During my college years from 2008 to 2013, the prevailing view among those familiar with the workings of Microsoft Corporation (NASDAQ:MSFT) was that the company was a behemoth of a bygone era. After the Dot-Com bubble burst, its market capitalization languished in a narrow range for over a decade. However, in the past eight or nine years, the company has experienced a remarkable revival akin to a phoenix rising from the ashes. Embracing new growth opportunities, the business has witnessed an explosive surge in market capitalization. Currently, with a valuation of over $2.96 trillion, it stands as the second-largest publicly traded company globally, trailing only consumer tech giant Apple Inc. (AAPL).

Given this substantial upswing, investors might be concerned about overheated stock prices, reminiscent of the late 1990s. They might question whether the lofty expectations tied to the rise of quality AI could potentially disappoint. However, a careful analysis of the data and driving forces behind the company’s growth suggests that while AI holds promise to fuel future expansion, Microsoft’s long-term investment appeal does not hinge solely on the success of its AI ventures but rather on its steadfast positioning as a high-quality business at a reasonable price.

Robust Performance Endures

In recent times, my focus in articles about Microsoft revolved largely around its acquisition of video game behemoth Activision Blizzard, as evidenced in my previous piece. However, Microsoft’s offerings extend far beyond gaming initiatives. While my intention with this article isn’t to delve deep into each operating segment, a brief refresher could prove beneficial.

Operationally, Microsoft encompasses three primary segments. Firstly, the Productivity and Business Processes division encompasses a range of offerings, including ownership of LinkedIn, Microsoft 365 consumer subscriptions, and Office 365 subscriptions. Secondly, the More Personal Computing segment comprises various components such as Windows, gaming endeavors, and devices like the Surface. This segment also includes services like Microsoft News and Bing. Lastly, the Intelligent Cloud segment spans the company’s public, private, and hybrid server products and cloud services, notably Azure, a direct competitor to Amazon.com Inc.’s (AMZN) AWS.

Considerable excitement surrounds the potential of AI to enhance Microsoft’s financial performance in the future. Management has actively integrated AI into its operations. For instance, within Azure, the company facilitates the utilization of advanced models to optimize AI functionality. Customers can integrate their AI programs into other solutions to develop apps and services. Furthermore, Microsoft holds an ownership interest in OpenAI, the creator of ChatGPT, having invested $10 billion in 2023 following a $1 billion investment in 2019. The company also offers an AI ‘companion’ called Copilot for its customers.

Following the sustained robust performance, I upgraded my rating on Palantir Technologies Inc. (PLTR) from ‘sell’ to ‘hold’, conceding that the company had ‘broken my resolve.’ In one of my previous bearish articles about the firm, I acknowledged the immense potential of AI, estimating its contribution to the global economy to reach up to $15.7 trillion by 2030. Without a doubt, Microsoft stands to benefit from this expansion. However, I anticipate that its value will stem less from investments in OpenAI and Copilot and more from ‘owning’ an ecosystem that fosters AI innovation and evolves alongside it.

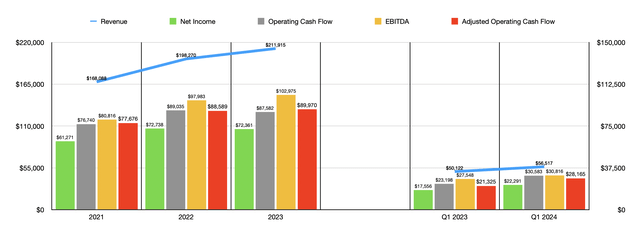

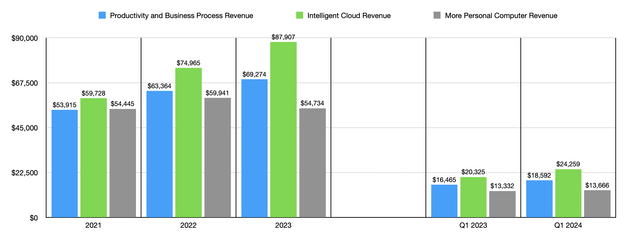

The potential upside for the company remains uncertain. Yet, even if we bank on the current trajectory persisting, shareholders should expect favorable outcomes. Consider revenue over the past few years — from 2021 through 2023, revenue expanded from $168.09 billion to $211.92 billion. In the first quarter of 2024, revenue of $56.52 billion surpassed the $50.12 billion reported in the same quarter of the 2023 fiscal year. As depicted in the chart above, profits have consistently mirrored the upward trajectory of revenue.

However, Microsoft comprises multiple operational segments. Notably, the More Personal Computer segment has not fared particularly well. Revenue remained relatively stagnant from 2021 through 2023 and in the first quarter of 2024, sales were only 2.5% higher than the preceding year. Conversely, all growth emanated from the other two segments. The Intelligent Cloud business, in particular, stands out as the most significant beneficiary of potential AI growth, regardless of the prevailing frontrunner in AI models. This is because the cloud simplifies the setup, management, and monetization of AI. As a major contender with one of the two largest cloud platforms globally, Microsoft is poised to reap substantial rewards.

Microsoft’s Financial Revelation: Unpacking the Surge in Cloud Operations

Microsoft, long revered as a stalwart in the tech industry, is currently experiencing an unprecedented surge in its Intelligent Cloud business segment. This revelation comes on the heels of a steady ascent in this domain over the past few years, with the Intelligent Cloud division ramping up its contribution to the company’s total revenue from 35.5% in 2021 to a staggering 42.9% in the first quarter of 2024. Simultaneously, the Productivity and Business Process segment has maintained its revenue share, presenting a dual-pronged growth strategy for the company. It’s an intriguing dynamic that signals a seismic shift for the corporate agenda and has far-reaching implications for stakeholders.

A Paradigm Shift in Profit Contribution

The pivotal uptick in Microsoft’s financial landscape is underscored by the Intelligent Cloud and Productivity and Business Process segments increasingly bolstering the company’s overall profitability. This has culminated in a tangible surge, particularly within the Intelligent Cloud segment, amplifying its significance within the conglomerate’s profit paradigm.

Margin Inflection Point

While the Productivity and Business Process segment has exhibited a commendable profit margin climb from 45.2% in 2021 to 53.6% in the first quarter of 2024, the Intelligent Cloud section has recently registered a notable improvement from a margin perspective. The continuing expansion of the firm’s cloud operations foreshadows a potential uptick in margins, poised to catalyze the company’s financial outlook. This promises a riveting arc in the profitability narrative, delineating a compelling trajectory for discerning investors.

The Midas Touch of Management’s Optimism

As the company hurtles toward the second quarter of the 2024 fiscal year, management’s optimistic guidance for a revenue projection of $60.90 billion signifies an auspicious surge. Conversely, analysts anticipate sales of $61.05 billion, catapulting the impending revenue to an enticing zenith. This meteoric rise, if materialized, would ensue that approximately 41.5% of the revenue emanates from the Intelligent Cloud operations, cementing its status as a fulcrum of profitability. Anticipating a robust profit per share of about $2.74 coupled with a surge in profits from $16.43 billion to $20.60 billion, all eyes are fixated on these pivotal metrics, integral in ascertaining the company’s true value.

The Gauntlet of Stock Evaluation

Naturally, skeptics highlight Microsoft’s lofty valuation, premising their reservations on the stock’s premium pricing and its relative historical benchmarks. However, contextualizing this against the backdrop of a burgeoning global cloud market, slated to burgeon at a cumulative annual growth rate of 14.1% from 2023 through 2030, propels the essence of Microsoft’s premium valuation. The company’s pivotal position at the vanguard of this burgeoning market augments the rationale for a premium valuation, underpinning a compelling case for astute investment.

Unveiling the Takeaway

Amidst this confluence of developments, Microsoft emerges not as a mere value play but as a prodigious growth prospect, potent enough to substantiate the market’s fervent demand for a slice of the pie. With its trajectory aligned with the burgeon in cloud operations, Microsoft beckons to investors with a discerning eye and a proclivity for embracing volatility, unfurling an opportunity that beckons prudent consideration.