Steering Through Headwinds and Tailwinds

Home sweet home – a sentiment that underpins the very fabric of our lives. As the housing market ebbs and flows, the guiding star of D.R. Horton (DHI) shines bright in an ocean of uncertainties. The scarcity of existing homes for sale, paired with favorable mortgage rate trends and Federal Reserve musings about a possible rate cut, have infused a newfound optimism in the homebuilding domain. And in this realm of promise, D.R. Horton stands firm, fortified by its stability and robust fundamentals to weather any storm that may come its way.

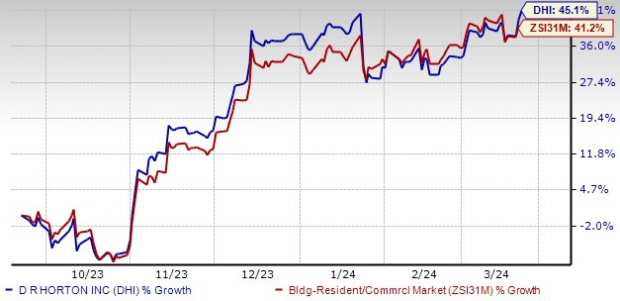

Like a phoenix rising from its ashes, D.R. Horton has basked in the glow of favorable winds, smart acquisition strategies, expanded homebuilding lots, reduced cycle times, and a varied product lineup across different brands and price segments. The company’s stock has surged an impressive 45.1% in the last six months, dwarfing the Building Products – Home Builders industry’s rise of 41.2% during the same period. With a Zacks Rank #3 (Hold) and a healthy long-term earnings growth rate of 12.4%, DHI’s core strength remains unshaken. Bolstering its growth trajectory is a VGM Score of B, supported by a solid Value Score of B.

Strong Winds of Change

Amidst the heady aroma of progress, concerns linger like a shadow over DHI’s doorstep. High SG&A expenses, escalating land/labor costs, and stiff pricing competition continue to cast a pall on the company’s growth story. Analysts have revised down their estimates over the past 60 days, reflecting a cautious sentiment on the stock’s potential. The Zacks Consensus Estimate for fiscal 2024 EPS has edged down to $14.17 from $14.20 over this timeframe.

But what fuels this engine of growth? Let’s dive into the driving forces propelling D.R. Horton forward.

Wind in the Sails – Tailwinds

Improving Macro Scenario: The housing market paints a pretty picture, with a robust job market, limited existing home availability, and inviting mortgage rates setting the stage for growth. The recent Federal Reserve decision to maintain the benchmark interest rate between 5.25%-5.5% is a reassuring beacon for homebuilders, hinting at a stable environment ahead.

On March 20, 2024, the Federal Reserve opted to keep its interest rate steady for the fifth consecutive meeting, citing the need for more data before making any rate changes. As the Fed juggles the delicate art of timing potential actions, the majority anticipates three rate cuts in 2024, fostering a sense of stability for industry players.

Strategic Acquisitions: D.R. Horton’s growth playbook is marked by strategic acquisitions. The company has swiftly absorbed homebuilding entities in coveted markets, a strategy that paid off handsomely. In the fiscal first quarter of 2024, no acquisitions were reported.

In a notable move in July 2023, D.R. Horton successfully acquired Truland Homes’ operations in Baldwin County, AL, and Northwest Florida, for a hefty sum of $100 million in cash. This transaction included approximately 155 homes in inventory, 620 lots, and a backlog of 55 homes. Moreover, the deal encompassed around 660 additional lots through land purchase agreements.

In the same fiscal quarter, the company’s investments in lots, land, and development totaled $2.4 billion, marking a 3% uptick sequentially and a robust 41.2% surge year over year. These investments covered $1.4 billion in finished lots, $740 million for land development, and $270 million for land acquisition.

Affordable Homes: D.R. Horton’s strategic pivot towards more affordable entry-level homes is reaping rich dividends, with this segment witnessing strong demand amidst limited supply. First-time homebuyers constituted around 56% of the company’s closings in the first quarter of fiscal 2024.

As labor and material availability improve, home construction cycle times shorten, enabling the company to release homes for sale earlier in the process. With an eye on 2024, DHI is well-positioned to navigate shifting market dynamics with its affordable product mix and ample lot supply, aligned with evolving homebuyer needs. Projections indicate a 6.7% growth in net sales orders to 24,681 units for the second quarter of fiscal 2024 and a 13.8% increase to 89,166 units for the entire fiscal year, year over year.

A Brisk Challenge – Headwind

Pressure on Margins: Rising land and labor costs present a menacing specter, squeezing margins and eroding homebuilders’ pricing flexibility. Labor scarcities are nudging wages higher, while limited land availability is inflating prices. Simultaneously, bloated costs from finished lots, skilled labor, and soaring material prices pose a quandary, potentially denting margins across key regions.

Responding to market dynamics, homebuilders are dangling tantalizing incentives to stoke sales, albeit at the cost of climbing operating expenses. In the fiscal first quarter of 2024, homebuilding SG&A expenses surged 14.5% to $603.4 million year over year, with these expenses representing 7.8% of revenues, a 50 bps uptick from the prior-year period. The surge can be attributed to expanding operations to fuel growth, alongside ramped-up equity and stock market-driven compensation expenses.

For the same fiscal quarter, the pre-tax profit margin contracted by 140 bps to 16.1% compared to the prior-year period. This erosion stemmed from a 100 bps slide in home sales gross margin and a 50 bps rise in homebuilding SG&A expenses (as a percentage of revenues). For the fiscal second quarter of 2024, the company anticipates homebuilding SG&A expenses (as a percentage of revenues) in the range of 7.5% to 7.7%, up from the prior-year’s 7.3%.

Charting New Waters – Brighter Horizons

As D.R. Horton steers through the choppy waters of the homebuilding landscape, it’s worth noting other solid stocks in the construction sector riding high waves of success.

Other Stars in the Sky

NVR, Inc.: Currently flaunting a Zacks Rank #1 (Strong Buy), NVR’s stock has surged 33.5% in the last six months. The company boasts an average trailing four-quarter earnings surprise of 8.1%. Projections point to a 7.7% growth in 2024 sales and a 4.6% uptick in EPS from the prior year.

Vulcan Materials Company: Sporting a Zacks Rank of 1, VMC has enjoyed a robust 35.4% rise in its stock over the past six months. The company has delivered an average trailing four-quarter earnings surprise of 19.5%. Forecasts indicate a 1.4% growth in 2024 sales and a substantial 19.4% surge in EPS from a year ago.

Sterling Infrastructure, Inc.: Presently adorned with a Zacks Rank of 1, STRL has seen its share price ascend by 53.1% in the last half-year. The company boasts an average trailing four-quarter earnings surprise of 20.4%. Predictions suggest a rise in 2024 sales and EPS for STRL.

Unveiling the Hidden Gems: 5 Promising Stocks 2024

Flying Under the Radar: A Golden Opportunity

In the volatile realm of stock investments, enthusiasts are always on the lookout for the next big thing, a hidden treasure trove that can fuel their coffers with gold. The recent unveiling of Vulcan Materials Company (VMC), D.R. Horton, Inc. (DHI), NVR, Inc. (NVR), and Sterling Infrastructure, Inc. (STRL) has set the financial world abuzz.

Wall Street’s radar might have missed these underdogs, but therein lies a golden opportunity for savvy investors to jump in on the ground floor, primed for potential skyrocketing growth akin to meteoric rises of the past.

Resilience in the Face of Adversity

The financial landscape of 2023 painted a dismal picture with declines reported across various sectors. However, amidst the chaos and uncertainty, these companies stood tall, weathering the storm with admirable resilience.

D.R. Horton, Inc. (DHI) emerges as a standout star, soaring a remarkable 45% in just six months, hinting at the potential for further upside in the unfolding tapestry of 2024.

Shifting Gears: Anticipation and Projections

As investors shift gears to align with the changing winds of fortune, the anticipation and projections surrounding these stocks grow by the day. With experts at Zacks Investment Research pinpointing them as potential home runs set to double – a forecast that rings like a symphony for those looking to strike gold.

The year-over-year growth rates of 11.7%, and 11.4%, respectively, signal a promising trajectory, underlining the potential these stocks hold for discerning investors seeking to navigate the tumultuous waters of the stock market.