Unilever PLC (UL), the renowned consumer products company, is on a quest: “Who wants ice cream?” With a presence in 190 countries and serving 3.4 billion people daily, Unilever boasts a diverse portfolio. Brands like Dove, Pond’s, Knorr, and Axe have solidified its global imprint.

Despite its sprawling reach, the ice cream sector accounts for only 13% of Unilever’s $66.23 billion in annual sales. Newly appointed CEO Hein Schumacher inherited a conglomerate clamoring for change, facing years of underperformance and the keen gaze of activist investor Nelson Peltz.

Amidst challenges, Unilever has stumbled, losing market share against competitors like Procter & Gamble (PG). Share prices dipped by 14% over five years, a stark contrast to the S&P 500 Consumer Staples sector’s 38% rise over the same period.

Decoding Schumacher’s Strategy

Schumacher’s game plan involves a two-fold approach: divorcing Unilever from its ice cream arm and streamlining operations. The ice cream business, valued at $17 billion, is set for emancipation by the end of 2025, marking a strategic move aiming to bolster the company’s performance.

The restructuring efforts include slashing 7,500 jobs, amounting to nearly 6% of Unilever’s workforce. Anticipated cost savings of $866 million over three years mark a step towards efficiency and agility.

The spun-off ice cream entity will emerge as a giant in the industry, commanding a 20% market share, and housing five of the globe’s top ten ice cream brands in its stable. Notable names in its repertoire include Ben & Jerry’s, Magnum, and Wall’s.

Despite its significant sales figures, the ice cream division lags behind Unilever’s personal care unit profitability-wise, sporting a profit margin less than half of the company’s average. Operating at 10.8% in 2023, the ice cream unit is a study in contrasts against Unilever’s 16.7% margin.

Grasping the seasonal and capital-intensive nature of the ice cream business, Unilever’s strategic move is delineated by the logic of minimal supply chain overlap with its core operations.

Decoding Schumacher’s Strategy

The moves made by Schumacher have laid the groundwork for a promising transformation. However, as the Financial Times aptly points out, mere financial engineering may not be sufficient.

For Unilever to bridge the valuation gap with its peers, sustained improvement across its core divisions is imperative. Schumacher’s aspirations to push growth targets from the current 3% range to “mid-single digits” accompanied by margin enhancements hint at a proactive stance.

A heightened spotlight on brand and marketing initiatives, rising from 13% of sales in 2022 to 14.3% in the past year, underscore the intent to drive growth holistically.

With a predominant consumer base in emerging markets, accounting for 60% of sales, Unilever holds a unique advantage. Its foothold in the developing world positions it as a long-term growth engine, setting the stage for sustained success.

If the overhaul of Unilever’s structure falls short, a potential separation of its food business might be on the horizon. Such a change would pivot Unilever towards a growth-oriented strategy, accentuating its strengths in home and personal care segments.

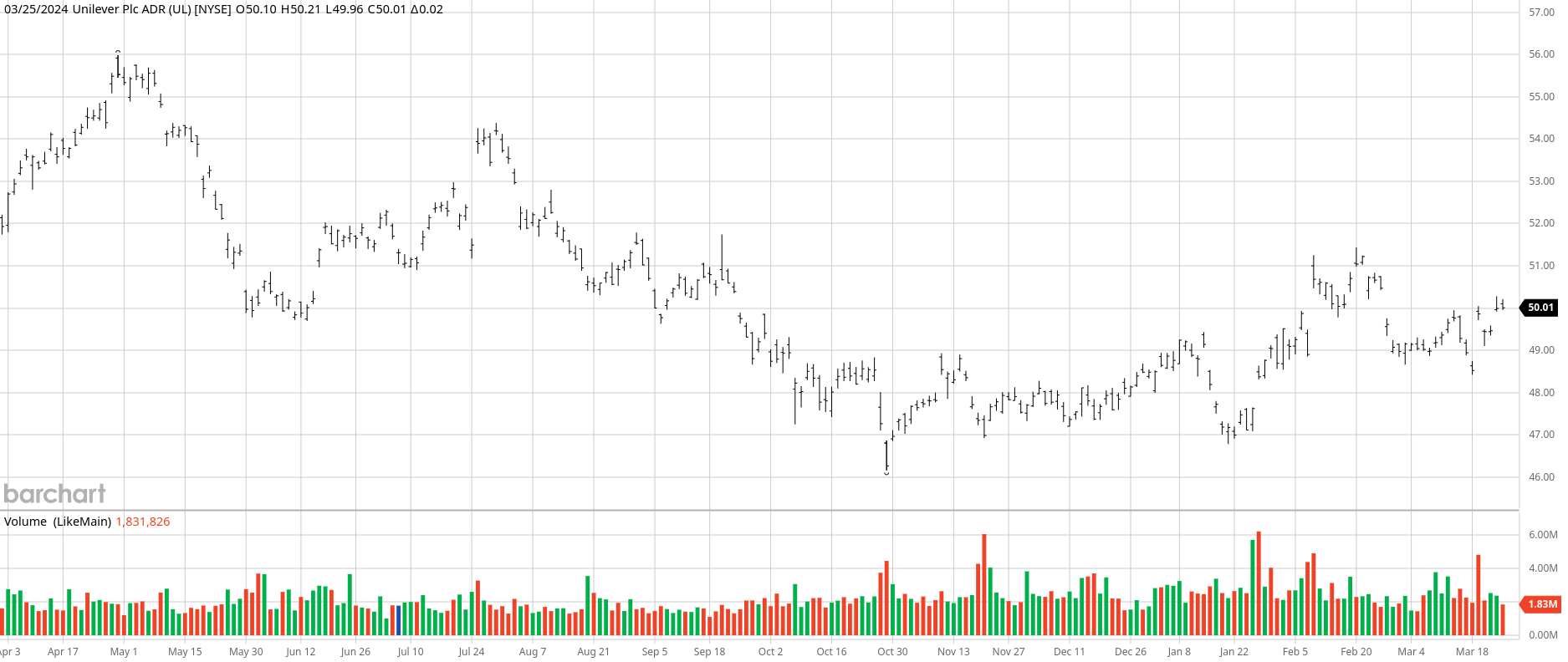

Unilever’s evolution is a saga worth tracking. Valued investors can consider a strategic entry point below $50 for Unilever’s stock.

On the date of publication, Tony Daltorio did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.