Do yourself a favor.

Don’t do a Google search for “worst Valentine’s Day cards ever.”

It’s really not worth it.

Sure, you might find some funny ones in there such as a quote from The Office‘s Dwight saying:

“All you need is love: False. The four basic human necessities are air, water, food, and shelter.”

And the UUEFKTN Ted Lasso one that reads, “You make me feel like I fell out of the lucky tree and hit every branch on the way down” is mildly amusing too.

But overall, I’d call them bewildering.

They make me wonder what in the world the creators were thinking.

One of the “better” – if I can even use that word here – examples is the WOWcard with a banana on it that says, “In banana years, you are bread.” It’s listed on Amazon as:

“Banana pun card, funny puns anniversary card, funny birthday card, I love you card, Thank you card, Valentine

day card, card for husband wife boyfriend girlfriend, cute greeting card.”

Judging by the rest of the description, it seems clear that English is not the maker’s first language.

So who knows… maybe in his or her culture, such a bold crack about someone’s age generates warm fuzzy feelings galore.

But if I tried giving that to MY wife?

Let’s just say I’d be sleeping on the couch for a month.

Or more.

Fortunately for all of our relationships this Valentine’s Day, there are much more appropriate gifts to get.

Valentine’s Day Gift Guide: Financial Edition

Look guys (and gals too – even though you tend to be much more savvy when it comes to gift-giving), sometimes the answer is simple.

Chocolates, flowers, and/or jewelry, topped with a sweet, sincere card. It really doesn’t need to be more difficult than that.

Of course, there’s the matter of personality to consider. What is her (or his) exact taste?

If your valentine is a no-muss, no-fuss type, then the stereotypical dozen red roses and “I love you so much” card might be all she really wants. Or if she’s into the finer things, you should probably add a trip to the jewelry store.

Is she a stereotypical, pink-loving, self-proclaimed “girly girl?” She might melt at a pair of sparkling, dangly earrings.

Is she obsessed with fitness? Cut out the chocolates and replace it with a romantic dinner at a tasty, trendy, health-conscious restaurant.

Is she the mother of your still-in-the-house children? In that case, a spa day might be in order.

But one way or the other, just try combining common sense with who your significant other is.

Oh. And your budget too. No offense to the high-maintenance guys and gals out there, but Valentine’s Day is not a good reason to go into debt.

There are actually very few reasons to “go” there, including if you’re:

- Starting or running a business – in an intelligent fashion

- Buying a home

- Advancing your education (again, in an intelligent manner).

How about using leverage to buy stocks?

That’s a whole different discussion for a whole ‘nother day. This day is about real love and how to express it.

Which is why I’d like to point you to several sweet REITs that are hard to beat.

“Oh Baby, I Can’t Think of Anyone Else I’d Rather Be Bored With”

Nothing says “I love you” quite like financial stability.

And nothing says “financial stability” quite like safe, steady, growing real estate investment trusts.

I know they seem boring, especially in this market where stocks like Nvidia Corporation (NVDA) can climb 19% in a single day.

But I will point out Yahoo Finance’s post from Friday (February 9), which highlighted how Nvidia “has rallied so much this year… it’s now threatening to overtake Amazon.com” as “the fourth-most valuable U.S. company.”

Call me a coward if you’d like. But I’m just not comfortable putting the same value on a tech company that reported total revenue of $26.97 billion in the year ending January 31, 2023, as one that reported over $500 billion in that same basic timespan.

And there are similar discrepancies in gross profits and year-over-year gains.

To me, that’s the same as trying to equate puppy love with married-for-25-years-or-more love. The first might end up becoming the second, but treating them equally right from the get-go is risky.

As the Yahoo Finance article adds:

“The shares are up more than 40% so far in 2024 amid signs that demand for its chips used in artificial intelligence

computing remains strong. But the stock has run so far, so fast that it’s reigniting concerns about whether the

gains are sustainable, ahead of Nvidia’s earnings due later this month.”

This might make me old, but I think being able to continue providing a roof over my family’s heads in beds we can sleep well in with no fears about our financial future…

That’s better than all the sparkly, shiny things in the world.

Except on Valentine’s Day, of course. Because you’d better believe I’m using common sense to get my wife something nice along with the following lovely REITs.

Realty Income Corporation: A Fortress of Stability in Investment Landscape

Valuation and Quality

When it comes to real estate investment trusts, Realty Income is a name that strikes a chord with seasoned investors. With a solid footing in the market, this company upholds the principles of safety and stability, making it an attractive choice in a volatile investment landscape.

Credit Ratings and Economic Headwinds

Especially in the wake of concerns such as sticky inflation and elevated rates, the focus on safety becomes paramount. Realty Income, with its BBB+ credit rating, is a standout choice, given the unpredictable economic climate.

Default Probabilities and Delinquency Rates

An examination of historical data reveals that companies with an A rating or better have shown a low 15-year default probability of less than 2%. In contrast, entities with lower ratings have faced delinquency rates and probabilities that raise red flags, emphasizing the significance of a high credit rating.

Realty Income’s Resilience

Grounded in a blend of income, consistent growth, and a robust balance sheet, Realty Income stands as a beacon of stability in the investment landscape. The company’s focus on quality and financial strength makes it a reliable choice for investors seeking long-term security in their portfolios.

A Robust Track Record

Realty Income, also known as “the monthly dividend company,” boasts a legacy spanning over half a century and 29 consecutive years of dividend growth. The company’s commitment to consistent dividend increases, even during turbulent economic periods, reflects its resilience and financial prudence.

Diversified Portfolio and Strategic Acquisitions

Realty Income’s portfolio encompasses over 13,000 commercial properties across the United States, the United Kingdom, Spain, Italy, and Ireland, with a strong focus on retail properties. The company’s strategic acquisitions, including partnerships with major industry players, further enhance its market position and diversify its assets.

Tenant Base and Market Position

The company has strategically aligned itself with reliable tenants such as Dollar General, Walgreens, Dollar Tree, and 7-Eleven, providing a solid foundation for sustained growth and stability. This positioning, coupled with a focus on anti-cyclical segments, bolsters Realty Income’s position in the market.

Performance and Market Resilience

Realty Income’s consistent performance is evident in its impressive portfolio occupancy rate of 98.8% and a weighted average lease term (“WALT”) of 9.7 years, reinforcing its reputation as a low-risk investment option. With an annualized return of 13.4% since 1994 and a beta of 0.5 compared to the S&P 500, the company offers investors superior market performance with minimized risk exposure.

Attractive Valuation and Conclusion

In addition to its strong fundamentals, Realty Income is attractively valued, offering investors a compelling value proposition. With its unwavering focus on quality, stability, and financial prudence, Realty Income remains a standout choice for investors seeking a fortress of stability in today’s dynamic investment landscape.

The Dynamic Duo of Real Estate Investment Trusts

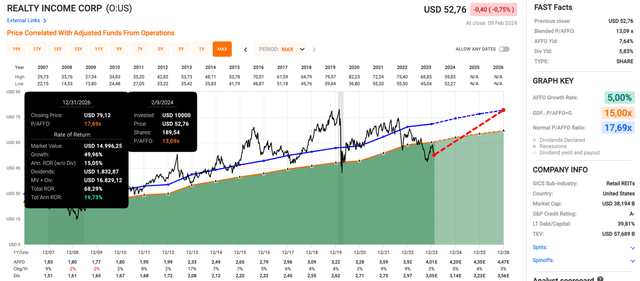

Realty Income, a strong player in the Real Estate Investment Trust (REIT) arena, epitomizes resilience with its current trading position at a blended P/AFFO of just 13.1x against a normalized valuation of 17.7x. This discrepancy has investors raising their eyebrows, as the company is expected to showcase a 5% growth in AFFO this year, followed by 4% in 2025 and 3% in 2026. The discount is attributed to the looming threat of prolonged elevated funding rates and inflation – indeed, storm clouds on the horizon. If REITs were characters in a Raymond Chandler novel, Realty Income might be the tough-talking gumshoe under the streetlamp in a dark alley – battered but unbeaten. This tough stance expresses the potential for up to a 20% annual return, inclusive of dividends, as the company claws its way back to normalized valuation.

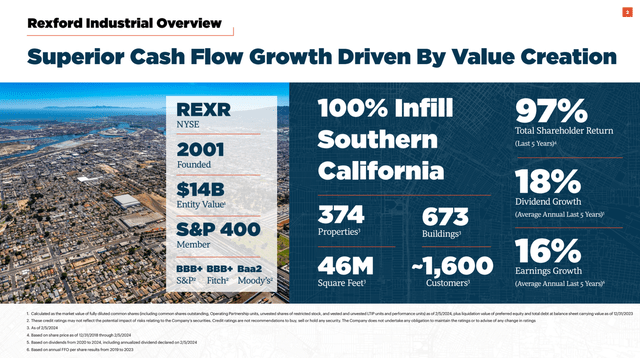

And now, stepping into the ring with a lower yield but promising growth is Rexford Industrial Realty, Inc. (REXR) – a heavyweight with a BBB+ credit rating and a track record leaving investors breathless. REXR, an industrial REIT, might seem like the wild card in the REIT deck, yet this California-based juggernaut has been delivering knockout blows, with an annual return of 16.3% since its IPO in 2014.

Rexford Industrial Realty, Inc. (REXR) – 3.2% Yield

Rexford, the rising star of industrial REITs, has a special place in the spotlight with a strategic focus on the effervescent Southern California market. With a portfolio enviously bulging with over 670 buildings across 374 properties, serving around 1,600 tenants, Rexford caters primarily to warehousing, transportation, wholesale trade, and manufacturing sectors. Its clientele includes the heavyweights of the transportation and aerospace industry, and the leading lights of automotive and EV suppliers.

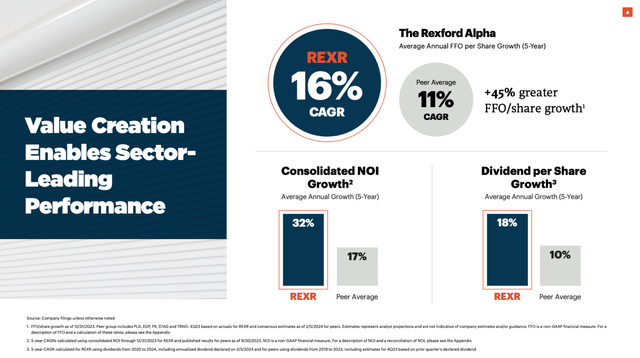

Benefiting from a robust tenant demand and the vibrant dynamics of the Southern California market, Rexford has been a beacon of growth, with funds from operations (“FFO”) per share soaring by an astonishing 16% annually over the past five years – leaving its peers in the dust with their respectable 11% growth rate. Talk about a company setting the pace!

During its recent earnings call for the fourth quarter of 2023, Rexford fired on all cylinders, underlining its position to seize growth opportunities within the infill Southern California industrial markets. The company emphasized a robust pipeline of value-added repositioning projects and the potential for substantial rent escalations, geared to fuel further expansion and value enhancement.

Looking ahead, Rexford anticipates a staggering 42% internal cash net operating income (“NOI”) growth over the next three years, translating to an impressive $240 million incremental NOI within its existing portfolio. This trajectory is expected to send total cash NOI to over $800 million during the same period, assuming current rental rates and no additional acquisitions – an ambitious game plan indeed.

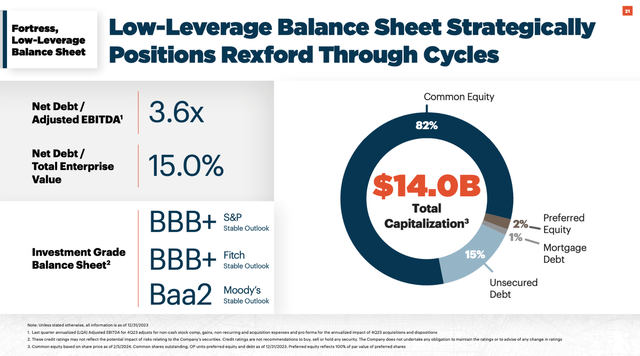

Fueled by a low-leverage balance sheet and substantial liquidity of $1.2 billion, including full availability on its $1 billion line of credit, Rexford’s firepower is undeniable. Moreover, with market rents for properties similar to those in its portfolio showing stability and a low infill market vacancy rate, the company’s market positioning remains exceptionally strong – no mere flash in the pan.

In the SoCal industrial real estate market, the demand is formidable, and supply shortages prevail. California still holds the title for the biggest industrial market, with an uber-sized customer base. Rexford is right in the thick of this scuffle – a heavyweight in a high-stakes bout.

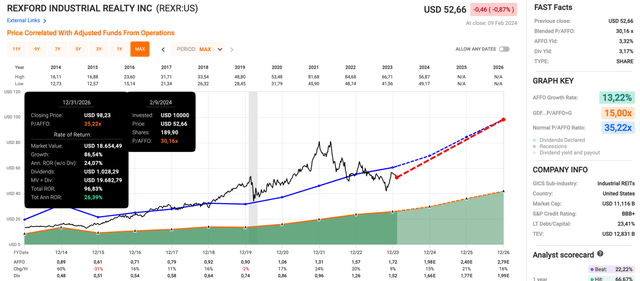

Riding on the back of these powerful forces, Rexford announced a robust 10% increase in its first-quarter dividend, yielding 3.2% and supported by an 84% 2024E adjusted FFO payout ratio. The stock seems to be attracting attention, accounting for a blended P/AFFO ratio of 30.2x in trading, with a long-term normalized valuation multiple of 35.2x. With an expected 15% AFFO growth in 2024, followed by 21% in 2025 and 16% thereafter, it makes a compelling case for an annual theoretical return of 26.4% – a proposition that’s hard to ignore.

The Love Language of REITs: Realty Income, Rexford, and VICI Properties

The market is like a fickle Valentine – ever-changing, sometimes unreliable, but the love for real estate investment trusts (REITs) endures.

Realty Income Corporation (O) – 4.4% Yield

In the world of investing, some things never go out of style, much like the timeless appeal of flowers and chocolates on Valentine’s Day. Among the stalwarts, Realty Income Corporation (O) brings the promise of consistent returns and enduring stability to the table.

With over five decades of uninterrupted dividends, Realty Income has remained the ‘steady Eddie’ of the REIT world, earning the trust of income-seeking investors with its remarkable track record. Sporting a 4.4% yield, this investment embodies the reliability of a long-term, committed relationship.

Akin to a perennial bouquet delivering soothing fragrances throughout the seasons, Realty Income is not just surviving but thriving through ever-changing market conditions. The company’s resilience is reminiscent of enduring affections, creating a deep sense of trust among Income investors even in the most volatile times.

Rexford Industrial Realty, Inc. (REXR) – 1.1% Yield

In a market landscape akin to a bustling city street on Valentine’s Day, Rexford Industrial Realty, Inc. (REXR) stands out like a vibrant bouquet in a sea of ordinary gifts. With a mere 1.1% yield, REXR, much like an exciting first date, offers the promise of growth amidst the rush of Southern California’s industrial real estate sector.

Just as flowers are a timeless way to convey affection, the allure of REXR comes from its potential to flourish, much like a budding romance. As a REIT on the rise, it holds the promise of providing investors a dynamic, stimulating experience with its rapid development in the thriving Southern California market.

While it may take a while until rates come down substantially, REXR is one of the most promising REITs on our radar, benefitting from safety, growth, and secular benefits in its home market and industry.

VICI Properties Inc. (VICI) – 5.6% Yield

When it comes to preparing something special for Valentine’s Day, there are not many cities as accommodative as Las Vegas, a city that is home to some of the fanciest restaurants and hotels in the world. And standing amidst the glittering lights of the Vegas strip, VICI Properties Inc. (VICI) shines as a prominent player, ready to woo investors with its strategic approach and promising outlook.

Much like a luxurious gift that promises indulgence, VICI captivates with an appealing 5.6% yield, swiftly expanding its portfolio while smartly diversifying its assets and maintaining a robust balance sheet, setting the stage for potential outperformance in the REIT sector.

With an approach like a carefully curated fine dining experience, VICI focuses on quality over quantity, minimizing risks despite its focused tenant base, and ensuring steady cash flows from its high-profile tenants such as Caesars Entertainment and MGM Resorts. This unique strategy adds a touch of exclusivity, much like a coveted reservation at an upscale restaurant.

Essentially, what sets VICI apart is its non-commoditized real estate and triple net lease agreements, mitigating risks and ensuring steady cash flows. Moreover, with an average lease term of 42 years, VICI enjoys remarkable stability, supported by 100% rent collection even during challenging times like the global pandemic of 2020.

With a seamless expansion plan beyond Vegas and a healthy balance sheet, VICI presents an attractive 5.6% dividend yield and an alluring growth potential, resembling a lavish gift promising both stability and excitement.

Takeaway

When it comes to expressing love on Valentine’s Day, skip the risky business of offbeat gifts and focus on what truly matters: financial stability and thoughtful gestures. Just as real love endures, so do the dependable returns of REIT investments.

This Valentine’s Day, show your affection with gifts that stand the test of time, just like these sweet REITs.