Weave Communications, Inc. Soars with Augmented Portfolio

Weave’s dedication to expanding its portfolio with a focus on delivering substantial benefits to healthcare recipients has been a standout achievement.

In 2023, Weave added over 450 net new customer sites, underscoring the robust demand for its vertically customized software solution among small and medium-sized healthcare practices, resulting in a burgeoning customer base.

During the fourth quarter of 2023, Weave launched the ACH Debit and Payment Plan to heighten transaction security for patients and present healthcare providers with cost-effective alternatives, including flexible payment schedules through recurring monthly plans.

Recently, Weave unveiled an integration with Athenahealth, enriching healthcare providers’ management capabilities through automation and enhancement features such as automatic data synchronization, missed call notifications, call alerts, birthday wishes, and email marketing.

In February, Weave integrated Payment Plans into its suite, streamlining the payment process for healthcare establishments by enabling automated monthly charges for patients, simplifying billing procedures, and reducing manual invoicing.

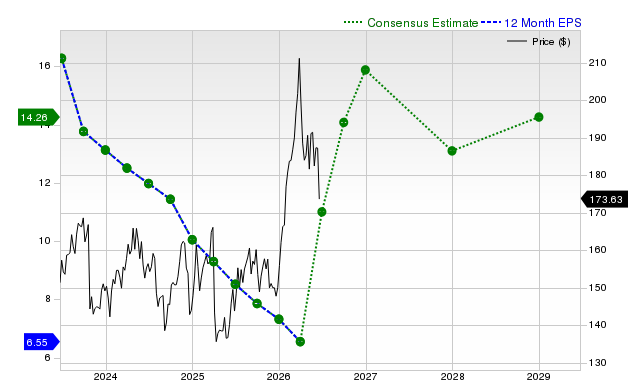

The stellar revenue growth experienced by Weave in the fourth quarter of 2023, reaching $45.7 million, reflecting a 21.2% surge year-over-year, was underpinned by continued high demand for the healthcare platform and steady customer base expansion.

For the first quarter of 2024, Weave predicts revenues in the $45.2-$46.2 million range. The Zacks Consensus Estimate for first-quarter 2024 revenues stands at $45.89 million, indicating a 15.98% year-over-year growth rate.

Furthermore, the Zacks Consensus Estimate for loss remains stable at 2 cents per share over the past 30 days.

Zacks Rank & Recommendations for Investors

Weave currently holds a Zacks Rank #2 (Buy).

Year to date, Weave’s shares have seen a 1.7% increase, a modest progression compared to the 13.6% uptick in the Zacks Computer & Technology sector.

Noteworthy stocks in the broader technology domain, each boasting a Zacks Rank #1 (Strong Buy), include Bill Holdings BILL, Bentley Systems BSY, and NVIDIA NVDA.

Bill Holdings shares have declined by 23.1% year to date. BILL’s projected long-term earnings growth rate is currently 23.64%.

Bentley Systems shares have decreased by 5.5% year to date. BSY’s long-term earnings growth rate is forecasted at 12%.

NVIDIA shares have witnessed a substantial 79.6% increase since the beginning of the year. NVDA’s long-term earnings growth rate is estimated at 30.93%.

To access the original article on Zacks.com, click here.