Benefits Fueling Vornado’s Growth Trajectory

Vornado Realty Trust (VNO) stands tall amidst the skyline with a portfolio of prime office properties nestled in the bustling markets of New York, Chicago, and San Francisco. The company’s strategic focus on high-rent, high-barrier-to-entry markets and a diverse tenant base comprising industry stalwarts promise a steady influx of cash and cultivation of opportunities in the long run.

With a backdrop of anticipated dips in total revenues in the near future, the sails are set for a 1% and 5.2% rise in 2025 and 2026, respectively. As job markets tailored for office space expansion and rapid growth in technology, finance, and media sectors emerge, Vornado is poised to harness the windfall for an upward trajectory.

The Advantageous Position of Vornado

Surrounded by the glitz and promise of the Big Apple, Vornado’s assets in New York City are a beacon for office occupants seeking to expand their urban footprint. The company’s top-tier properties, adorned with transit-centric locations and plush amenities, are seeing a surge in rentals—a wave that Vornado is set to ride high, acquiring competitive advantages in the process.

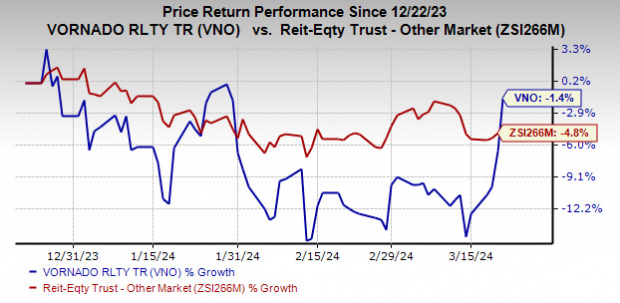

Bolstering the company’s prospects is a robust balance sheet, flaunting $3.2 billion in liquidity as of December 31, 2023. This financial flexibility, coupled with recent refinancing moves to slash borrowing costs, equips Vornado to not only seize upcoming investment opportunities but also ensure the smooth sailing of its ongoing development projects.

Challenges on the Horizon

Yet, amid the upbeat symphony playing for Vornado, discordant notes hover on the horizon. A murky concoction of economic unpredictability and the dawn of hybrid work setups hint at a fluctuating office space demand in the short term. Vornado’s heavy reliance on the New York City office market exposes it to the fluctuating tides of the macroeconomic scenario in that region.

Moreover, the thundercloud of high-interest rates poses as a formidable adversary for Vornado. As borrowing costs swell, casting shadows over its capacity to acquire or develop real estate assets, the company finds itself anchored down by a hefty debt load of approximately $10.28 billion as of December 31, 2023. The allure of substantial dividends acts as a siren’s call for REIT investors; however, a recent dividend reduction and a dim outlook for FFO adjustments in 2024 dampen the gleam, painting a somber picture for dividend seekers.

Exploring Alternatives

If contemplating alternative ventures amidst the real estate shimmer, consider glancing at brighter prospects in the broader REIT sector. Companies like Tanger Inc. (SKT) and SL Green Realty (SLG), adorned with a Zacks Rank #2 (Buy), offer promising avenues for investors seeking to harness the market’s upward currents. With a projection of 3.6% and 19% growth in FFO per share for SKT and SLG in 2024, respectively, these contenders sparkle as potential luminaries in the REIT cosmos.

Remember: the figures discussed regarding earnings are articulated in funds from operations (FFO), a veritable compass steering investors through the enigmatic seas of REIT performance.

Ready to venture into the exciting realm of stocks set to double? Join the ranks of prescient investors and scout for unicorns hidden beneath Wall Street’s gaze. Who knows, the next jackpot could be just a click away!

For further insights and stock analyses, delve into Zacks Investment Research’s treasure trove. Seek wisdom where others falter and let the stars of financial acumen guide your investment journey.