A Tale of Struggles and Hope

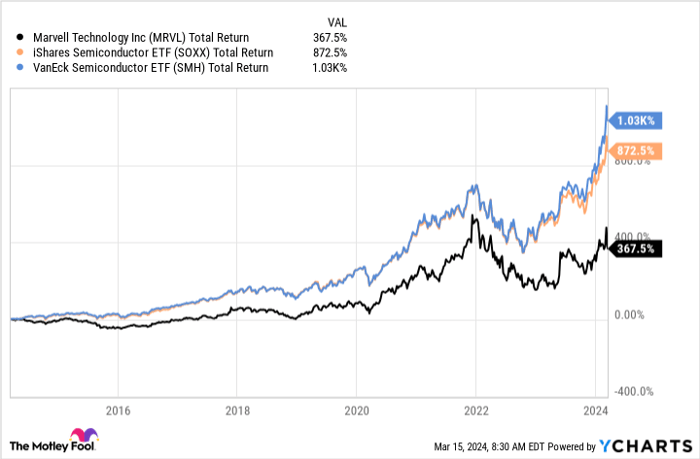

Long-term investors in Marvell Technology (myself included) have weathered quite the storm. The company has trailed the industry average in chip performance for three, five, and a decade when benchmarked against popular ETFs like iShares Semiconductor ETF and VanEck Semiconductor ETF. Through this tumultuous journey, Marvell, under the stewardship of CEO Matthew Murphy since 2016, has undergone a transformation. Strategic acquisitions between 2020 and 2022 were aimed at capitalizing on the burgeoning data center AI explosion. The dividends from these ventures are just beginning to materialize.

The Pivot to AI

Historically, Marvell thrived in selling an array of high-performance network and data storage chips, including consumer devices such as PCs. However, under Murphy’s leadership, the company has pivoted significantly towards data centers, focusing on AI training chips. Marvell has piqued investor interest by highlighting its partnership with Nvidia in accelerated computing systems and positioning itself as a top competitor against industry behemoth Broadcom.

In its fiscal Q4 2024, ending Feb. 3, the data center segment accounted for over half of Marvell’s total revenue. During the earnings call, the CEO revealed that AI chip sales within this sector exceeded $200 million. While the future appears bright for Marvell’s data center and AI division, the other half of its business continues to struggle.

|

Marvell Segment |

Q4 Fiscal 2024 Revenue |

Change (YOY) |

Q1 Fiscal 2025 Expectations (QOQ) |

|---|---|---|---|

|

Data center |

$765 million |

54% |

Low single-digit percentage increase |

|

Enterprise (non-data center and non-cloud) |

$243 million |

(34%) |

40% decrease |

|

Mobile carriers (5G networks and other) |

$171 million |

(38%) |

50% decrease |

|

Consumer markets |

$143 million |

(21%) |

70% decrease |

|

Automotive and industrial |

$82 million |

(17%) |

Flat |

|

Total revenue |

$1.43 billion |

1% |

$1.15 billion, 20% decrease (down 13% YOY) |

Data source: Marvell Technology Group. YOY = year over year. QOQ = quarter over quarter.

Guided by Murphy, Marvell anticipates challenges in non-data center sales in the initial half of the current fiscal year, which threatens to offset the progress in the burgeoning AI market.

Separating Hype from Reality

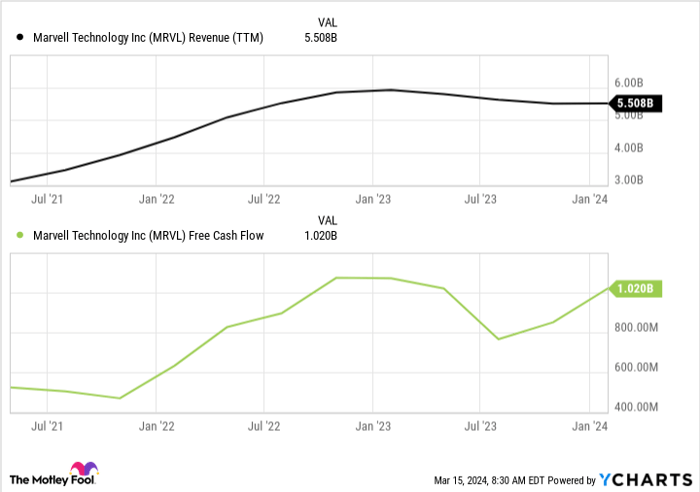

After years of navigating transitions and an industry downturn due to the pandemic aftermath, Marvell foresees stability and growth returning to its markets beyond data centers in the latter part of 2024. Bolstering this outlook, Marvell’s board sanctioned a $3 billion stock repurchase initiative. Although free cash flow has been modest in recent years, the surge in the last quarter to $465 million signals a potential upturn. As the sales of new AI chips intensify post years of development and tech assimilation, Marvell stands at the threshold of a new chapter.

Data by YCharts.

Albeit trading at 56 times trailing-12-month free cash flow, Marvell hardly qualifies as a bargain. Yet, if growth indeed materializes this year, selling at this juncture could prove hasty. I opt to retain my position and observe the fruition of Marvell’s AI endeavors.

Should you invest $1,000 in Marvell Technology now?

Before diving into Marvell Technology stock, consider this insight:

The analyst team at Motley Fool Stock Advisor has identified the 10 best stocks they believe could yield substantial returns in the coming years. Marvell Technology didn’t make the list, but these selected stocks could be the stars of the future.

Stock Advisor offers a roadmap for investment success, including portfolio building guidance, regular analyst updates, and bi-monthly stock picks. Since 2002, the Stock Advisor service has far outpaced the S&P 500’s returns.

Discover the 10 stocks

*Stock Advisor returns as of March 11, 2024

Nicholas Rossolillo and his clients hold positions in Broadcom, Marvell Technology, and Nvidia. The Motley Fool holds and recommends Nvidia and Broadcom. It also recommends Marvell Technology. The Motley Fool upholds a disclosure policy.

The opinions expressed herein are solely those of the author and do not reflect Nasdaq, Inc.’s views.