Uncovering the Investment Potential

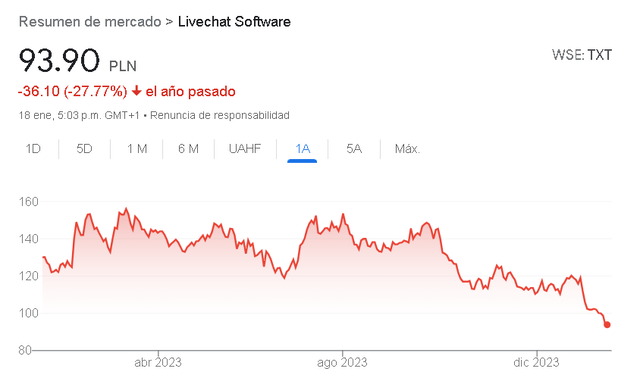

Text (OTC:LCHTF), previously known as LiveChat Software, weathered a tumultuous year, with its stock price plummeting by almost 30%. A combination of factors, such as slower growth, an increase in subscription cancellations, and apprehension surrounding artificial intelligence, have cast a shadow on the company’s prospects.

In this commentary, I intend to explore the company’s business model, its range of products, and conduct a comprehensive analysis of its financial documents. Furthermore, I will offer my viewpoint on the challenges faced and elaborate on why I perceive these obstacles as transitory, positioning Text as a compelling current investment prospect.

Insight into Business Operations

Established in 2002 in Poland, Text crafts software tailored for managing text-based customer communications in both the business-to-consumer (B2C) and business-to-business (B2B) domains. The aim is to elevate customer experiences and facilitate real-time interactions between businesses and their website visitors. Here are the key products developed by the company:

- LiveChat constitutes 91% of the revenue and facilitates swift contact between customers and companies via a chat integrated into the company’s website. This feature empowers businesses to offer live chat support, enabling customer service representatives to engage with website visitors, address inquiries, and provide immediate assistance.

- ChatBot empowers the creation of conversational chatbots for customer service teams, offering automation features for handling routine queries, thereby enhancing response times and operational efficiency.

- KnowledgeBase is designed to aid businesses in establishing and managing a centralized repository of information, allowing customers to access solutions to common queries, troubleshoot issues, and obtain self-help support, akin to the traditional “FAQs” sections but automated.

- HelpDesk is tailored to assist businesses in efficiently managing customer inquiries, support tickets, and communication channels, enabling customers to leave messages outside of business hours and facilitating effective organization and prioritization of requests by customer support teams.

In essence, Text aids businesses in managing customer interactions from diverse platforms within a unified interface. It facilitates tracking and analyzing customer interactions, streamlining workflows, and prioritizing security to safeguard sensitive customer data, ultimately enhancing the overall customer service experience.

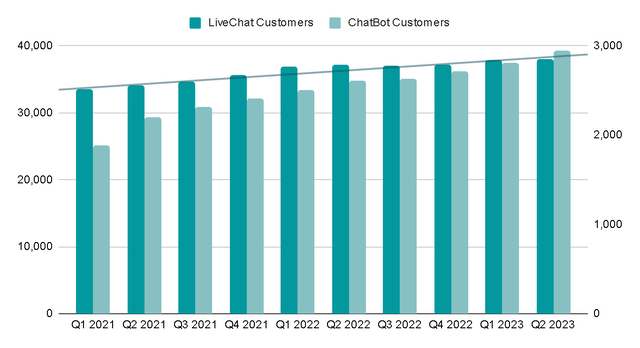

This insight elucidates the annual uptick in the company’s active client base. Text’s products address a pivotal facet of any business – customer service – making discontinuation of the subscription to access these products illogical. This assures a consistent and predictable income stream for Text.

Crucial Financial Metrics

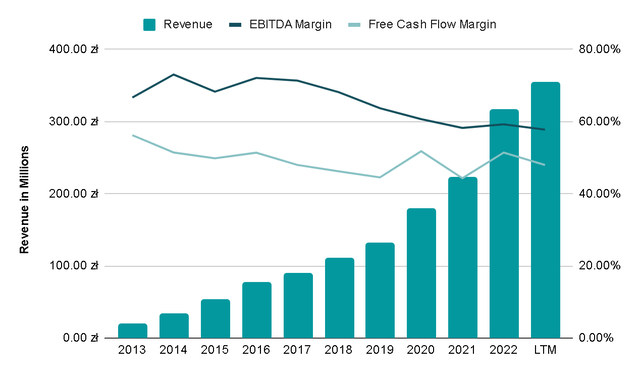

Since 2013 (fiscal year 2014), the company has recorded an exceptional annual revenue growth of 34%. However, a worrisome trend of declining margins year after year has surfaced. This warrants vigilant monitoring, as it could signify intense competition, compelling Text to reduce prices to remain competitive. The ensuing impact on gross margins might subsequently erode the EBITDA margin, attributable to challenges in establishing clear differentiation in this market segment, leading to heightened price wars.

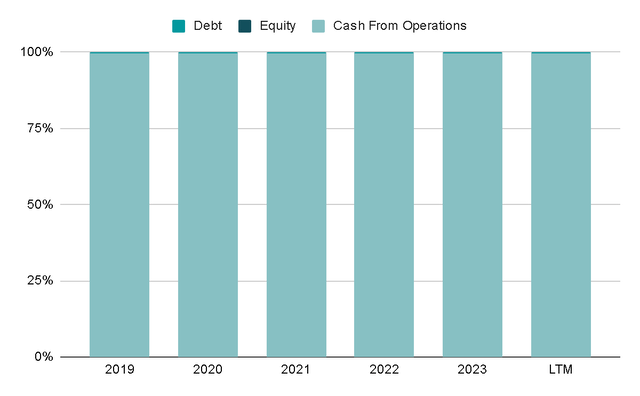

Notwithstanding the challenges posed by competition, the company has adhered to a prudent capital allocation strategy. 100% of its operations have been financed with the cash generated by the business. No debt or shares have been issued, culminating in a robust financial position. Currently, the Net Debt/EBITDA ratio is negative, signifying that the company could fully settle its total debt with the available cash on the balance sheet.

This financial stability is pivotal, particularly in light of the constant necessity for innovation to enhance products, and the evident intensity of competition. Steering clear of excessive debt mitigates financial risk for the company.

The company has exclusively channeled its capital into bolstering internal business operations, fostering the creation of new products. Notable examples include the debut of KnowledgeBase in 2017, ChatBot in 2018, HelpDesk in 2019, and most recently, in 2022, the introduction of OpenWidget – a tool designed to enhance websites. This strategic capital allocation ensures the expansion of the product portfolio and continual enhancement of existing offerings.

The Financial Landscape of Text: A Detailed Analysis

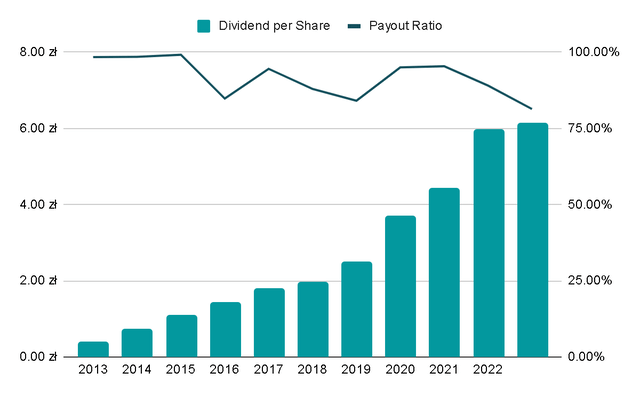

A curious aspect is that over the last five years, 77% of the capital has been directed towards dividend payments. This might seem unexpected for a rapidly growing software company. The dividend has experienced an annual growth rate of 32% over the past decade, constituting approximately 80% of Net Income.

Considering that the company has not stopped releasing and improving products in recent years, it would seem that they are generating more cash than necessary to reinvest in the business and since they have no debt either, they decide that remunerating the shareholder is the best option, which is an extra benefit for shareholders

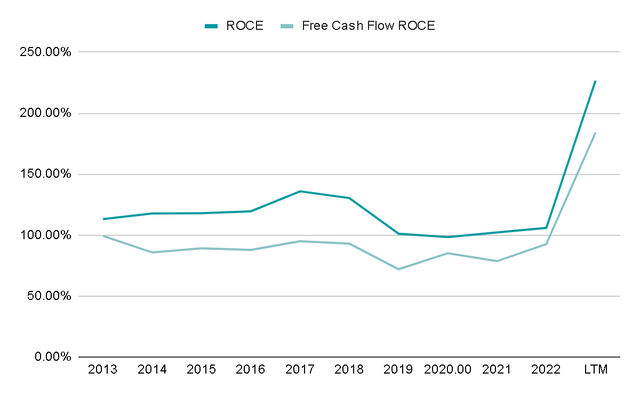

Another highly positive aspect is the company’s exceptional profitability, evident in the Return on Capital Employed, which currently stands at an impressive 226%. Over the last decade, it has consistently averaged 125%, showcasing sustained high performance.

This not only indicates an asset-light business model with high-profit margins but also reflects the success of capital allocation and investments in developing new products. With such a track record, there’s an expectation that the management will continue this trend in the coming years.

A Glimpse into Valuation

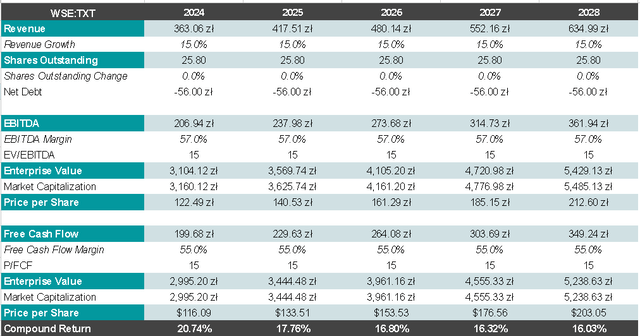

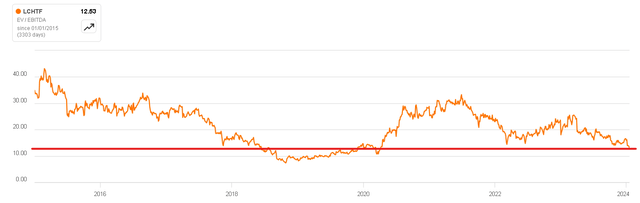

To add to the positive outlook, the company’s valuation appears highly attractive. A projection of 15% annual growth over the next five years, maintaining current margins, and applying an exit multiple of 15x EV/EBITDA suggests an expected return of 16%, in addition to the current dividend yield of 6.5%.

This attractiveness is underscored when considering the current valuation multiples:

- PER 13x

- EV/EBITDA 12x

- Free Cash Flow Yield 6.6%.

Notably, if Text were a U.S. company, its valuation could easily be at least double the current levels, given its robust ROCE, margins, and growth trajectory. But, considering that it is an unknown Polish company with a $600 million market cap, these types of inefficiencies are more common to occur.

Risks and Concerns Unveiled

As evident from recent share price trends, the company has faced challenges in recent months, and it’s crucial to address key concerns:

1- Slowing Growth: A recent update on key performance indicators revealed a modest increase of 2.2% in Monthly Recurring Revenue (MRR) compared to the previous year, and 0.3% compared to the preceding quarter. This slowing growth is a noteworthy factor.

2- Average Revenue Per User (ARPU): The LiveChat product’s ARPU decreased to $156.4 USD from $160.7 USD a year ago, while ChatBot’s ARPU increased to $132.4 USD from $115.1 USD. LiveChat’s declining ARPU raises concerns about its revenue generation per user.

3- Churn Rate Increase: The company witnessed a modest increase in the total number of customers, adding only 19 clients this quarter. However, the churn rate has escalated, reaching around 3.5%, significantly higher than the average 3%.

We have rather symbolic increase in the number of customers because this quarter has added just 19 clients. This is something disappointing to us. The churn for this quarter has increased much higher than the average 3%. It was closer to 3.5%.

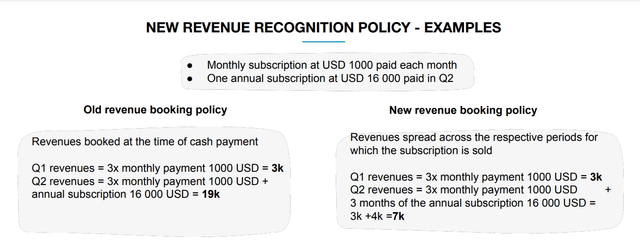

In my analysis, the sluggish growth can be attributed to two main factors. First, the adverse macroeconomic environment may have led some small clients that are in risk of going out of business to cut expenses, affecting their subscription to the platform-a potentially temporary situation. Second, a significant factor is the recent change in the revenue recognition policy, impacting how revenue is accounted for. Here’s an example of how this has changed:

With the recent change in revenue recognition, the company, even with the same revenue generation, might appear to be yielding less in the final report. While this impacts short-term results, it’s important to recognize that this shift aligns with the more accurate and commonly used practices in U.S. companies. In the long term, this change is considered a prudent decision.

This alteration in revenue recognition likely contributes to the observed decrease in Average Revenue Per User. So, although the company is experiencing a slowdown in growth due to the economic environment, it’s crucial to acknowledge that this deceleration might be also attributed to the artificial impact of the revenue recognition change. Looking forward, the next year should provide clarity, indicating whether this adjustment was a short-term challenge or a more sustained concern for the business.

4- Artificial Intelligence: A widely discussed topic in recent months, AI’s potential impact on the company has raised questions about whether it could spell “the end of Text. “In my opinion, this concern is unfounded. While AI is a powerful tool, it requires implementation by someone because AI doesn’t independently seek potential clients to offer its services (at least not currently). Companies like Text will play a crucial role in implementing AI in businesses through their existing

“`

ChatBot’s Impact on Text’s Financial Strategy

In recent developments, the unveiling of a new ChatBot by Text this year has stirred quite a buzz among its clients. The incorporation of an AI model within the product has garnered positive reception, culminating in notable performance outcomes. This move not only signals confidence in the business but could also counterbalance low earnings growth.

While share buybacks may not directly impact business performance, they can instill confidence in investors. Given the company’s track record in developing new products and its practice of using remaining capital for dividends, it’s worth considering the potential benefits of aggressive share repurchases. For instance, if the company generates $10 USD in profits with 10 shares outstanding, the earnings per share is $1 USD. However, if they repurchase 1 share, the earnings per share would increase by 11%, showcasing the potential impact of strategic share buybacks on earnings per share.

Assessing Text’s Position

In considering Text’s financial standing, several factors come into play. While the company automates and improves critical areas for its customers such as customer service, concerns arise due to the perception of limited differentiation between Text’s products and other chatbots. Additionally, the company’s prudent capital allocation has resulted in a debt-free status, but declining margins and the choice between share buybacks and dividends present considerations for investors.

Despite ongoing aspects to monitor, the current valuation is compelling and already accounts for somewhat negative scenarios. With a substantial dividend yield of 6.5%, the current valuation positions Text as a ‘buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.