Why the Neutral Rating?

AT&T (NYSE:T) is making efforts to transform its business for growth and operational efficiency, showing some progress. But there are lingering doubts. This leaves me with a ‘neutral/hold’ rating. I don’t anticipate the upcoming Q4 FY23 earnings on 24th Jan 2024 to alter my viewpoint, as I await consistent signs of growth and improved margins to solidify my faith in a genuine turnaround.

-

AT&T possesses a few growth drivers, but they fall short of delivering significant overall growth

-

Long-term margin improvement is anticipated, however, may not align with the guidance provided

-

AT&T trades at a discount compared to its counterparts, but the gap isn’t compelling enough to warrant a buy

I am keen to glean further insights into the sustainability of growth drivers from the management’s discourse during the Q4 FY23 earnings call and gain a deeper understanding of the pivotal catalyst (discussed later in this article).

The Quest for Meaningful Growth Continues

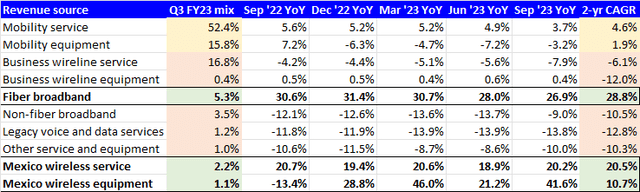

The primary takeaway from the table above is that AT&T generates the bulk of its revenue from services provided to Mobility (wireless) subscribers, accounting for 52.4% of the overall revenue mix in Q3 FY23. However, this segment has only seen a 4.6% CAGR over the last 2 years, with recent quarterly trends indicating a deceleration in growth. Most other business lines are experiencing declines. The only areas of growth are Fiber Broadband services and Mexico wireless operations.

When delving into the growth categories, the mix*2-yr CAGR figures provide a clearer picture of their contributions to overall growth, considering both the mix and absolute growth rates. Notably, the low revenue contribution mix of the growth engines (8.6%) has failed to meaningfully alter the company’s overall 2.2% nominal revenue growth. For context, the US nominal GDP registered an 8.4% CAGR over the past 2 years.

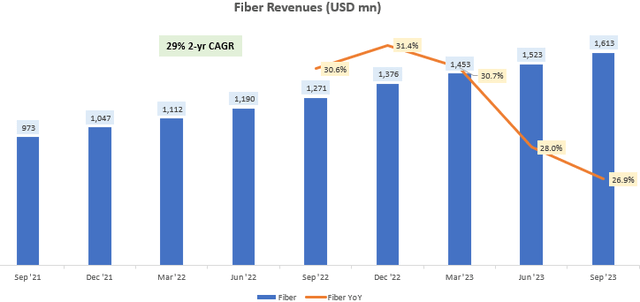

In recent earnings and discussions with UBS and Oppenheimer, much of the focus has been on the prospects of the US Fiber Broadband business, which has enjoyed a robust 29% 2-yr CAGR:

Notably, this growth has been propelled by pricing enhancements, with ARPU consistently rising from $58.17 to $68.21 over the past 2 years:

The sustainability of growth driven by pricing strategies is questioned by sell-side analysts in the Q3 FY23 earnings call, who seek insight into the potential for continued growth. Management has indicated further potential in FY24; however, skepticism looms over the sustainability of leveraging pricing in essentially a commodity service, particularly in the face of evolving industry competition and technology.

Furthermore, AT&T’s customer base predominantly comprises individuals with a higher willingness to pay. Data from a study on AT&T’s customer demographics reveals that 52% of its users fall in the top 1/3rd of monthly household gross income, in contrast to the broader mobile carrier users category at 34%. Thus, the company’s ability to rely on price hikes with other customer segments remains uncertain.

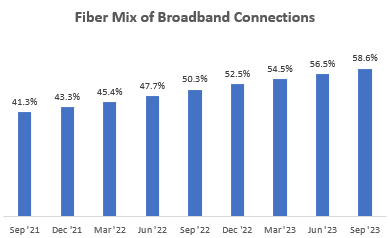

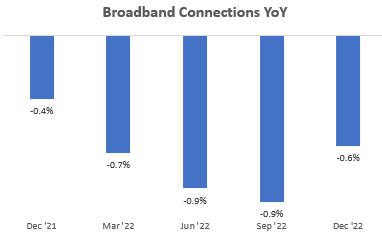

Shifting focus to volume growth analysis, it is evident that fiber volume growth has been driven by increased penetration of fiber-related broadband, with the fiber mix of AT&T’s overall broadband connections steadily rising by 1700 basis points over the past 2 years:

However, growth derived from increased penetration becomes progressively challenging. Notably, overall broadband connections have witnessed a year-on-year decline over the last 5 quarters, dropping from 13.8 million to 13.7 million:

While this may not be ideal, the CEO, John Stankey, expressed optimism during the UBS Conference call:

“I’d like to see us get into a unit growth business for customers as well. And I think we now have the formula where we can start to see that happen in ’24.” – CEO John Stankey, Author’s emphasis

It is expected that analysts will delve further into this during the Q4 FY23 earnings call, especially considering that it is typically the period for providing guidance. It is hoped that management will be more forthcoming in their responses.

Bridging the Margin Gap

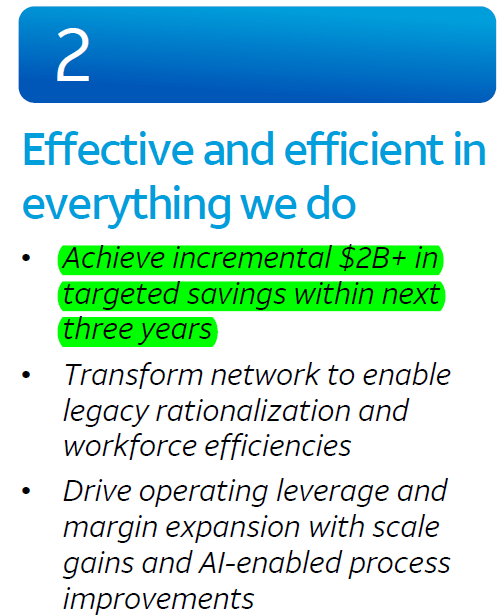

During the Q3 FY23 earnings call presentation, AT&T management outlined their focus on realizing $2 billion in savings over the next 3 years, implying a projected $667 million of margin accretion annually, assuming a linear run-rate improvement. This would be against the current TTM revenue base of $43 billion.

Evaluating AT&T’s Future Potential

When adjusted EBITDA is estimated to grow by 1.55%, it signals a positive trend in the company’s performance. The growth projections for FY24, currently standing at 1.23% for EPS growth, indicate a contrasting view. These figures, even factoring in some revenue growth, cast a shadow on the core operating margins level. Capital IQ’s data revealed a consistent underperformance with EBIT margins missing expectations by a median of 200 basis points since Q2 FY20, aligning with the tenure of CEO John Stankey, who assumed office in July 2020.

Discussing the Q4 FY23 earnings call, it’s expected to affirm the $2 billion savings objective over the next 3 years. Yet, a single quarter’s performance won’t drastically change the expectation of lagging behind consensus forecasts over the long term.

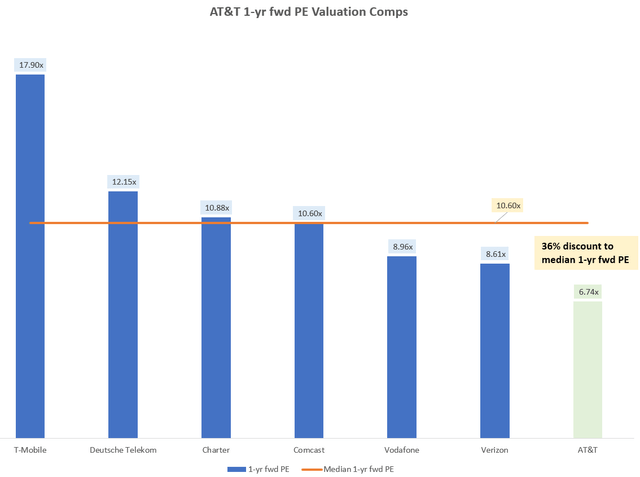

AT&T’s Valuation in Comparison to Peers

Among the comparables are T-Mobile (TMUS), Deutsche Telekom (OTCQX:DTEGY), Charter Communications (CHTR), Comcast (CMCSA), Vodafone (VOD) (OTCPK:VODPF), Verizon (VZ), AT&T (T)

The chart displays AT&T trading at a 1-year fwd PE of 6.74x. This represents a 36% discount from the median multiple of 10.6x. Although this might suggest an appealing value proposition, my investment strategy seeks a fusion of value and a key growth catalyst, which is yet to materialize.

Anticipating the Major Growth Driver

I perceive the US Broadband Equity Access and Deployment Program [BEAD] as the principal growth catalyst for AT&T. The anticipated $42.45 billion federal initiative for nationwide broadband rollout is expected to ignite robust volume growth in broadband connections, reversing the current trend of decline and further propelling fiber rollouts. However, signs indicate that this pivotal catalyst may not fully unfold until 2025:

Other than the wheels of government turn slowly, not really [any update on BEAD developments]… I think this is going to be a 2025-plus thing when kind of look at the aggregate portions of the build, the private capital that comes in and ultimately, customers that come on the network and start buying services that might not have been buying services before.

– CEO John Stankey in the Q3 FY23 earnings call

The US Government’s BEAD Information Sheet supports the notion that implementation post the final proposal will likely extend beyond 2025:

I anticipate the stock to experience a significant upward trajectory only around mid-late 2024, as the orientation of the market tends to look ahead. It is crucial to align with the timing of catalyst expectations versus their actual manifestation. This concept was further elaborated by investing luminary Stanley Druckenmiller, citing the importance of visualizing the future rather than being fixated on the present.

But before he left, he taught me two things. A, never, ever invest in the present. It doesn’t matter what a company’s earning, what they have earned. He taught me that you have to visualize the situation 18 months from now, and whatever that is, that’s where the price will be, not where it is today. And too many people tend to look at the present, oh this is a great company, they’ve done this or this central bank is doing all the right things. But you have to look to the future. If you invest in the present, you’re going to get run over.

– Stanley Druckenmiller

Therefore, any insights into the progress on the BEAD catalyst in the upcoming Q4 FY23 earnings call are highly anticipated by investors.

Insight from Technical Analysis

For those unfamiliar with my approach to Technical Analysis, a primer explaining my method using the principles of Flow, Location, and Trap is available for reference.

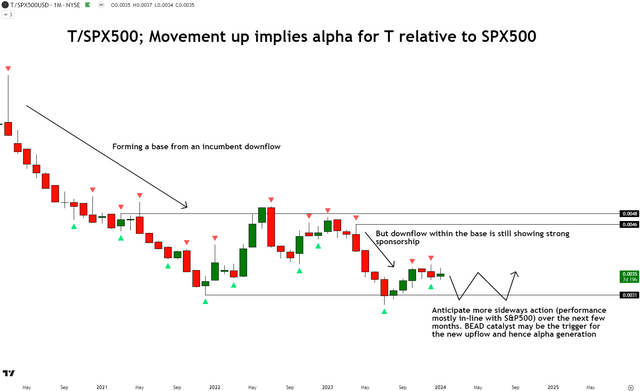

Assessing the relative monthly chart of T/SPX500, the consolidation of ratio prices is evident, indicating a pause in the downward trend. Despite the consolidation, the ongoing downward trend suggests that a significant turnaround may be distant. Hence, I anticipate further sideways movement for several months until closer to the BEAD catalyst’s impact. While there may be movements due to earnings surprises, I don’t foresee these significantly altering the prevailing expectations.

Assessment and Outlook

AT&T experiences growth drivers in its Fiber business and Mexican operations, yet these are overshadowed by declining segments, which constitute a larger portion of revenues. Consequently, the company’s topline growth has trailed behind US nominal GDP growth rates. The growth in the fiber business has largely stemmed from price hikes, which may not be a sustainable long-term driver. What’s imperative is volume growth, particularly in broadband connections, which currently exhibit a decline. I don’t forecast a substantial change until the US government’s broadband rollout catalysts (BEAD) come into full play from 2025 onwards.

Regarding margins, the management aims to achieve $2 billion in margin accretion from cost savings over the next 3 years. However, consensus estimates appear to factor in a slightly lower accretion. Considering the history of management falling short on EBIT expectations, there’s a potential for disappointment even with the downwardly adjusted expectations over the medium to long term.

Although trading at a 36% discount to peers based on a 1-year fwd PE basis, AT&T may present an attractive value proposition. Nonetheless, for my investing approach, which demands an operational catalyst, this isn’t adequate to warrant a buy recommendation. Hence, my assessment renders the stock a ‘neutral/hold’. This stance is unlikely to transition even after the impending Q4 FY23 results, as I seek at least two quarters of evidence showcasing volume growth improvement, ideally spanning 6-12 months before the BEAD catalyst takes effect.

Interpreting Hunting Alpha’s Ratings:

– Strong Buy: Anticipate the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

– Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

– Neutral/hold: Anticipate the company to perform in-line with the S&P500 on a total shareholder return basis

– Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

– Strong Sell: Foresee the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views ranges from multiple quarters to around a year. While not immutable, I will share any changes in stance in a pinned comment to this article and may also publish a new article detailing the reasons for the altered viewpoint.