Artificial intelligence (AI) remains an irresistible vortex in the technology domain, propelling titans like Nvidia (NVDA) to meteoric ascents of around 85% year to date. However, for those who feel they may have missed the Nvidia frenzy, fret not! The AI landscape is vast, offering fertile ground for other flourishing ventures.

One such gem is Super Micro Computer (SMCI), a rising star that has dazzled the market with an impressive spike of 804.8% over the last year. The behemoth’s exponential revenue and earnings expansion have catapulted it into the illustrious corridors of the S&P 500 Index, fueling its bull run.

A Glimpse into Super Micro Computer

Super Micro Computer (SMCI) stands as a beacon of efficiency in providing computing solutions. The surge in demand for its AI-centric products has seen its revenue soar by a staggering 103.3% year over year to $3.66 billion in the second quarter of fiscal 2024. Moreover, adjusted earnings per share (EPS) leaped by 71.5% to reach $5.59 in the same interval.

For those with a keen eye on financial figures, the stock has seen an extraordinary 244% surge year to date, vastly outpacing the Nasdaq Composite’s mere 11.3% upturn.

Moreover, in consort with stalwarts like Nvidia, Advanced Micro Devices (AMD), and Intel (INTC), Super Micro Computer unveiled three potent Supermicro SuperCluster solutions fueled by Nvidia GPUs. The establishment concluded the second quarter with substantial cash and cash equivalents standing at $726 million and $376 million in bank debt.

Forecasts hint at a hefty revenue hike in fiscal 2024, with expected figures ranging from $14.3 billion to $14.7 billion, in symmetry with analyst conjectures. Furthermore, a whopping 85% surge in earnings is anticipated for the fiscal year. Eyeing the trajectory into fiscal 2025, analysts project a delightful 40.9% increase in revenue and a corresponding 40.1% uptick in earnings.

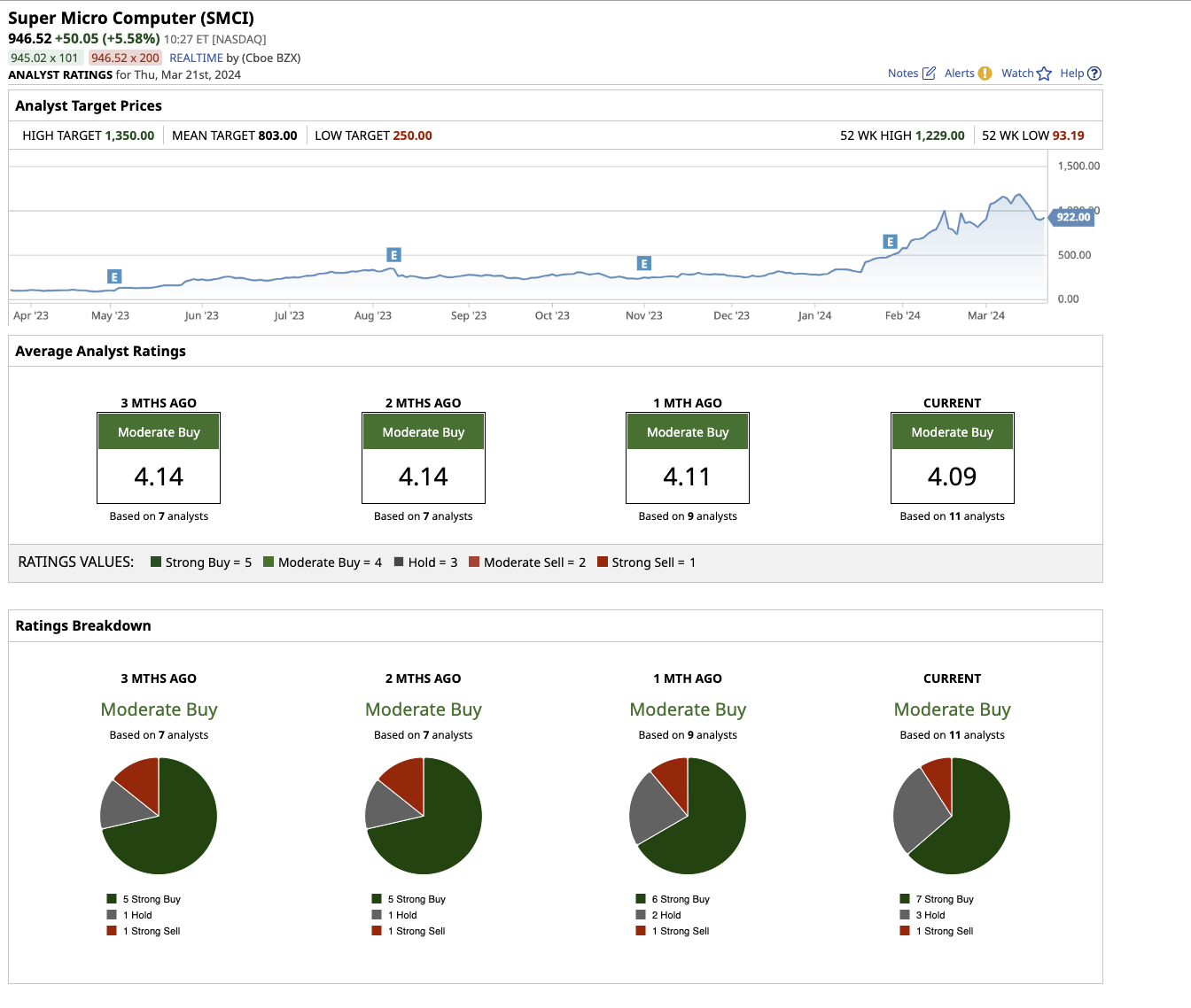

Wall Street sentiment echoes a “moderate buy” for SMCI stock, with analysts notably optimistic about its revenue and earnings avenues. Bank of America Securities’ Ruplu Bhattacharya maintains a resolute “buy” stance with a target price of $1,280, underlining the company’s sturdy foothold in the burgeoning AI server market.

Exploring the Snowflake Phenomenon

Snowflake (SNOW), a stalwart in cloud computing, emerges as a promising contender in the AI realm. The burgeoning demand for AI, cloud computing, and data analytics solutions is a catalyst for Snowflake’s burgeoning prospects.

While last year witnessed Snowflake’s stock ascend by approximately 38% against the S&P’s 25% advancement, its unprofitable standing and lofty valuations have left investors in a contemplative state.

The year 2023 has seen SNOW stock dip by 18% year to date, creating an opportune entrance point for astute investors keen on long-term gains.

Primarily propelled by product revenue stemming from platform consumption, Snowflake witnessed a remarkable 32% surge in total revenue, amounting to $774.7 million in the fourth quarter of fiscal 2024. The stratum of customers generating over $1 million in trailing 12-month product revenue numbered 461, underscoring the company’s formidable presence in the market.

While the profitability eludes Snowflake, a promising trajectory is evident withvisions of a profitable leap in fiscal 2025. Despite trading at 15 times the projected 2025 sales, an upward surge is envisaged with the escalating public cloud expenditure guaranteeing a bountiful horizon for Snowflake in the impending years.

Wall Street consensus deems SNOW stock a “moderate buy,” with anticipations set high as the mean target price hovers at $205.39, portraying a lucrative 27.5% upside potential within the next year.

On the date of publication, Sushree Mohanty held no positions (either directly or indirectly) in any of the securities mentioned in this article. All data and information presented here are intended solely for informational purposes. For more details, refer to the Barchart Disclosure Policy.

The opinions voiced in this article solely represent the author’s views and do not necessarily align with those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.