Let’s delve into one of the smaller firms on my radar: Atkore Inc. (NYSE:ATKR), a company I commenced covering on August 27, 2023, under the moniker “Atkore: A Top-Tier Industrial Mid-Cap Play.”

Several months ago, I introduced a compelling mid-cap play with substantial exposure across a broad spectrum of non-residential, residential, construction, and industrial markets.

While Atkore’s roots reach back to the 1950s, Atkore Inc. was established as a Delaware company in 2010. It’s the parent company of Atkore International Holdings and Atkore International.

[…] Atkore operates in two core segments:

Electrical products for the construction of electrical power systems

Safety and Infrastructure products for critical infrastructure protection

Roughly half a year later, I’m revisiting the stock. Not only did the company just report its 1Q24 earnings, but it also initiated a dividend, which could mark the birth of a highly successful dividend growth stock.

Although I made the case in my prior article that I won’t be a buyer of ATKR due to my investment in Carlisle Companies (CSL), I’m changing my mind.

If I can get ATKR on a potential correction, I’ll happily make it a part of my dividend (growth) portfolio.

Now, let’s dive into the details!

Economic Performance

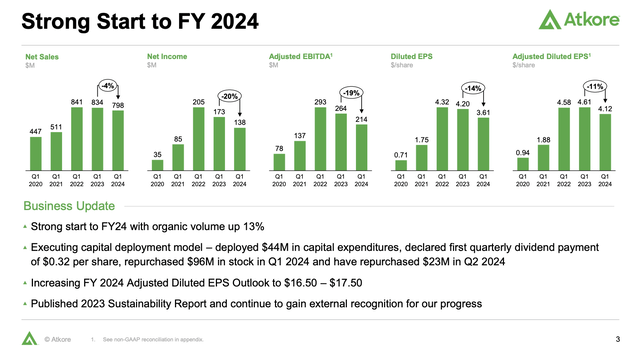

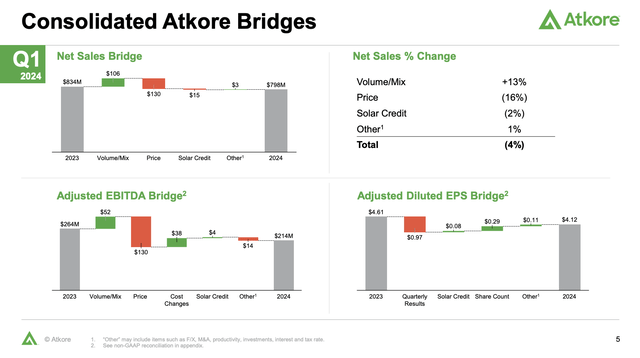

Let’s commence with the not-so-great news. Atkore is not immune to economic headwinds, as net sales for the first quarter of 2024 reached $798 million, signifying a 4% year-over-year decline.

Adjusted EBITDA declined by 19%. Net income contraction was slightly worse at negative 20%.

However, organic volume growth was a standout number, surging by an impressive 13% across all key product areas.

Despite this commendable performance, the gains were partially offset by the ongoing pricing normalization, in line with the company’s previously communicated trends.

Notably, the volume expansion was most prominent in the classic pipe and conduit category, recording high-single-digit growth, primarily driven by robust demand for PVC products.

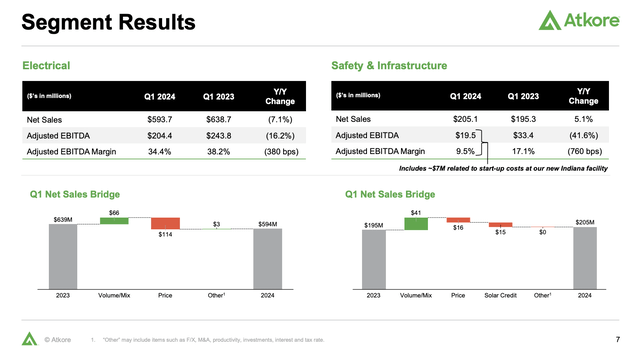

Segment-wise, both the Electrical and S&I segments showed positive volume growth.

However, the Electrical segment experienced margin compression, attributed to the mentioned pricing normalization, which, nonetheless, remained strong at 34%.

On the S&I side, there was year-over-year margin compression due to cost comparisons against the prior year and planned start-up costs in Indiana aimed at supporting volume ramp-up.

Before I delve into the expected ramp-up in volumes, it’s important to note that the company maintains a robust balance sheet.

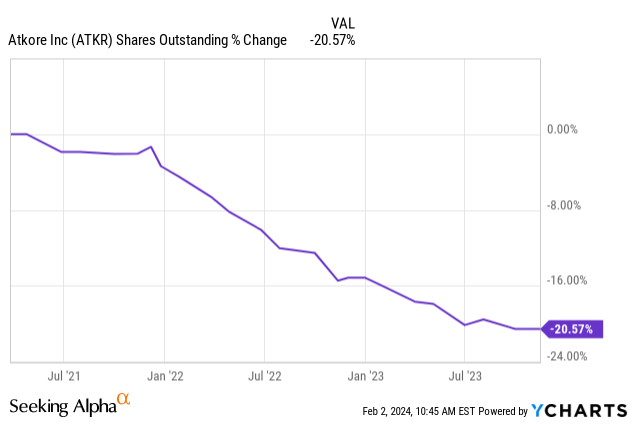

The company has no debt maturities until the 2028 fiscal year and used close to $100 million in 1Q24 to buy back stock.

Over the past three years alone, the company has bought back a fifth of its shares!

Data by YCharts

Overall, the company maintains a very healthy balance sheet, as it has just $763 million in gross debt. Adjusted for cash and cash equivalents, it has $382 million in net debt, which is just 0.4x 2024E EBITDA.

Speaking of this year’s expected EBITDA, the company is upbeat about its future, which includes the introduction of a dividend.

The Birth of a Dividend Stock

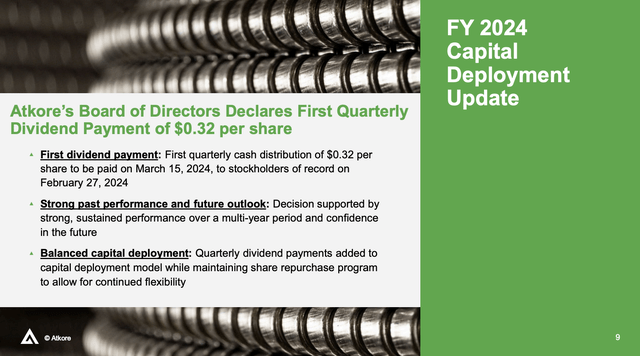

Thanks to strong free cash flow and a healthy balance sheet, ATKR introduced a dividend.

The first dividend will be $0.32 per share, which will be paid to shareholders of record on February 27, 2024.

This dividend translates to a yield of 0.9%.

At this point, you’re probably thinking something like, “So what, 0.9% won’t make a big difference!”.

Sure, a 0.9% yield means you get $90 in dividends from a $10,000 investment. That is not a lot.

However, this is just the start.

Not only does this signal that the company has a lot of confidence in its future, but we also…

Atkore: A Hidden Gem in the Industrial Sector

Atkore: A Hidden Gem in the Industrial Sector

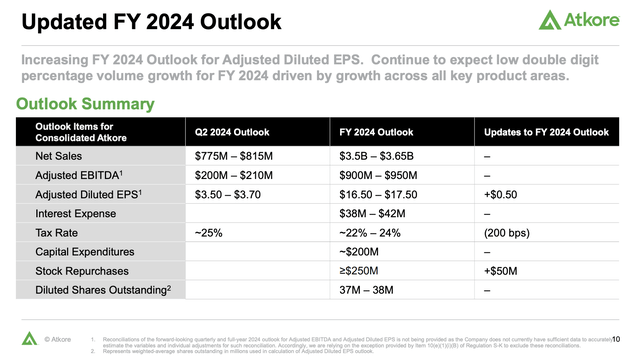

Potential investors should take note of the substantial room for the company to expand its dividend. The company is predicted to generate between $16.50 and $17.50 in annual EPS. If the $17 EPS guidance midpoint is used, this would result in a payment ratio of just 8%, making it one of the lowest payout ratios in the industrial sector at large, not just within its own industry. Maintaining a 40% EPS payout ratio could potentially yield 4.5%. Analysts also anticipate the company to produce over $420 million in free cash flow this year – indicating an 8% free cash flow yield or an 11% cash payout ratio. This suggests the potential for significant dividend growth rates in the coming years, supported by aggressive buybacks.

Positive Outlook

Atkore maintains its expectation of attaining low double-digit percentage volume growth for the full fiscal year 2024. Despite challenges, such as adverse weather conditions affecting performance in January, the company is unwavering in its outlook for full-year net sales and adjusted EBITDA. Additionally, the company foresees a sequential improvement in adjusted EBITDA from the second quarter to the third and then from the third to the fourth quarter.

Image

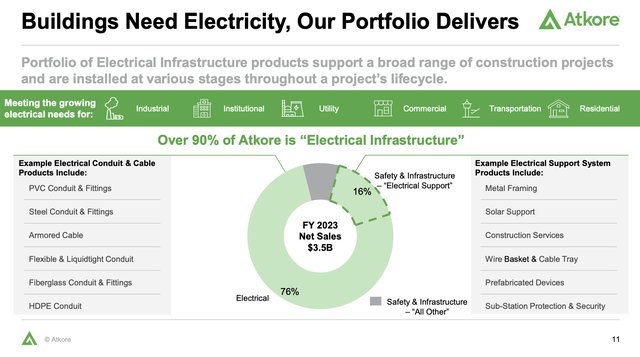

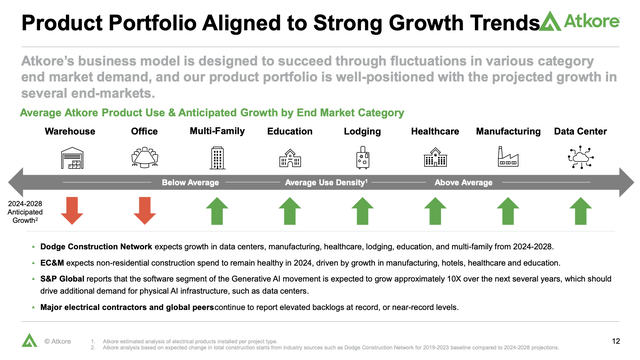

Furthermore, Atkore highlights its robust position within the electrical industry, with over 90% of its product portfolio supporting electrical infrastructure. The company’s optimism is bolstered by anticipated growth in key end-market categories such as data centers, manufacturing, lodging, healthcare, education, and multifamily. This favorable industry outlook aligns with reports from other major public electrical contractors and peers, which have indicated record backlogs and project positive growth, instilling confidence in the future of the entire industry.

Given the remarkable transition of the company, it appears well-positioned to deliver robust dividend growth and buybacks, potentially outperforming its industrial peers over the long term. Over the past five years, ATKR yielded over 540%, surpassing the Industrial Select Sector ETF (XLI) by a significant margin.

Image

Although a future return of 45.9% per year is not expected, the company seems poised to maintain heightened growth. With a market cap of less than $6 billion and limited analyst coverage, the stock is currently flying under the radar. However, once it grows, it is likely to attract more attention and investment. Valuation-wise, the company is trading at just 8x 2024E EPS, utilizing the midpoint of its guidance. Even if the company grows its EPS by just 6% per year after 2024, an 8x earnings valuation still seems undervalued. Gradually moving to a >12x EPS valuation could pave the way for >15% annual returns in the years ahead, even with subdued EPS growth rates.

Image

The only reason I have not become a shareholder yet is that I am contemplating how to structure my portfolio due to adding another industrial stock. Additionally, I have my eye on a few other players, including Amphenol (APH), and I already own Carlisle. Moreover, given the recent market rally, I am exercising additional caution in deploying substantial cash. Regardless, I firmly believe that ATKR is an excellent stock that is likely to continue functioning as a wealth generator for its investors.

Key Takeaway

Atkore has emerged as a compelling investment, with its recent dividend initiation signaling confidence in future growth. The introduction of the dividend, beginning at 0.9%, opens up the potential for significant future growth, given its low payout ratio. Despite encountering economic headwinds, the company has demonstrated robust organic volume growth, particularly in the electrical sector. With a promising industry outlook and a track record of outperforming, ATKR, currently undervalued at 8x 2024E EPS, presents an exciting opportunity for long-term investors.

The free Daily Market Overview 250k traders and investors are reading