I previously covered Albemarle (NYSE:ALB) in an article where I touted the company’s enduring competitive edge in the lithium sector. However, the time has come for a change. I am temporarily downgrading the stock and in this article, I will shed light on the reasons behind this decision.

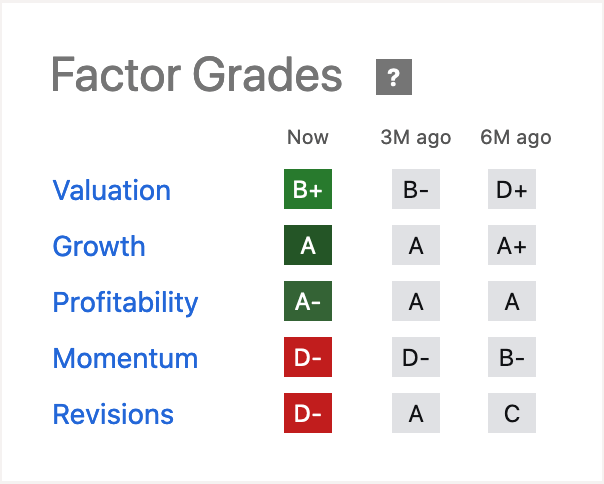

The Seeking Alpha Quant rating for Albemarle indicates a deep value standing, reflecting impressive growth and profitability, but faltering momentum and revision ratings. With the stock plummeting 65% from a high of $325 to $112, investors are naturally plagued with questions – “Will the stock bounce back?” and “When should one expect it?” While I remain steadfast in my conviction that the company will eventually reverse its fortunes, it seems unlikely to occur within the next 3-4 months. Here’s why.

Lithium Prices and Albemarle’s Earnings Forecast

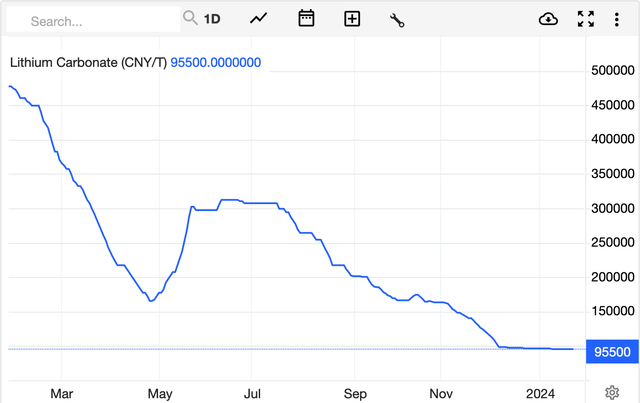

Since my last article, the price of lithium has continued its downward spiral. Initially, the China Spot price of lithium carbonate stood at around $25/kg. Presently, it has plummeted to as low as $13/kg.

The price of spodumene concentrate was reported to be between $1000 and $1200 in December. While I believe in the long-term potential of lithium, various factors have contributed to the price depression, including inventory destocking and marginal supply sources – a matter I expounded upon in my article on Pilbara Minerals (OTCPK:PILBF).

Of particular concern for Albemarle’s stock is the company’s method of forecasting earnings. Instead of making educated guesses about future prices, the firm bases its forecast on prevailing market prices. CEO Kent Masters expounded on this during an earnings call, indicating a worrisome trend.

We decided to do our guidance by not forecasting lithium prices, but by basically take the — whatever the market is today and we forecast it for the balance of the year. And that’s the methodology that we’re going to use for the foreseeable future, the near term.

Essentially, this implies that in their upcoming earnings call, they are likely to revise their price forecast. Consequently, this will precipitate a downgrade in their top and bottom line forecast for 2024.

Some Defensive Actions

Albemarle has recently undertaken several cost-cutting measures in anticipation of their impending earnings call. The company has announced its intentions to, “Preserve Growth, Reduce Costs, and Optimize Cash Flow.” This includes a reduction in growth CAPEX, with Albemarle expecting its 2024 capital expenditures to be in the range of $1.6 billion to $1.8 billion, down from approximately $2.1 billion in 2023. Notably, there are five key bullet points to this strategy.

Notably, they continue their expansion in China but have scaled back their Western expansions. The Kemerton lithium trains, which convert feedstock from the Greenbushes mine, were initially planned to have four trains, but this has been revised down to three.

Additionally, they are postponing their American conversion facilities, a move that was highly anticipated by the US government. Another significant action is Albemarle’s divestment of its stake in Liontown Resources (OTCPK:LINRF). Following a failed bid to acquire the spodumene developer, Albemarle opted to offload its shares, fetching roughly $120 million at a slight discount to the last close.

While these defensive maneuvers are commendable, they signify a tilt towards survival in the short term, rather than thriving. This may trigger fear among investors as they weigh the impact of these actions on the company’s near future.

Earnings Call

On February 14, 2024, Albemarle will host their next earnings call. Several aspects are worth observing. Firstly, they are expected to make an earnings revision. Analysts are likely to inquire about their outlook on the possibility of a price recovery. If the company seems to hint at a lengthy wait, it may be prudent to exercise caution.

Secondly, in the previous earnings call, Albemarle disclosed data about lithium stocks in the upstream. Any signs of dwindling stocks could be a positive indicator.

Thirdly, any cessation in lithium sales warrants attention. The Greenbushes mine, owned in a joint venture, has halted its lithium sales and is now accumulating stocks.

Furthermore, it is essential to monitor the progress of their upgrades. Albemarle is expanding its lithium chemical capacity in China and Australia, with the completion of these projects expected to bolster their capacity.

Lastly, any information pertaining to the Kings Mountain Mine should be noted.

The Bottom Line

Fundamentally, Albemarle remains a formidable company poised for long-term success. Bargain hunters are likely to eye it as a fantastic buying opportunity in the near future should its stock plummet further, possibly below $100.