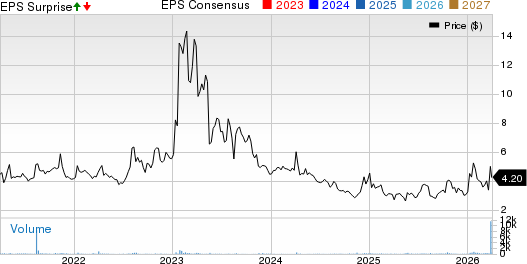

Teleflex Incorporated (TFX) unveiled its fourth-quarter 2023 adjusted earnings per share (EPS) from continuing operations at $3.38, a 4% dip from the previous year. Despite the decrease, the figure outperformed the Zacks Consensus Estimate by an impressive 3.7%.

The GAAP EPS for the fourth quarter stood at 66 cents, contrasting with $1.65 in the same period of the previous year.

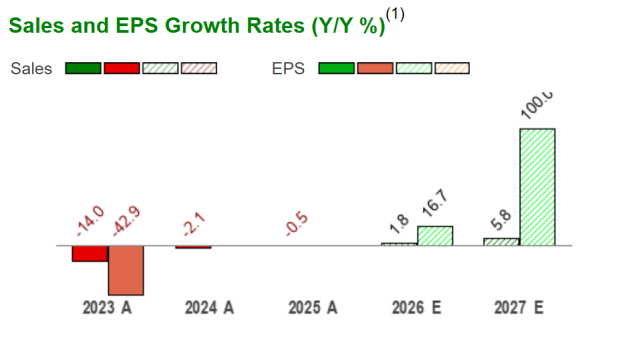

On an annual scale, adjusted EPS for Teleflex reached $13.52, marking a 3.5% uplift from the previous year and surpassing the Zacks Consensus Estimate by 0.8%.

Revenue Performance at a Glance

Teleflex witnessed a 2.1% increase in net revenues for the fourth quarter, reaching $773.9 million year over year, an increase of 0.7% at a constant exchange rate (CER). This figure managed to exceed the Zacks Consensus Estimate by 0.7%.

For the entire fiscal year, revenues amounted to $2.97 billion, indicating a 6.6% rise compared to the previous year (up 6.5% at CER) and aligning with the Zacks Consensus Estimate.

Insights into Segments

The Americas segment reported net revenues of $450.6 million, reflecting a 1.6% decline year over year (down 1.9% at CER). Factors contributing to this drop include slower growth in the Vascular and Surgical business, further exacerbated by five fewer shipping days.

EMEA (Europe, the Middle East, and Africa) segment saw net revenues of $152.4 million, rising by 3.1% year over year but falling by 2.7% at CER due to challenges in Anesthesia and Surgical coupled with fewer shipping days.

Analyzing Financial Figures

Revenues from Asia Pacific surged by 12.5% to $88.3 million (up 12.6% at CER), propelled by strong commercial performance and robust underlying demand.

OEM (Original Equipment Manufacturer and Development Services) also displayed growth, with revenues hitting $82.6 million, climbing 12.1% year over year (up 10.9% at CER).

Detailed Product Revenue Overview

Various segments experienced fluctuations in net revenues. The Vascular Access segment recorded $186.7 million, while the Interventional business boasted $135.6 million in net revenues.

Concerningly, the Anesthesia segment faced a year-over-year revenue decrease to $98.2 million, while the Surgical segment saw a drop to $109.6 million.

Margin Challenges and Future Projections

Gross profit in the fourth quarter rose by 2.2% year over year to $431.4 million, with the gross margin expanding by six basis points to 55.8%. However, the adjusted operating profit decreased by 7.6% to $134.9 million, with an 182-bps contraction in the adjusted operating margin to 17.4%.

Regarding liquidity, Teleflex ended the fourth quarter of 2023 with $222.8 million in cash and cash equivalents, lower than the $292 million at the end of 2022. Cash flow from operating activities surged to $511.7 million from $342.8 million in the year-ago period.

2024 Financial Outlook and Concluding Thoughts

Teleflex outlined its financial guidance for 2024, projecting GAAP revenue growth between 3.6%-4.6% and adjusted EPS from continuing operations in the $13.55-$13.95 range.

Despite facing challenges with declining margins, Teleflex displayed resilience and exceeded revenue expectations, showcasing adept execution in the face of market fluctuations. While margin pressures persist, the company’s strategic initiatives and product launches portend a promising future in the fast-evolving healthcare landscape.

As Teleflex navigates the restorative journey towards margin stability, investors are keenly observing how the company leverages market opportunities and sustains financial performance in the upcoming quarters.

The Rising Stars in the Medical Space: Stryker Corporation, Cencora, Inc., and Cardinal Health

Stryker Corporation: Leading the Pack

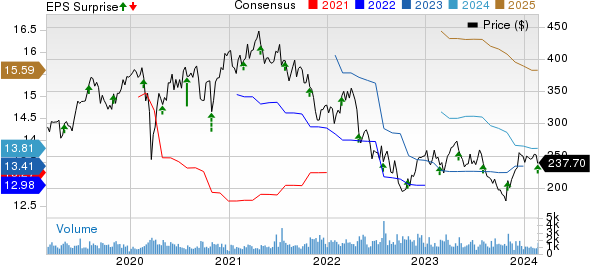

When it comes to soaring above the competition, Stryker Corporation shines as a beacon of success. With a resounding Zacks Rank #2 (Buy), Stryker recently reported a staggering fourth-quarter 2023 adjusted EPS of $3.46, toppling the Zacks Consensus Estimate by an impressive 5.8%. Their revenues, totaling $5.8 billion, surpassed expectations by 3.8%. A feat worthy of applause, no doubt. This medical giant boasts an estimated earnings growth rate for 2025 that leaves the S&P 500 in the dust, at 11.5% compared to the latter’s 9.9%. With consecutive earnings beats over the past four quarters averaging 5.1%, it’s clear that Stryker is not merely running the race but setting the pace for others to follow.

Cencora, Inc.: Surging Ahead

Not one to be overshadowed, Cencora, Inc. is making waves of its own in the medical space. Carrying a respectable Zacks Rank #2, Cencora recently reported a remarkable first-quarter fiscal 2024 adjusted EPS of $3.28, surpassing the Zacks Consensus Estimate by a notable 14.7%. Revenues of $72.3 billion outpaced estimates by 5.1%. With an earnings yield of 5.75%, significantly higher than the industry average of 1.85%, Cencora is proving that it is not just keeping pace but surging ahead in the medical sector. Their consistent earnings beats over the last four quarters, averaging at a remarkable 6.7%, speak volumes about their trajectory.

Cardinal Health: Reaching New Heights

Cardinal Health deserves a standing ovation for its recent accomplishments in the medical domain. With a Zacks Rank #1, Cardinal Health reported second-quarter fiscal 2024 adjusted earnings of $1.82, surpassing the Zacks Consensus Estimate by an impressive 16.7%. Revenues totaling $57.45 billion marked an 11.6% increase compared to the previous year and also exceeded the Zacks Consensus Estimate by 1.1%. With a long-term estimated earnings growth rate of 15.3%, outpacing the industry’s 11.8%, Cardinal Health is not merely climbing the ladder of success; it is reaching new heights with each stride. Their remarkable track record of beating earnings estimates over the past four quarters, with an average surprise of 15.6%, showcases their unwavering commitment to excellence.

Just Released: Zacks Top 10 Stocks for 2024

Hurry – you can still get in early on our 10 top tickers for 2024. Hand-picked by Zacks Director of Research, Sheraz Mian, this portfolio has been stunningly and consistently successful. From inception in 2012 through November 2023, the Zacks Top 10 Stocks gained +974.1%, nearly tripling the S&P 500’s +340.1%. Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2024. You can still be among the first to see these just-released stocks with enormous potential.

Stryker Corporation (SYK) : Free Stock Analysis Report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

Teleflex Incorporated (TFX) : Free Stock Analysis Report

Cencora, Inc. (COR) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.