Marriott International, Inc. MAR seems poised for a prosperous future owing to an upsurge in leisure demand, strategic digital initiatives, and a robust loyalty program. The company’s relentless focus on expanding its units also adds to its growth saga. While macroeconomic uncertainties linger, the company’s positive outlook shines through.

It’s time to delve into the compelling reasons why investors should consider keeping Marriott within their investment portfolio.

Nurturing Growth Drivers

Marriott is experiencing a wave of pent-up leisure travel demand. In the fourth quarter of 2023, there was a marked increase in leisure transient travel, accounting for 44% of global room nights. This upward trend was accompanied by a 3% rise in Average Daily Rate (ADR) compared to the previous year. The group demand segment exhibited impressive strength, with a 7% year-over-year increase in group revenues in the United States and Canada. Looking forward to 2024, there is a positive outlook with global group revenues up by 13% and Marriott expecting continued momentum in the recovery phase.

The company’s loyalty program, Marriott Bonvoy, boasting almost 196 million members worldwide, plays a pivotal role in supporting its marketing strategies. Marriott is making concerted efforts to elevate customer experience across multiple booking platforms as part of its ongoing technological transformation. With a focus on enhancing engagement beyond hotel stays, Marriott is leveraging successful collaborations within the Marriott Bonvoy ecosystem, including co-branded credit cards. Anticipated growth in total non-RevPAR-related fees for 2024 is expected to range between 9-10% year-over-year, driven by robust credit card and residential branding fee expansion.

Marriott’s strategic focus on global expansion and seizing opportunities in the international hotel market further augments its growth trajectory. Expanding its lodging presence worldwide, the company is making significant headway in the high-growth mid-scale segment. Discussions are underway for potential deals such as Citi Express in the Caribbean and Latin America and Four Points Express in Europe, the Middle East, and Africa. In addition, plans are in motion for a new transient mid-scale brand launch in the United States. As of the end of the fourth quarter of 2023, Marriott’s development pipeline included 3,379 hotels with roughly 573,000 rooms, of which over 232,000 were under construction. For the year 2024, Marriott foresees net room growth in the range of 5.5-6% year over year.

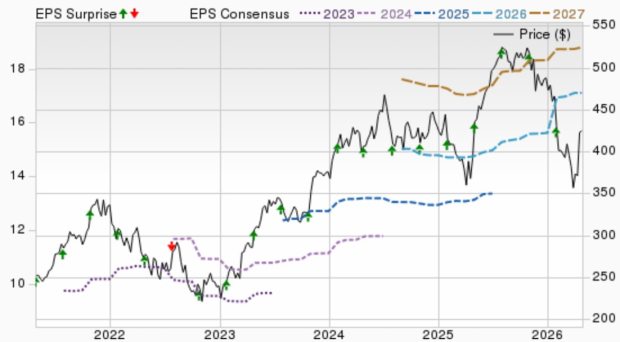

Image Source: Zacks Investment Research

Marriott’s shares have surged by 61% in the past year, outpacing the industry’s 43.3% growth.

Navigating Through Challenges

Despite its stellar performance, Marriott is not immune to the financial market’s uncertainties stemming from liquidity constraints. The prevailing banking climate in the United States and Europe, marked by escalating interest rates, presents challenges in securing financing. The evolving financing landscape, characterized by banks awaiting further clarity on capital requisites and potential regulations, has posed obstacles. However, despite these challenges, Marriott continues to forge ahead with deals backed by committed financing, with no significant escalation in deals falling through.

Zacks Rank & Promising Contenders

Marriott currently holds a Zacks Rank #3 (Hold).

Other notable stocks in the Zacks Consumer Discretionary category worth considering are:

Trip.com Group Limited TCOM, carrying a Zacks Rank #2 (Buy), has charted an average trailing four-quarter earnings surprise of 53.1%. TCOM’s shares saw a 23.7% increase over the past year.

Estimates indicate a year-over-year sales and EPS surge of 18.2% and 8%, respectively, for TCOM in 2024.

Royal Caribbean Cruises Ltd. RCL, boasting a Zacks Rank #2, has an average trailing four-quarter earnings surprise of 26.4%. RCL’s shares catapulted by 125.3% in the past year.

The sales and EPS estimates for RCL in 2024 show anticipated increases of 14.7% and 47.9%, respectively, from the previous year.

Hyatt Hotels Corporation H, with a Zacks Rank #2, displayed an average trailing four-quarter earnings surprise of 17.8%. H’s shares witnessed a 51.5% surge over the past year.

Estimates for H in 2024 indicate a rise of 3.5% in sales and an impressive 27% in EPS compared to the previous year.

5 Stocks Set to Double

Handpicked by a Zacks expert, these stocks are primed for potential growth of +100% or more in 2024. Past recommendations have seen impressive increases of +143.0%, +175.9%, +498.3%, and +673.0%.

Most of the stocks highlighted in this report are flying under the Wall Street radar, presenting an excellent opportunity to get in early on the action.

Discover These 5 Potential Home Runs Today >>

Opinions and insights expressed herein are solely those of the author and may not reflect the views or opinions of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.