American Express (NYSE: AXP) has shot up by more than 30% in the last 90 days, propelling the stock to all-time highs. While some may see this as a sign of overvaluation, there are compelling reasons to consider American Express as an undervalued asset, worthy of long-term investment.

The Numbers Unveil a Promising Story

A substantial increase in a stock’s value doesn’t always equate to overpricing. It’s imperative to delve into the metrics to unravel the driving forces behind this performance surge. American Express appears to be one of those cases.

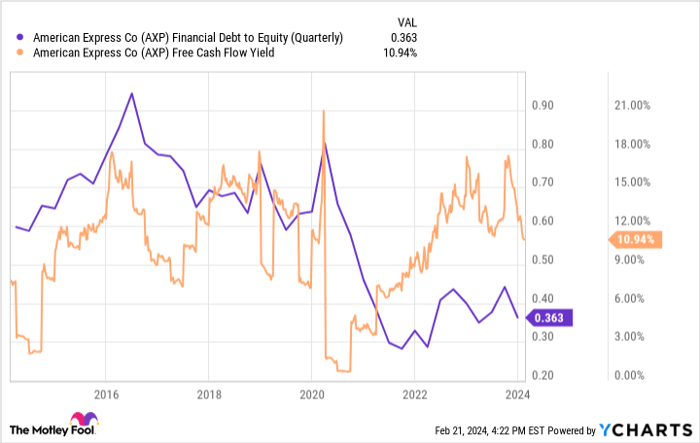

Prior to the recent ascent, the stock traded at a nearly 18% free cash flow yield, a noteworthy figure for a globally renowned brand with a consistent nod from investment maestros such as Warren Buffett. In hindsight, the market made a glaring oversight. Similar price levels have been fleeting over the last decade. Coupled with a swift decrease in debt levels concurrent with the rise in interest rates, American Express found itself in an enviable position.

From a historical perspective, American Express presented an irresistible opportunity back in November, and today, the stock still stands as an attractive investment. Investors are poised to gain an almost 11% free cash flow yield, capitalizing on reduced debt levels, which affords American Express operational flexibility during high-interest rate periods.

Furthermore, despite decreasing debt levels, American Express continues to yield high returns on equity, defying the typical pattern where increasing debts inflate this metric. This showcases the efficiency of its business model and competitive advantages. Essentially, American Express operates with minimal physical assets, leveraging its brand value, likely worth tens of billions of dollars. It would take a competitor decades to replicate its business model and brand recognition.

Is American Express a Forever Stock?

A “forever stock” is exactly what its name suggests – a stock you can hold indefinitely. American Express fits this description.

When identifying “forever stocks,” seeking a company that creates a positive feedback loop is crucial. This means that past growth fuels future growth. Amazon, an undisputed “forever stock,” is a prime example. As more buyers flock to its platform, more sellers are enticed to follow, leading to a cycle of perpetual growth.

American Express reaps the rewards of its own positive feedback loops. Firmly rooted since 1850, American Express has forged an esteemed brand, securing the eighth spot on Fortune‘s 2024 list of the most admirable brands. The trust in its name continually garners new customers, further amplifying its brand value and attracting even more customers.

Additionally, American Express capitalizes on potent network effects akin to Visa and Mastercard. The triad constitutes the primary choices on the finite list of accepted card networks. A widespread merchant acceptance compels consumers to use these cards, creating a cyclical effect. Despite the recent surge, American Express shares are not excessively priced. However, beyond short-term performance, American Express has cultivated a business primed to benefit from positive feedback loops for decades. Acquiring it at a bargain valuation is advantageous, yet the optimal strategy with stocks like American Express is to simply buy and hold them indefinitely.

Should you invest $1,000 in American Express right now?

Before considering an investment in American Express, weigh this:

The Motley Fool Stock Advisor analyst team has pinpointed what they believe to be the 10 best stocks for investors right now, and American Express didn’t make the cut. These selected stocks could yield colossal returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, encompassing portfolio-building guidance, regular analyst updates, and two monthly stock picks. Since 2002, the Stock Advisor service has more than tripled the return of S&P 500*.

See the 10 stocks

*Stock Advisor returns as of February 20, 2024

American Express is an advertising partner of The Ascent, a Motley Fool company. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Mastercard, and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.