E ratio of 10.98 in relation to this year’s conservative consensus estimate is worth noting. PayPal’s earnings revision grade stands at a respectable B (SA Quant System). There is a high likelihood that PayPal could exceed the consensus figure, earning approximately $6 this year, pushing its P/E ratio even lower. It’s fascinating how undervalued PayPal is.

Additionally, the consensus EPS estimate for next year at $6.16 may be surpassed by PayPal, showcasing a modest 10-12% year-over-year EPS growth. This would place its forward P/E ratio at just 9.3. The market seems to be assigning an excessively pessimistic outlook to PayPal, but such ultra-low sentiment often presents the perfect opportunity to invest in a stock.

PayPal’s Enduring Position in the Industry

As of Q3 2023, PayPal boasted 428 million active user accounts. Although this represents a minor decline from the recent record of 435 million users, a resurgence in growth is anticipated. With an approximate 42% market share, PayPal continues to lead the global online payment services segment. Additionally, within the U.S., PayPal commands nearly 60% of the payment services market.

PayPal’s Dominance in Global Online Payment Processing

In 2022, PayPal processed a staggering 22.8 billion global transactions. Despite the temporary decline in active users, PayPal recorded a record 6.2 billion transactions last quarter, marking an 11% increase from the 5.6 billion processed in the same quarter a year ago. Consequently, PayPal’s growth persists despite a sluggish economic environment. As economic conditions ameliorate, PayPal stands to benefit from a compounded effect of increased transaction volume and renewed user growth, potentially resulting in better-than-anticipated

PayPal’s Bright Future: A Bullish Investment Outlook

The last I checked, PayPal was still a fintech company capitalizing on transactions. It’s different from a traditional financial institution with heavy loan exposure and minimal growth. Despite the transitory economic slowdown and other short-term negative factors, PayPal’s sales growth should improve, and increased optimization and cost-cutting should expand profitability in future quarters. Therefore, PayPal deserves a higher multiple than its current sub-ten P/E ratio.

I used modest revenue and EPS growth to achieve price projections much higher than PayPal’s current stock price. Also, I used a relatively low P/E ratio of below 20 for PayPal in future years. In a bullish scenario, PayPal’s sales and earnings growth could be higher than my projections, and its P/E ratio could expand beyond the 20 range, leading to higher stock prices than my model projects. PayPal Holdings, Inc. stock is exceptionally undervalued and remains a strong buy here with an intermediate-term and more extended outlook for its shares.

Future Revenue and EPS Projection

| Year | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

| Revenue Bs | $33 | $36 | $40 | $44.5 | $50 | $55 | $60 |

| Revenue growth | 10% | 9% | 11% | 11% | 12% | 10% | 9% |

| EPS | $6 | $7 | $8 | $9.20 | $10.50 | $12.20 | $14 |

| EPS growth | 20% | 15% | 15% | 14% | 15% | 15% | 14% |

| Forward P/E | 14 | 16 | 18 | 19 | 19 | 18 | 17 |

| Stock price | $98 | $128 | $166 | $200 | $232 | $252 | $280 |

Source: The Financial Prophet.

Risks and Challenges

Despite my bullish projections, there are risks associated with investing in PayPal. Competition may be PayPal’s most significant concern. To keep leading in its segment, PayPal needs to remain on top of its game, as big companies like Amazon.com, Inc. (AMZN), Apple Inc. (AAPL), and Alphabet Inc. (GOOG, GOOGL) all have alternative payment processing platforms. The primary risk factor is worsening user growth, which could transition to fewer active users, leading to declining transactions. Another concern is lower margins and a potential earnings contraction. There is also the risk of poor performance by new management. Macroeconomic factors and Fed policy could also adversely influence PayPal’s business. Investors should consider these and other risks before committing to a PayPal investment.