No one likes a dividend cut:

- They reduce the income stream that many retirees rely on for funding their retirement lifestyle.

- They often trigger a negative market response, leading to steep stock price declines. This typically adds insult to injury by adding steep capital losses on top of the steep decline in income, limiting investors’ ability to recycle the capital into another investment in an attempt to recoup their lost income.

Some companies are forced to cut their dividends due to macroeconomic events, such as many investment-grade companies like Simon Property Group (SPG) and Energy Transfer (ET) did due to economic fallout from the COVID-19 lockdowns. However, many times dividend cuts come as a result of poor balance sheet management. AT&T (T) is a classic example of this, as they had to slash their dividend in an attempt to offload cumbersome debt and retain more cash to deleverage more aggressively after burning billions of dollars on ill-fated acquisitions.

In this article, we will look at two double-digit yielding stocks that we think may soon be forced to cut their dividends in response to management overleveraging their balance sheets.

Medical Properties Trust Stock (MPW)

MPW – a REIT (VNQ) that focuses on for-profit hospitals in locations like the U.S., Europe, and Australia – recently posted solid Q3 results with FFO results and guidance that beat consensus expectations but has seen its stock price continue to crater since then anyway:

MPW’s problems began as a result of its aggressive spending on growth investments, particularly via acquiring numerous hospitals in its bid to continue its strong growth rate.

However, COVID-19 sent several of its hospital tenants into a tailspin due to significant cost increases that were not sufficiently offset by income growth Moreover, interest rates have risen sharply, which is now stressing its heavily leveraged balance sheet. As a result, management has been laser-focused on paying down its debt in a bid to shore up its balance sheet.

As part of this effort, they slashed their dividend by nearly 50% to retain more cash flow with which to pay down debt. They also have been selling assets aggressively, including an Australian hospital portfolio for over $300 million that it plans to use to reduce debt.

That being said, while it seemed for a while like MPW might be on its way out of the woods, conditions have recently deteriorated for its largest tenant Steward Health, which is having to defer rent payments and receive additional financial support from MPW due to its balance sheet issues.

In addition to the fact that MPW generates a lot of its revenue from Steward, it also has invested a considerable amount of money into Steward via both equity and debt structures in recent years as part of its efforts to keep the operator afloat and hopefully help it get through current industry headwinds. Should Steward go bankrupt, it would likely lead to a double hit to MPW in which both its revenues and balance sheet would suffer.

As a result, we think that MPW will likely have to reduce its dividend to the bare minimum in the near future to maximize its financial flexibility as it strives to continue paying down debt aggressively while also trying to keep Steward afloat.

NextEra Energy Partners Stock (NEP)

NEP’s distribution is well-covered by CAFD and – unlike MPW – its underlying business model is quite stable. Nearly all of NEP’s cash flow comes from lengthy power purchase agreements (with a weighted average term to maturity of well over a decade) on its wind and solar farms with mostly utility (XLU) counterparties whose weighted average credit rating is BBB+. As a result, while there is some cash flow variance that comes with changing wind and sun patterns, there are very few reasons why NEP would experience a sudden sharp decline in cash flow.

Moreover, its large portfolio and operating expertise give it numerous repowering opportunities that enjoy very high returns on investment and typically involve low risk. This gives NEP an impressive organic growth profile that can also be largely self-funded through leveraging the cash flows on the assets themselves, including the monetization of related tax credits.

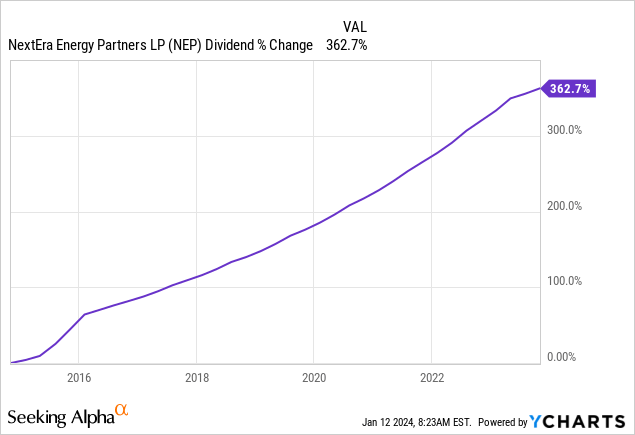

Last, but not least, NEP has an impressive track record of growing its payouts very aggressively and – despite recently halving its distribution growth outlook – is still guiding for a 5-8% distribution per unit CAGR through 2026 at least.

That being said, NEP still has some major challenges confronting it. To finance this aggressive growth over the past decade, the company stretched its balance sheet beyond its limits and is now having to play catch-up given that its cost of capital has soared due to rising interest rates. In addition to piling on a considerable amount of project-level debt, NEP took on considerable corporate-level debt and also used CEPFs (a form of equity financing that must be paid back by some contractually established date or the assets purchased with that funding will largely go to the investors in the CEPFs).

Unfortunately for NEP, its CEPFs were nearly all scheduled to come due beginning in 2023, which just happened to be when interest rates reached heights not seen in quite some time. As a result, while it was likely planning on redeeming these CEPFs with a combination of attractively priced equity and cheap debt (or potentially even new CEPFs), suddenly any kind of equity financing was off the table and its options for debt financing were also increasingly limited. Instead, management was forced to pivot to selling off its non-core pipeline assets to raise the equity proceeds needed to redeem its CEPFs maturing through 2025 and then leaned on a major favor from its parent and largest shareholder

NextEra Energy – Balancing Act: Navigating Financial Risk and Growth Opportunities

The energy sector is anything but predictable. Much like a tightrope walker, NextEra Energy (NEE) is attempting to maintain their balance, suspended between the need to offset lost cash flow from pipeline assets and the desire to continue growing its distribution. The company is seeking to suspend its IDR fees through 2026, a move that should provide a lifeline to sustain and potentially expand its distribution. This strategic maneuver aims to adapt to the changing landscape of the energy market, but questions loom about the challenges ahead.

The Tightrope Walk: Ongoing Challenges for NEP

While the plan to suspend IDR fees is a positive step, it is evident that NEP is far from secure. The management’s projection of a 90%+ payout ratio over the coming years signifies the precarious position the company finds itself in. Added to the mix are the risks associated with:

- The necessity to sell the Meade Pipeline asset at a favorable valuation

- The successful execution of repowering projects and the generation of anticipated returns

- The urgency to secure a substantial, attractively priced and financed acquisition by 2025 to continue driving growth and counterbalance the loss of cash flow from the Meade Pipeline sale and the expense of funding CEPFs in 2026 and beyond.

The looming uncertainties, high leverage on its balance sheet, and a heightened payout ratio in the face of prevalent high-interest rates all add up to a rather surprising scenario where management still steers the ship towards a 5-8% distribution CAGR through 2026. Nevertheless, the company’s distribution appears manageable under the assumption that the aforementioned strategies unfold as intended. However, should these plans falter, NEP could find itself compelled to slash its distribution, a grim prospect for investors.

It is worth noting that we approach NEP with a bullish outlook as a speculative investment. We perceive the stock as undervalued and consider the 12%+ yield as adequate compensation for the inherent risk. However, it is crucial to underscore to potential investors that NEP’s distribution is far from secure and could face potential cuts in the coming years if the company fails to deftly navigate its financial tightrope.

Investor Takeaway: High-Yield Stocks and Considerations

Dividend cuts cast a dark shadow for dividend investors, especially among high-yield stocks. This is often a consequence of high-yield stocks exhibiting at least one, if not both, of the following traits:

- High payout ratios

- Challenges to their business models and/or balance sheets, leading the market to anticipate a dividend reduction

In the context of NEP, despite the relatively high payout ratio and challenging balance sheet, we maintain a bullish stance due to our belief in the stock’s substantial undervaluation and its potential to deliver robust long-term returns, even in the event of a future distribution cut. Conversely, when considering MPW, the situation is distinctly different. While its payout ratio is not particularly high, the underlying business model and balance sheet present significant hurdles. We remain wary of MPW due to the perceived fragility of its business model, where the specter of bankruptcy looms if Steward fails to weather the storm.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.