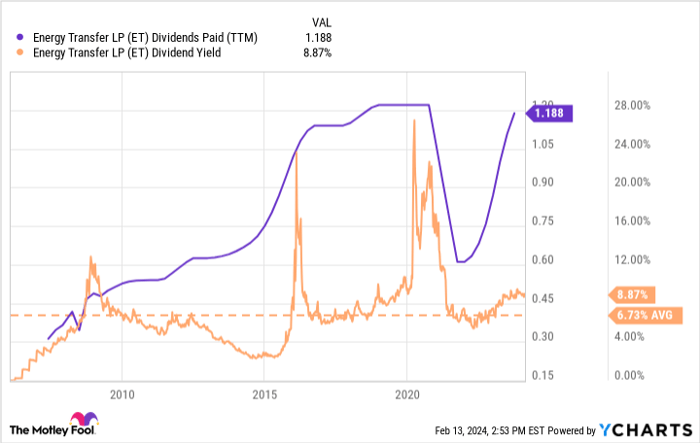

Few stocks are capable of sustaining a 9% dividend. Nonetheless, Energy Transfer (NYSE: ET) defied odds on February 6th by increasing its already high dividend yield above 9%. The company has consistently raised its payout every quarter for over two years. The question remains – can investors rely on this unusually high dividend yield?

Why Energy Transfer is a Dividend Heavyweight

While some businesses focus on growth, Energy Transfer is designed to generate free cash flow. It owns assets capable of producing substantial excess cash – a key reason behind its consistently high dividend yield. As the name suggests, Energy Transfer facilitates the transportation of energy products from extraction sites to refineries and eventually the market. The company primarily deals with crude oil and natural gas, possessing pipeline and terminal assets throughout the U.S., with a strong focus on high-production areas like Texas and neighboring states.

Building assets like pipelines requires significant capital investment. However, once constructed, Energy Transfer often enjoys a monopoly over its customer base. This market power allows the company to dictate terms, enabling it to generate approximately 90% of its cash flow based on fees, mitigating the impact of volatile commodity prices. This stability has facilitated a steady dividend payout for over a decade, with the only exception being a temporary suspension during the early days of the pandemic, as a cautious measure amidst uncertain market liquidity.

For the current year, the company anticipates generating at least $7 billion in distributable cash flow, approximately $1 billion more than required to support the dividend and near-term growth initiatives.

ET Dividends Paid (TTM) data by YCharts.

The Conundrum of High Dividend Yields

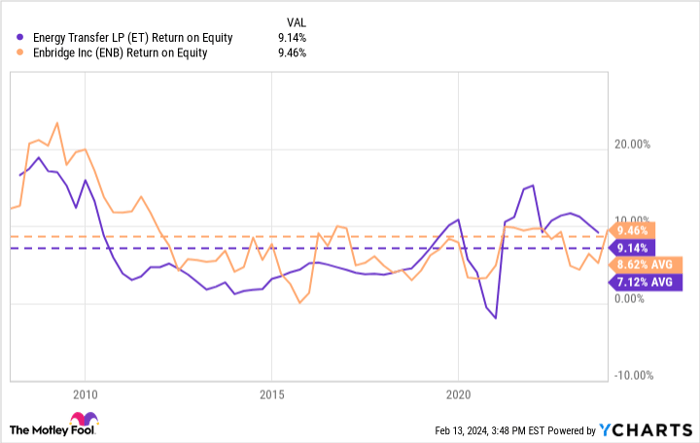

Despite demonstrating the ability to sustain a 9% dividend, Energy Transfer’s stock price isn’t rising to reduce the yield to a more normalized range. Similar companies relying on fossil fuel production have been trading at a discount for years, as evidenced by Enbridge – a close competitor with a dividend yield of around 8%, despite a 10% annual dividend growth for almost three decades. Market hesitancy is not reflective of unreliable dividends or deteriorating business performance; both Energy Transfer and Enbridge have maintained respectable returns on equity over the past decade.

ET Return on Equity data by YCharts.

The underlying concern is the potential of these businesses to hold stranded assets if regulations or market dynamics prompt a sudden shift away from oil and gas. However, while such a shift might occur in the distant future, short-term projections indicate steady growth in oil and gas consumption. Hence, the 9% dividend yield appears sustainable, barring a global recession.

Considering these factors, investing in Energy Transfer for its 9% dividend could be a stable short-term strategy. However, it’s important to acknowledge that the inevitable shift from fossil fuels to renewable energy will present a long-term challenge to sustaining such high dividends.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce substantial returns in the coming years.

Stock Advisor provides investors with a comprehensive blueprint for success, including guidance on portfolio building, regular analyst updates, and two new stock picks each month. The Stock Advisor service has significantly outperformed the S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of February 12, 2024

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Enbridge. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.