Micron Technology, Inc. (MU) is experiencing a surge in demand for its high-bandwidth memory (HBM) chips, driven by increased investment from AI hyperscalers and data center operators. The company’s CEO, Sanjay Mehrotra, forecasts fiscal second-quarter 2026 revenues between $18.3 billion and $19.1 billion, an increase from $13.64 billion in the previous quarter. This growth is attributed to ongoing supply constraints and rising prices, bolstering Micron’s profitability, which currently has a net profit margin of 28.2%.

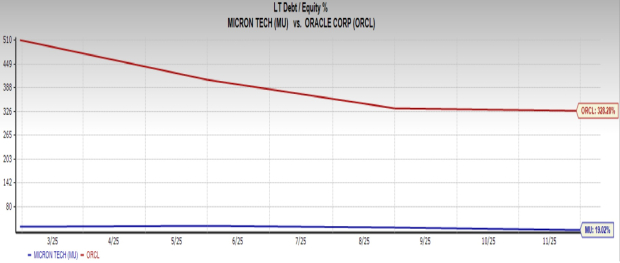

Meanwhile, Oracle Corporation (ORCL) reported a remarkable 438% increase in Remaining Performance Obligations, reaching $523 billion in fiscal second quarter 2026, thanks to new contracts with Meta Platforms, Inc. and NVIDIA Corporation. Despite this growth, Oracle’s business faces challenges linked to an unprofitable partnership with OpenAI and higher financial risk, indicated by its debt-to-equity ratio of 328.3%, compared to Micron’s 19%.

As Micron holds a Zacks Rank of #1 (Strong Buy) while Oracle carries a #3 (Hold), it may currently be the more appealing investment option within the tech sector.