The Global Semiconductor Market Revival

The semiconductor industry faced turbulent times recently, with stagnant sales in 2022 and an 11% decline in 2023 due to weakened demand in sectors like smartphones and PCs, leading to an oversupply.

However, 2024 heralds a year of resurgence for semiconductors. Deloitte predicts a 13% revenue growth to reach $588 billion, driven by a 4% projected increase in PC and smartphone sales. Notably, these markets are expected to sustain long-term growth, particularly with the rise of artificial intelligence (AI).

The AI-Driven Semiconductor Boom

AI emerges as a driving force in the semiconductor industry, with demand for AI chips set to grow annually by 38% through 2032, culminating in $372 billion in annual revenue by the end of the period. The escalating need for AI chips is propelling investments in semiconductor equipment to mitigate shortages.

This climate presents a ripe opportunity to invest in Applied Materials (NASDAQ: AMAT), a company specializing in semiconductor manufacturing equipment and services.

Capitalizing on Secular Growth

The semiconductor industry witnesses a surge in new fabrication plants globally, with 42 slated to launch in 2024, a significant increase from 29 in 2022 and 11 in 2023. Projections suggest the global semiconductor market revenue will more than double between 2023 and 2029, reaching $1.38 trillion, signaling substantial growth potential.

With the semiconductor manufacturing equipment market expected to generate $154 billion in 2028 compared to $84 billion in 2021, Applied Materials is primed to capitalize on this trend. Noteworthy customers like Samsung, Taiwan Semiconductor Manufacturing, and Intel contribute significantly to its revenue base.

Driving Revenue Growth and Profit Expansion

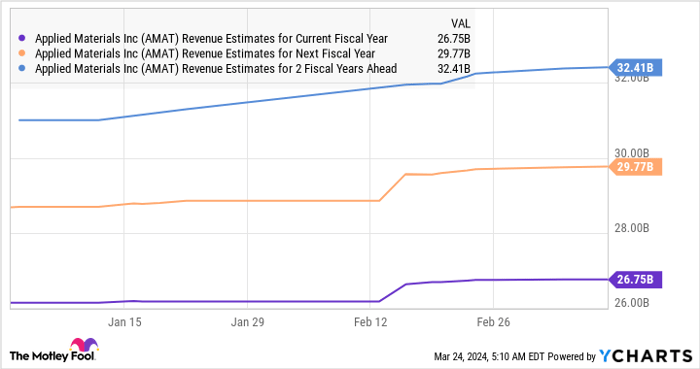

Revenue figures for Applied Materials in the first quarter of fiscal 2024 remained steady at $6.7 billion. Although analysts project flat revenue of $26.8 billion in fiscal 2024, recent estimates indicate a positive revenue trajectory in the upcoming years, with double-digit growth projected.

As illustrated in the charts above, a notable acceleration in top-line growth is anticipated alongside bottom-line growth. Analysts foresee sustained 15% annual earnings growth for the next five years, indicative of Applied Materials’ enduring momentum.

Furthermore, with a relatively low 24 times earnings valuation at present, offering a discount to the Nasdaq-100, investors stand to gain a bargain with Applied Materials’ stock. Given its 30% year-to-date gains, investing in this semiconductor stalwart could lead to substantial returns.

Before making an investment decision, consider analyzing the performance and potential of Applied Materials.

Harsh Chauhan holds no position in the discussed stocks. The Motley Fool has positions in and recommends Applied Materials and Taiwan Semiconductor Manufacturing. It also suggests Gartner and Intel while recommending specific options related to Intel. The Motley Fool operates based on a disclosure policy.

The opinions expressed herein are those of the author and do not necessarily reflect Nasdaq, Inc.’s views.