Insights into CME Group

CME Group (NASDAQ:CME) is scheduled to announce its FY23 earnings on the 14th of February before the opening bell. Amid a period of economic uncertainty, characterized by heightened market volatility, the company has experienced a surge in trading activity, driving substantial revenue growth. Anticipating this trend to persist, CME Group’s financial outlook appears promising, positioning it as an attractive investment opportunity.

A Glimpse at the Company

CME Group operates as a global platform facilitating the trading of futures and options contracts. Through its platform, CME Globex, the company connects buyers and sellers to engage in these transactions. Additionally, CME Group provides essential clearing services, ensuring the completion of every trade, even in the event of default by one party, albeit with additional fees.

Exploring the Financial Landscape

As of Q3 ’23, the company boasted approximately $2.4 billion in cash and equivalents, while carrying long-term debt of around $3.4 billion. Demonstrating commendable financial prudence, CME Group maintains a robust solvency position, supported by a debt-to-assets ratio comfortably below 0.6 and a debt-to-equity ratio well under 1.5. Furthermore, the company’s interest coverage ratio registers over 20x, signifying ample capacity to meet debt obligations even under adverse performance conditions.

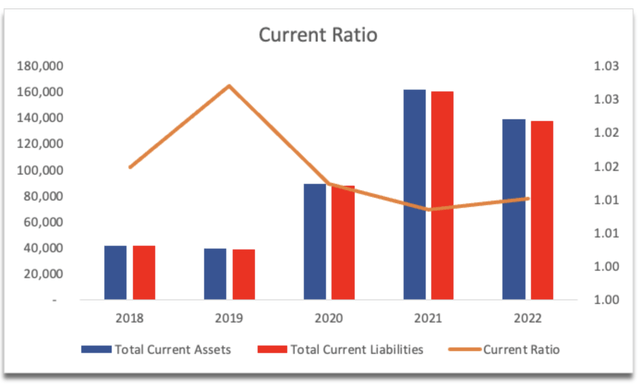

The company’s consistent current ratio, hovering around 1 over the past decade, attests to its sound liquidity position, devoid of any imminent challenges.

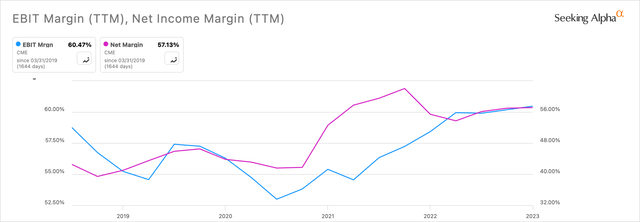

While CME Group’s gross margins remain indistinct due to the absence of cost of goods sold (COGS) disclosure, both its EBIT and net margins exhibit robust performance, rebounding impressively since the onset of 2021. Notably, the company operates in a high-margin industry, an appealing attribute for potential investors.

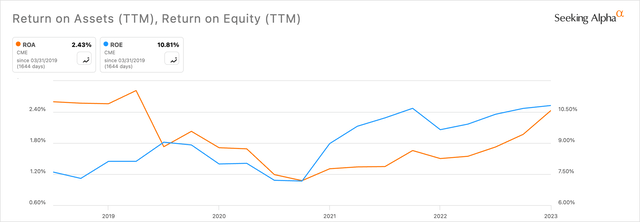

Amid efficiency and profitability considerations, the company’s return on assets (ROA) and return on equity (ROE) appear meager, influenced by its asset-heavy nature tied to performance bonds and guaranty fund contributions. Operating as a protective reserve against potential member defaults within the clearing house, this asset pool, predominantly invested in risk-free securities, garners only modest returns. Consequently, while achieving enhanced ROA and ROE figures remains desirable, the intricate nature of this asset class poses challenges.

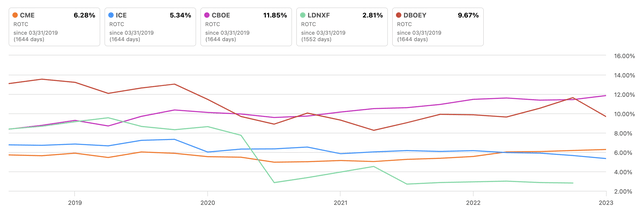

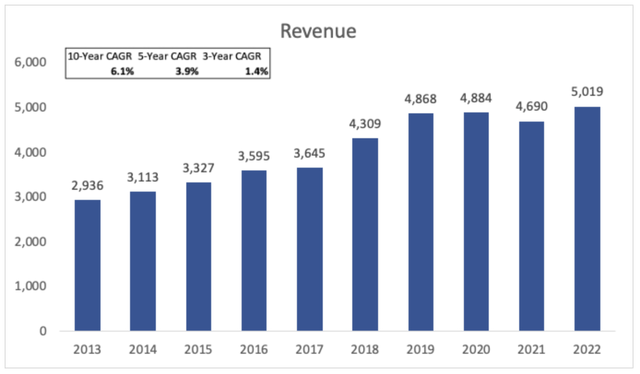

Assessing its competitive edge, CME Group stands as a prominent player in an industry with limited public counterparts. Notably, the company’s return on total capital ranks competitively amidst its peers, signaling its relative strength. However, its revenue growth over the past decade, showing a modest 6% increase, coupled with recent decline, presents a deterrent for investors focused on top-line growth. Nevertheless, potential value enhancement through operational improvements remains a plausible prospect.

Overall, CME Group has maintained consistent operational performance over the past decade, indicative of stability. While not reflective of exponential expansion, this steadfast trajectory presents a favorable alternative to tumultuous fluctuations. Amidst recent operational pondering, the company continues to exhibit resilience in navigating challenging market dynamics, imbuing optimism for sustained growth.

CME Group: A Closer Look at the Potential Ahead

Recent market behavior has been anything but predictable, leaving investors anxious about what to expect next. Amidst this backdrop, one company, CME Group, stands at the crossroads of opportunity and uncertainty. As CME Group prepares to release its upcoming earnings, let’s dissect the crucial elements at play and evaluate the potential for growth and stability in the foreseeable future.

Earnings Outlook

Analysts have set their sights on CME Group’s upcoming earnings, projecting GAAP and adjusted EPS to land at $2.18 and $2.28, respectively, on $1.43B revenues. While the management has been tight-lipped about providing a specific top-line figure for the upcoming Q4, a proximity to analyst predictions wouldn’t come as a shock. Notably, CME Group has consistently outperformed on EPS over the past 12 quarters, albeit encountering five misses on revenue. This track record suggests a high likelihood of exceeding EPS expectations while potentially falling short on revenue once again.

Furthermore, the management has disclosed an anticipated expense figure of around $1.535B for the year, excluding license fees. Looking ahead, analysts foresee nearly 11% growth in top-line revenue for FY23, a stark contrast to the average, with subsequent years tapering down to approximately 3%. However, these projections must be taken with a grain of salt, given the inherent uncertainty prevailing in the current economic climate.

Insights into the Outlook

The macro environment’s unpredictability may, surprisingly, work to CME Group’s advantage. The volatility stemming from uncertainties often drives clients to seek hedging solutions, amplifying trading activity and, consequently, boosting revenue growth for CME Group. Additionally, the subdued FY23 revenue growth estimates reflect the ripples of a turbulent and uncertain year, with a sudden upswing in the last three months. As the U.S. job market signals robustness, the prospect of rate cuts dwindles, setting the stage for heightened market volatility, a harbinger of potential success for companies like CME Group, reliant on trading activity.

The surge in trading activity is evident from the substantial increase in stock index options and futures contracts traded in the initial half of ’23, surging by approximately 81% year-over-year, with options volume surpassing a 100% surge. Notably, the APAC region accounted for roughly 89% of the total volume of contracts traded, underscoring a shifting landscape in investment preferences.

Furthermore, the rising popularity of options trading parallels the burgeoning interest in cryptocurrencies. The possibility of CME Group expanding its repertoire to include more cryptocurrency-related products could potentially capture a larger investor base. However, the foray into such ventures must be navigated cautiously, given the prevalence of fraudulent coins alongside the speculative nature of cryptocurrencies.

In essence, the steady growth in options volumes is indicative of a potential resurgence in CME Group’s top-line growth, with technological advancements serving as a catalyst, facilitating seamless and instantaneous transactions, bolstering its competitive stance.

Valuation and Risks

Ascertaining a fair value for the company involves treading cautiously, especially in light of the persisting market vagaries. With a conservative approach, estimated conservative CAGR in revenues over the next decade hovers around 4%, ensuring a wider margin of safety amid the prevailing uncertainties. A moderated estimation between GAAP and adjusted EPS conveys a balanced outlook for margins and EPS, demonstrating a judicious stance toward future company prospects.

Employing the company’s WACC of approximately 6% for the DCF model, with a 2.5% terminal growth rate and an additional 20% discount on intrinsic value, the intrinsic value of CME Group is estimated at around $217 per share, signifying a meager 5% discount from its fair value.

On the other hand, potential regulatory changes could impose higher costs on CME Group, potentially denting its trading activity and hindering top-line growth. Moreover, stiff competition poses a significant threat, potentially eroding CME Group’s market share and diminishing its edge. The specter of an economic slowdown looms large, casting shadows on trading volumes and appetite for risk, which could impede CME Group’s top-line growth.

Parting thoughts

Navigating the currents of uncertainty and promising potential, CME Group beckons shrewd investors with its enduring presence and the promise of sustained performance. A steady, albeit unassuming growth trajectory is poised to align with technological advancements, further enhancing the company’s competencies in a swiftly changing landscape. It’s in this light that I initiate coverage on the company with a favorable buy rating, anticipating gratifying long-term outcomes owing to CME Group’s resilience and growth synergies.